There appears to be a prevailing market belief that commodity prices can only rise over the next several years. Inelastic demand from developed countries and unremitting demand growth from emerging markets are the most commonly cited reasons for this. As a result, investors are putting companies in this space on a pedestal, taking recent earnings growth of such firms for granted. Value investors must be careful not to get caught up in this game of rising commodity prices leading to rising earnings expectations; it can result in portfolio disaster.

One commodity in particular that well-represents the general consensus of that of commodity bulls is the oil market. Demand for oil is indeed inelastic in the short-term; one cannot design a more fuel-efficient car overnight, and nor does one upgrade his car overnight in response to a change in the price of oil. But over the long-term, the market for oil is like any other market in that it responds to price signals.

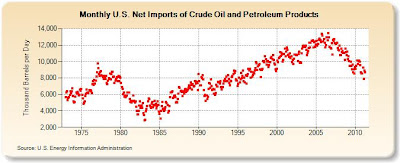

To see this in action, consider US oil imports over the last several years (click to enlarge):

In the chart above, it is clear that oil consumers react to high oil prices, it just takes them time. In both the early 80's, and in the last five years or so, high oil prices resulted in down-trending consumption in the ensuing years. Though it may be argued that part of the reason for the fall in consumption is thanks to the recession, it is worth noting that US GDP today is around 50% higher than it was in the mid to late 1990's, which was the last time the US was importing so little oil according to the chart.

Of course, making up for this demand are emerging markets like China and India, where economic growth is strong. Despite this, however, global "proved" oil reserves are actually increasing despite these draw-downs.

But what happens if these emerging markets have not conquered the business cycle? If growth slows or a recession is experienced in these economic behemoths, expect there to be a lot of oil for sale without a lot of takers.

Furthermore, as oil prices currently remain high, a number of new technologies are about to make it possible to consume less oil without lowering our cushy living standards. For example, hybrids and electric vehicles continue to improve in fuel efficiency and price. Since transportation fuels make up more than 70% of oil consumption, expect technology changes in this space to meaningfully reduce oil consumption in the coming years.

Though I am clearly a long-term bear on oil, the end result of all this may very well be that oil (and other commodity) prices will continue to rise as they have over the last decade. But hopefully it is clear that whether this will happen or not is not clear at all. The future is uncertain, and considering the cyclical nature of this industry, it would be very dangerous to extrapolate the last ten years into the future.

For example, can you really predict what an oil services firm will earn five or ten years from now with any reasonable standard of deviation? Probably not. But if you pay 10 times earnings for such a company, you are implicitly saying that you can.

Commodity prices are volatile and difficult to predict over the next week, let alone over the next few years. As such, it is best for investors to stay away. Why place a bet when the odds are uncertain? Place your bets when the odds are in your favour.

One commodity in particular that well-represents the general consensus of that of commodity bulls is the oil market. Demand for oil is indeed inelastic in the short-term; one cannot design a more fuel-efficient car overnight, and nor does one upgrade his car overnight in response to a change in the price of oil. But over the long-term, the market for oil is like any other market in that it responds to price signals.

To see this in action, consider US oil imports over the last several years (click to enlarge):

In the chart above, it is clear that oil consumers react to high oil prices, it just takes them time. In both the early 80's, and in the last five years or so, high oil prices resulted in down-trending consumption in the ensuing years. Though it may be argued that part of the reason for the fall in consumption is thanks to the recession, it is worth noting that US GDP today is around 50% higher than it was in the mid to late 1990's, which was the last time the US was importing so little oil according to the chart.

Of course, making up for this demand are emerging markets like China and India, where economic growth is strong. Despite this, however, global "proved" oil reserves are actually increasing despite these draw-downs.

But what happens if these emerging markets have not conquered the business cycle? If growth slows or a recession is experienced in these economic behemoths, expect there to be a lot of oil for sale without a lot of takers.

Furthermore, as oil prices currently remain high, a number of new technologies are about to make it possible to consume less oil without lowering our cushy living standards. For example, hybrids and electric vehicles continue to improve in fuel efficiency and price. Since transportation fuels make up more than 70% of oil consumption, expect technology changes in this space to meaningfully reduce oil consumption in the coming years.

Though I am clearly a long-term bear on oil, the end result of all this may very well be that oil (and other commodity) prices will continue to rise as they have over the last decade. But hopefully it is clear that whether this will happen or not is not clear at all. The future is uncertain, and considering the cyclical nature of this industry, it would be very dangerous to extrapolate the last ten years into the future.

For example, can you really predict what an oil services firm will earn five or ten years from now with any reasonable standard of deviation? Probably not. But if you pay 10 times earnings for such a company, you are implicitly saying that you can.

Commodity prices are volatile and difficult to predict over the next week, let alone over the next few years. As such, it is best for investors to stay away. Why place a bet when the odds are uncertain? Place your bets when the odds are in your favour.