After a brief (overseas holiday related) absence, the top 5 graphs of the week are back! This week we look at China's inflation numbers, as well as its international trade figures. Then we also review the inflation numbers from the US and UK, before checking out some of the monetary policy decisions out over the past week.

1. China Inflation

China recorded inflation of 4.9% year on year in January (4.6% in December), at least we think... The National Bureau of Statistics did make some adjustments to the way they calculate inflation e.g. changes to the basket of goods that make up the CPI, but it's not clear what the impact is. Anyway one thing's for sure, inflation is still chugging away thanks to short-term food price spikes, as well as rising energy commodity prices... and of course a generally booming economy (and property market - in spite of measures to lift supply and curb prices). This is a key risk area for China - both policy makers and investors - this year, so keep watching this space.

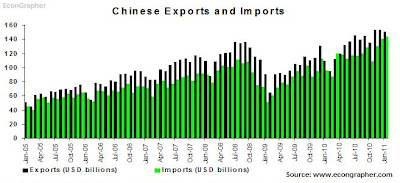

2. China International Trade

China chalked up about a US$6 billion trade surplus in January (usually about 15-20 billion), mostly thanks to a record imports number (that's good...). Of course the lunar new year holiday will be having a distorting effect, but look at the numbers, China is seeing a pretty strong rebound in trade volumes. The surge in imports is good for China suppliers, and the strong exports show that somewhere out there people are still buying stuff from the Chinese - so it's a relatively positive sign for the global economy. There's also likely some domestic demand impact on imports - and that will be something to watch over the medium term.

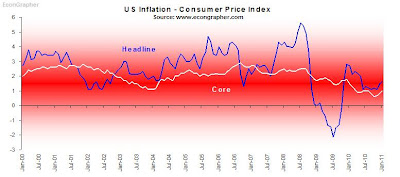

3. US Inflation

Meanwhile in the US, the patient showed signs of life. Core inflation came in at 1%, while headline was about 1.6%. So inflation is still relatively subdued, but the slight increase in core inflation is interesting; sure the numbers are liable to be choppy, but is this the all clear for those worried about deflation? Think about exceedingly loose monetary and fiscal policy (which will likely stay so for an extended period), think also about imported emerging market inflation, think also about rising commodity prices, think also about fake spare capacity, and also spare a couple of thoughts to a rebounding economy (sooner or later)... is high US inflation an emerging theme? maybe not yet, but something to think about!

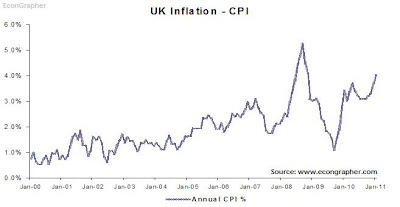

4. UK Inflation

Over in the UK, the inflation spike is already there, up to an emerging market-like 4% now. Albeit some of the surge in inflation is related to one-offs like tax increases, etc; but there is a rising risk that these things flow through into real price expectations and negotiations. Indeed, the spike in inflation has stoked sentiment for rate expectations, with a few punters suggesting 3 rate hikes by the Bank of England in 2011; and with the market already pricing in some tightening. Will the Bank of England make a move? would it touch the interest rate first or wind back the asset purchase program? Not sure, but if I had to guess I would call a rate hike sometime in the medium term.

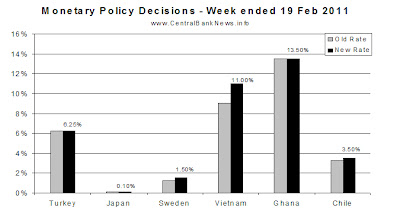

5. Monetary Policy Review

Over the past week Turkey held at 6.25%, Japan at 0.10%, and Ghana at 13.50%. Meanwhile the ones to move were Sweden +25bps to 1.50%, Vietnam +200bps to 11.00%, and Chile +25bps to 3.50%. Oh and the People's Bank of China hiked the reserve ratio another 50bps to 19.5% for large banks (on average), and 16% for the smaller banks. So what's the takeaway? Emerging markets inflation basically; and of course emerging market monetary policy tightening - it's a major theme for this year, especially with the spike in commodity prices (esp. food prices due to a range of factors including a few supply issues) and generally stronger economic growth in emerging markets. It's likely we'll see more such activity through the rest of the year.

Summary

So we saw China with relatively high inflation, in spite of the People's Bank of China's best efforts so far; it's likely we'll continue seeing high inflation figures in the near term. China also chalked up some interesting trade numbers, which say good things for China - but also for those that are doing business with them. Meanwhile in the US, inflation showed signs of life - perhaps even a harbinger of things to come. While the UK inflation situation continued to provide headache material for the Bank of England, with a spike in the CPI numbers. In monetary policy the theme continued to center on emerging market inflation and policy tightening.

Sources

1. National Bureau of Statistics www.stats.gov.cn & People's Bank of China www.pbc.gov.cn

2. China Customs www.customs.gov.cn

3. Bureau of Labor Statistics www.bls.gov

4. Trading Economics www.tradingeconomics.com

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs19feb11.html

1. China Inflation

China recorded inflation of 4.9% year on year in January (4.6% in December), at least we think... The National Bureau of Statistics did make some adjustments to the way they calculate inflation e.g. changes to the basket of goods that make up the CPI, but it's not clear what the impact is. Anyway one thing's for sure, inflation is still chugging away thanks to short-term food price spikes, as well as rising energy commodity prices... and of course a generally booming economy (and property market - in spite of measures to lift supply and curb prices). This is a key risk area for China - both policy makers and investors - this year, so keep watching this space.

2. China International Trade

China chalked up about a US$6 billion trade surplus in January (usually about 15-20 billion), mostly thanks to a record imports number (that's good...). Of course the lunar new year holiday will be having a distorting effect, but look at the numbers, China is seeing a pretty strong rebound in trade volumes. The surge in imports is good for China suppliers, and the strong exports show that somewhere out there people are still buying stuff from the Chinese - so it's a relatively positive sign for the global economy. There's also likely some domestic demand impact on imports - and that will be something to watch over the medium term.

3. US Inflation

Meanwhile in the US, the patient showed signs of life. Core inflation came in at 1%, while headline was about 1.6%. So inflation is still relatively subdued, but the slight increase in core inflation is interesting; sure the numbers are liable to be choppy, but is this the all clear for those worried about deflation? Think about exceedingly loose monetary and fiscal policy (which will likely stay so for an extended period), think also about imported emerging market inflation, think also about rising commodity prices, think also about fake spare capacity, and also spare a couple of thoughts to a rebounding economy (sooner or later)... is high US inflation an emerging theme? maybe not yet, but something to think about!

4. UK Inflation

Over in the UK, the inflation spike is already there, up to an emerging market-like 4% now. Albeit some of the surge in inflation is related to one-offs like tax increases, etc; but there is a rising risk that these things flow through into real price expectations and negotiations. Indeed, the spike in inflation has stoked sentiment for rate expectations, with a few punters suggesting 3 rate hikes by the Bank of England in 2011; and with the market already pricing in some tightening. Will the Bank of England make a move? would it touch the interest rate first or wind back the asset purchase program? Not sure, but if I had to guess I would call a rate hike sometime in the medium term.

5. Monetary Policy Review

Over the past week Turkey held at 6.25%, Japan at 0.10%, and Ghana at 13.50%. Meanwhile the ones to move were Sweden +25bps to 1.50%, Vietnam +200bps to 11.00%, and Chile +25bps to 3.50%. Oh and the People's Bank of China hiked the reserve ratio another 50bps to 19.5% for large banks (on average), and 16% for the smaller banks. So what's the takeaway? Emerging markets inflation basically; and of course emerging market monetary policy tightening - it's a major theme for this year, especially with the spike in commodity prices (esp. food prices due to a range of factors including a few supply issues) and generally stronger economic growth in emerging markets. It's likely we'll see more such activity through the rest of the year.

Summary

So we saw China with relatively high inflation, in spite of the People's Bank of China's best efforts so far; it's likely we'll continue seeing high inflation figures in the near term. China also chalked up some interesting trade numbers, which say good things for China - but also for those that are doing business with them. Meanwhile in the US, inflation showed signs of life - perhaps even a harbinger of things to come. While the UK inflation situation continued to provide headache material for the Bank of England, with a spike in the CPI numbers. In monetary policy the theme continued to center on emerging market inflation and policy tightening.

Sources

1. National Bureau of Statistics www.stats.gov.cn & People's Bank of China www.pbc.gov.cn

2. China Customs www.customs.gov.cn

3. Bureau of Labor Statistics www.bls.gov

4. Trading Economics www.tradingeconomics.com

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs19feb11.html