Have you ever wanted to participate in a leveraged buyout (LBO), but lacked the capital, the management expertise, and the lenders willing to finance most of the purchase? You are in luck! SuperValu (SVU, Financial), at today's prices, has almost all of the characteristics of an LBO without actually being an LBO. This is an important distinction, because it gives you the opportunity to participate.

LBO's are best done on companies with consistent cash flows, as these cash flows will be relied upon to reduce the debt used to finance the purchase. SuperValu has got the cash flow consistency. Demand for groceries does not go away no matter what goes on with the economy, and as a diversified retail grocery chain (operating under a number of banners including Acme, Albertsons, Bristol Farms, Cub Foods, Farm Fresh, Hornbacher’s, Jewel-Osco, Lucky, Save-A-Lot, Shaw’s, Shop ’n Save, Shoppers Food & Pharmacy and Star Market), SuperValu has generated positive operating margins year after year with little fluctuation. (The red ink on the income statements reflects Goodwill write-downs from past purchases, and do not affect the company's cash flows.)

LBO's are also characterized by having a strong, motivated management team to increase efficiency. To that end, SuperValu hired away Wal-Mart's CEO of the Americas to serve as the company's chief executive. Since his hiring in 2009, the CEO has applied cash flows to pay down debt: in the last three quarters, the company has generated about $1.4 billion in cash from operations, and applied over $1 billion of that to debt repayment. He has also implemented initiatives aimed at improving operations, including centralizing marketing, reducing SKUs, and reducing prices. Eighty-six percent of his pay is performance based.

LBO's are also characterized by large debt obligations relative to equity. This is what allows for the large upside for equity owners (profits beyond what is needed to pay off debt accrues to a small amount of equity, resulting in the potential for big returns), but it also represents the biggest risk to the enterprise. Again, SuperValu fits right into the LBO pattern: the company has total debt of $7.1 billion, compared to a market cap of just $1.8 billion.

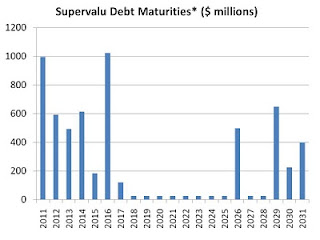

To understand the threat to SuperValu posed by the company's debt, it's important to consider how well the company is able to service its debt obligations. Interest coverage looks okay, as EBIT/interest is around 2, and EBITDA/interest is around 4. But principal repayments appear to be more of a threat, as some of the company's long-term debt is coming due quite soon. The following chart depicts the company's debt obligations over the next several calendar years:

The company only generates operating income of just over $1 billion, so the repayments due in 2011 loom quite large. Additionally, the company has a total of around $1 billion of capital leases due over the next several years which are not included in the chart above. But store refreshes are essential in retail, and this debt repayment schedule does not allow for much re-investment in the business, which is crucial to sustaining cash flow in the future. The company is also experiencing success with its Save-A-Lot banner, and therefore plans to spend capital to open a number of such stores in the coming year.

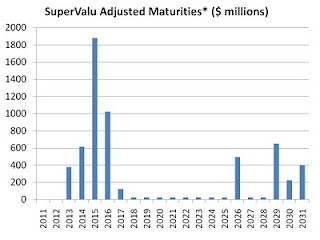

So how can the company meet its obligations and run the business successfully? Using its bank revolver. The company has a revolving line of credit expiring in 2015 under which it still has $1.7 billion available. As such, whatever it cannot pay off in 2011, it can borrow from the revolver. Adjusting the above chart for this revolver makes the debt schedule look as follows:

This gives the company a lot of breathing room in the near term. But it doesn't mean the company's debt is not a threat. What it does do, however, is allow the company to make the capital expenditures it needs to improve the business. Capex not required by the business (which appears to be most of the company's operating cash flow, judging from management's actions) can still go towards paying off debt.

Finally, the company has also been selling under-performing assets in order to generate cash. This helps both accelerate debt payments and make the company more profitable.

The price of the entire Supervalu enterprise (debt + equity) is around $9 billion, against earnings before interest, taxes and non-cash writedowns of about $1.1 billion, for an EV/EBIT ratio of about 8. Since SuperValu has both the breathing room and the cash flows to make the debt repayments and capital expenditures it needs to, the company should see an increase in the market value of its shares even if its enterprise value were to fall.

Disclosure: None

Saj Karsan

http://barelkarsan.com

LBO's are best done on companies with consistent cash flows, as these cash flows will be relied upon to reduce the debt used to finance the purchase. SuperValu has got the cash flow consistency. Demand for groceries does not go away no matter what goes on with the economy, and as a diversified retail grocery chain (operating under a number of banners including Acme, Albertsons, Bristol Farms, Cub Foods, Farm Fresh, Hornbacher’s, Jewel-Osco, Lucky, Save-A-Lot, Shaw’s, Shop ’n Save, Shoppers Food & Pharmacy and Star Market), SuperValu has generated positive operating margins year after year with little fluctuation. (The red ink on the income statements reflects Goodwill write-downs from past purchases, and do not affect the company's cash flows.)

LBO's are also characterized by having a strong, motivated management team to increase efficiency. To that end, SuperValu hired away Wal-Mart's CEO of the Americas to serve as the company's chief executive. Since his hiring in 2009, the CEO has applied cash flows to pay down debt: in the last three quarters, the company has generated about $1.4 billion in cash from operations, and applied over $1 billion of that to debt repayment. He has also implemented initiatives aimed at improving operations, including centralizing marketing, reducing SKUs, and reducing prices. Eighty-six percent of his pay is performance based.

LBO's are also characterized by large debt obligations relative to equity. This is what allows for the large upside for equity owners (profits beyond what is needed to pay off debt accrues to a small amount of equity, resulting in the potential for big returns), but it also represents the biggest risk to the enterprise. Again, SuperValu fits right into the LBO pattern: the company has total debt of $7.1 billion, compared to a market cap of just $1.8 billion.

To understand the threat to SuperValu posed by the company's debt, it's important to consider how well the company is able to service its debt obligations. Interest coverage looks okay, as EBIT/interest is around 2, and EBITDA/interest is around 4. But principal repayments appear to be more of a threat, as some of the company's long-term debt is coming due quite soon. The following chart depicts the company's debt obligations over the next several calendar years:

The company only generates operating income of just over $1 billion, so the repayments due in 2011 loom quite large. Additionally, the company has a total of around $1 billion of capital leases due over the next several years which are not included in the chart above. But store refreshes are essential in retail, and this debt repayment schedule does not allow for much re-investment in the business, which is crucial to sustaining cash flow in the future. The company is also experiencing success with its Save-A-Lot banner, and therefore plans to spend capital to open a number of such stores in the coming year.

So how can the company meet its obligations and run the business successfully? Using its bank revolver. The company has a revolving line of credit expiring in 2015 under which it still has $1.7 billion available. As such, whatever it cannot pay off in 2011, it can borrow from the revolver. Adjusting the above chart for this revolver makes the debt schedule look as follows:

This gives the company a lot of breathing room in the near term. But it doesn't mean the company's debt is not a threat. What it does do, however, is allow the company to make the capital expenditures it needs to improve the business. Capex not required by the business (which appears to be most of the company's operating cash flow, judging from management's actions) can still go towards paying off debt.

Finally, the company has also been selling under-performing assets in order to generate cash. This helps both accelerate debt payments and make the company more profitable.

The price of the entire Supervalu enterprise (debt + equity) is around $9 billion, against earnings before interest, taxes and non-cash writedowns of about $1.1 billion, for an EV/EBIT ratio of about 8. Since SuperValu has both the breathing room and the cash flows to make the debt repayments and capital expenditures it needs to, the company should see an increase in the market value of its shares even if its enterprise value were to fall.

Disclosure: None

Saj Karsan

http://barelkarsan.com