Novartis AG (NVS, Financial), through its subsidiaries, engages in the research, development, manufacture, and marketing of healthcare products worldwide. Novartis is an international dividend achiever, has paid uninterrupted dividends on its common stock since 1992 and increased payments to common shareholders every year for 14 years.

The most recent dividend increase was in November 2010, when the Board of Directors approved a 4.80% increase to 2.20 CHF/share. The largest competitors of Novartis include Pfizer (PFE, Financial), Merck (MRK, Financial) and GlaxoSmithKline (GSK, Financial).

Over the past decade this dividend growth stock has delivered an annualized total return of 8% to its shareholders.

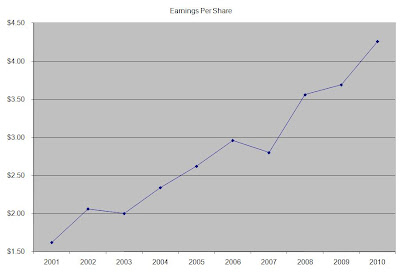

The company has managed to deliver an increase in EPS of 11.30% per year since 2001. Analysts expect Novartis to earn $5.51 per share in 2011 and $5.73 per share in 2012. In comparison Novartis earned $4.26 /share in 2010. The company has managed to consistently repurchase 2.10% of its common stock outstanding over the past decade through share buybacks.

The company is focusing on developing new pharmaceutical products, expanding its generics division and launching new platforms such as vaccines. Novartis also owns 33% of the bearer shares of Roche Holdings (RHHBY), valued at $8.1 billion at the end of 2010. This represents a 6.40% interest in the total equity of Roche Holdings.

The company’s acquisition of Alcon makes it the leader in eyecare globally. The margins in this segment are high, the acquisition will be accretive to EPS starting in FY 2011 and there is an opportunity for expansion in emerging markets

As a pharmaceuticals company, Novartis’s success is dependent on launching new drugs. Two new drugs are expected to add solid returns to the bottom line – Gilenya for multiple sclerosis and Galvus for diabetes. The company has a very strong pipeline, with 60 compounds and 25 new molecules.

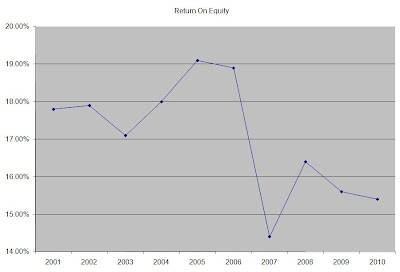

The return on equity has decreased from 18% in 2001 to 15.50% in 2010. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

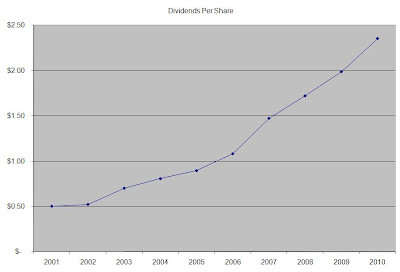

The annual dividend payment in US Dollars has increased by 18.70% per year over the past decade, which is higher than the growth in EPS. The increase in dividends in Swiss Francs has increased by 10.50% per year since 2001. Switzerland based companies, withhold 15% of any distributions made to US investors at source. US investors can deduct the 15% withholding on the US tax returns however. As a result, holding shares of Novartis in a tax-deferred account is not advisable, since no tax credit can be claimed on such accounts.

A 10% growth in distributions translates into the dividend payment doubling almost every 7years. If we look at historical data, going as far back as 1997, we see that Novartis has actually managed to double its dividend every six and a half years on average.

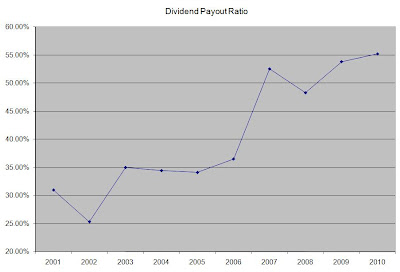

The dividend payout ratio is currently above 50%, although just by a few percentage points. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently Novartis is trading at 13.20 times earnings, yields 3.60% and has a sustainable dividend payout. The company currently fits my entry criteria, and I would consider initiating a position subject to availability of funds and my portfolio sector allocation.

Full Disclosure: None

The most recent dividend increase was in November 2010, when the Board of Directors approved a 4.80% increase to 2.20 CHF/share. The largest competitors of Novartis include Pfizer (PFE, Financial), Merck (MRK, Financial) and GlaxoSmithKline (GSK, Financial).

Over the past decade this dividend growth stock has delivered an annualized total return of 8% to its shareholders.

The company has managed to deliver an increase in EPS of 11.30% per year since 2001. Analysts expect Novartis to earn $5.51 per share in 2011 and $5.73 per share in 2012. In comparison Novartis earned $4.26 /share in 2010. The company has managed to consistently repurchase 2.10% of its common stock outstanding over the past decade through share buybacks.

The company is focusing on developing new pharmaceutical products, expanding its generics division and launching new platforms such as vaccines. Novartis also owns 33% of the bearer shares of Roche Holdings (RHHBY), valued at $8.1 billion at the end of 2010. This represents a 6.40% interest in the total equity of Roche Holdings.

The company’s acquisition of Alcon makes it the leader in eyecare globally. The margins in this segment are high, the acquisition will be accretive to EPS starting in FY 2011 and there is an opportunity for expansion in emerging markets

As a pharmaceuticals company, Novartis’s success is dependent on launching new drugs. Two new drugs are expected to add solid returns to the bottom line – Gilenya for multiple sclerosis and Galvus for diabetes. The company has a very strong pipeline, with 60 compounds and 25 new molecules.

The return on equity has decreased from 18% in 2001 to 15.50% in 2010. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

The annual dividend payment in US Dollars has increased by 18.70% per year over the past decade, which is higher than the growth in EPS. The increase in dividends in Swiss Francs has increased by 10.50% per year since 2001. Switzerland based companies, withhold 15% of any distributions made to US investors at source. US investors can deduct the 15% withholding on the US tax returns however. As a result, holding shares of Novartis in a tax-deferred account is not advisable, since no tax credit can be claimed on such accounts.

A 10% growth in distributions translates into the dividend payment doubling almost every 7years. If we look at historical data, going as far back as 1997, we see that Novartis has actually managed to double its dividend every six and a half years on average.

The dividend payout ratio is currently above 50%, although just by a few percentage points. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently Novartis is trading at 13.20 times earnings, yields 3.60% and has a sustainable dividend payout. The company currently fits my entry criteria, and I would consider initiating a position subject to availability of funds and my portfolio sector allocation.

Full Disclosure: None