Teekay LNG Partners reported fourth-quarter DCF of $44.1 million, up 12 percent from a year ago. These results covered the partnership’s quarterly distribution of $0.63 per unit but seemingly left little margin for error.

For many Master Limited Partnerships, such a thin coverage ratio would be construed as a red flag. But Teekay LNG Partners’ contract-backed income stream limits its exposure to prevailing commodity prices or economic conditions. In fact, management disclosed plans to increase the MLP’s quarterly distribution by 7 percent, to $0.675 per unit, in the first quarter of 2012.

Teekay LNG Partners owns a fleet of 20 ships that transport liquefied natural gas (LNG), five vessels that carry liquefied petroleum gas (LPG), and 11 conventional oil tankers. All its existing ships are contracted under long-term time charter arrangements at fixed day-rates; the MLP’s LNG carriers have an average of 16 years remaining on their fixtures, while the average outstanding contract for its LPG and conventional oil tankers stands at 15 years and 10 years, respectively.

Day rates for oil tankers continue to languish. Although demand for these vessels remains solid, a glut of newly constructed vessels has led to an oversupply of capacity, depressing day rates to levels that make it difficult for many operators to turn a profit. These headwinds, coupled with declining ship values, have forced General Maritime and a number of tanker owners to declare bankruptcy. Read more on the tanker industry.

But these headwinds won’t push Teekay LNG Partners on the rocks; conventional oil tankers only account for a small percentage of the firm’s DCF, and most of the MLP’s vessels are booked under long-term time charters at fixed day rates. When the contracts on Teekay LNG Partners’ oil tankers roll off five to 10 years from now, the supply-demand balance in this shipping market should have normalized.

Meanwhile, Teekay LNG Partners’ flagship business is booming. With a host of LNG export terminals coming onstream in Australia and Africa, global LNG supply is expected to grow at an annualized pace of 4.4 percent between 2011 and 2015.

After 2015, a number of new liquefaction facilities will come online in Australia, Russia and the Middle East. Most analysts also expect the U.S. and Canada to export LNG toward the end of the decade. All told, global LNG supply is expected to expand at an average annualized rate of 7.7 percent between 2015 and 2020.

Demand is rising to meet supply. In 2011 China’s LNG import volumes jumped by almost one-third. Meanwhile, Japan imports all of its natural gas supply via LNG tanker. Since the disaster at Fukushima Daiichi in spring 2011, Japan has closed the majority of its nuclear reactors for evaluation and maintenance, forcing the nation to ramp up its LNG imports. Germany’s decision to shutter all of its nuclear power plants over the next 10 years likewise bodes well for the global LNG market.

Demand for LNG tankers is booming, but most of these specialized vessels are booked under long-term deals associated with a particular export facility. Day rates in the spot market now exceed $140,000, up from about $65,000 in early 2011 and $20,000 in mid-2010.

Teekay LNG Partners’ existing fleet has limited exposure to these skyrocketing day rates, as these vessels are booked under long-term contracts. But the tight supply-demand balance in the market for LNG tankers makes fleet additions worthwhile.

In 2011 the MLP added a 33 percent equity interest in three LNG carriers last year and a 100 percent interest in three LPG carriers. All six of these vessels are booked under long-term deals that produce steady, reliable cash flows and the total value of those contracts exceeds $200 million.

In the third quarter of 2011, Teekay LNG Partners announced a joint venture with Japan-based Marubeni Corp (Tokyo: 8002) to purchase six LNG tankers from AP Moller Maersk for USD1.3 billion. This table outlines the current status of these six vessels:

Source: Teekay LNG Partners LP

The majority of these ships are booked under long-term charters, but two of the carriers — the Maersk Magellan and Maersk Methane — will come off contract in the next few years, allowing Teekay LNG Partners to take advantage of the tight market. In fact, the Maersk Methane’s contract was slated to expire in early 2012, but the joint-venture partners secured a three-year fixture for the vessel at a day rate of $130,000.

In 2012 Teekay LNG Partners’ interest in these six ships should generate $40 million in DCF, equivalent to a quarter’s worth of distributable cash flow.

Even better, the JV partners borrowed 80 percent of the cash needed to fund this acquisition, limiting Teekay LNG Partners’ required equity investment to $138 million. The MLP raised almost $180 million in a secondary unit offering at the end of 2011.

Based on management’s proposed higher distribution, units of Teekay LNG Partners now yield about 6.9 percent–well above the rate of return offered by the Alerian MLP Index. Check out my free report to uncover more MLP Investment picks.

For many Master Limited Partnerships, such a thin coverage ratio would be construed as a red flag. But Teekay LNG Partners’ contract-backed income stream limits its exposure to prevailing commodity prices or economic conditions. In fact, management disclosed plans to increase the MLP’s quarterly distribution by 7 percent, to $0.675 per unit, in the first quarter of 2012.

Teekay LNG Partners owns a fleet of 20 ships that transport liquefied natural gas (LNG), five vessels that carry liquefied petroleum gas (LPG), and 11 conventional oil tankers. All its existing ships are contracted under long-term time charter arrangements at fixed day-rates; the MLP’s LNG carriers have an average of 16 years remaining on their fixtures, while the average outstanding contract for its LPG and conventional oil tankers stands at 15 years and 10 years, respectively.

Day rates for oil tankers continue to languish. Although demand for these vessels remains solid, a glut of newly constructed vessels has led to an oversupply of capacity, depressing day rates to levels that make it difficult for many operators to turn a profit. These headwinds, coupled with declining ship values, have forced General Maritime and a number of tanker owners to declare bankruptcy. Read more on the tanker industry.

But these headwinds won’t push Teekay LNG Partners on the rocks; conventional oil tankers only account for a small percentage of the firm’s DCF, and most of the MLP’s vessels are booked under long-term time charters at fixed day rates. When the contracts on Teekay LNG Partners’ oil tankers roll off five to 10 years from now, the supply-demand balance in this shipping market should have normalized.

Meanwhile, Teekay LNG Partners’ flagship business is booming. With a host of LNG export terminals coming onstream in Australia and Africa, global LNG supply is expected to grow at an annualized pace of 4.4 percent between 2011 and 2015.

After 2015, a number of new liquefaction facilities will come online in Australia, Russia and the Middle East. Most analysts also expect the U.S. and Canada to export LNG toward the end of the decade. All told, global LNG supply is expected to expand at an average annualized rate of 7.7 percent between 2015 and 2020.

Demand is rising to meet supply. In 2011 China’s LNG import volumes jumped by almost one-third. Meanwhile, Japan imports all of its natural gas supply via LNG tanker. Since the disaster at Fukushima Daiichi in spring 2011, Japan has closed the majority of its nuclear reactors for evaluation and maintenance, forcing the nation to ramp up its LNG imports. Germany’s decision to shutter all of its nuclear power plants over the next 10 years likewise bodes well for the global LNG market.

Demand for LNG tankers is booming, but most of these specialized vessels are booked under long-term deals associated with a particular export facility. Day rates in the spot market now exceed $140,000, up from about $65,000 in early 2011 and $20,000 in mid-2010.

Teekay LNG Partners’ existing fleet has limited exposure to these skyrocketing day rates, as these vessels are booked under long-term contracts. But the tight supply-demand balance in the market for LNG tankers makes fleet additions worthwhile.

In 2011 the MLP added a 33 percent equity interest in three LNG carriers last year and a 100 percent interest in three LPG carriers. All six of these vessels are booked under long-term deals that produce steady, reliable cash flows and the total value of those contracts exceeds $200 million.

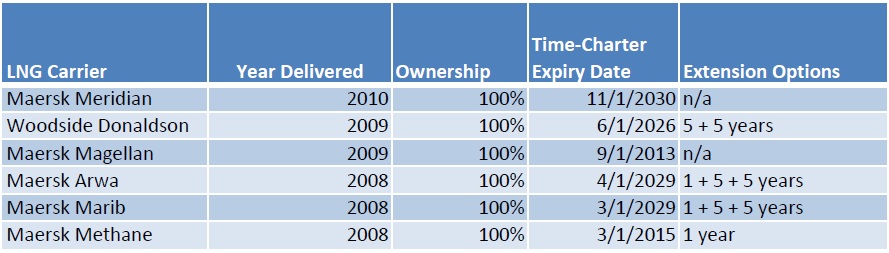

In the third quarter of 2011, Teekay LNG Partners announced a joint venture with Japan-based Marubeni Corp (Tokyo: 8002) to purchase six LNG tankers from AP Moller Maersk for USD1.3 billion. This table outlines the current status of these six vessels:

Source: Teekay LNG Partners LP

The majority of these ships are booked under long-term charters, but two of the carriers — the Maersk Magellan and Maersk Methane — will come off contract in the next few years, allowing Teekay LNG Partners to take advantage of the tight market. In fact, the Maersk Methane’s contract was slated to expire in early 2012, but the joint-venture partners secured a three-year fixture for the vessel at a day rate of $130,000.

In 2012 Teekay LNG Partners’ interest in these six ships should generate $40 million in DCF, equivalent to a quarter’s worth of distributable cash flow.

Even better, the JV partners borrowed 80 percent of the cash needed to fund this acquisition, limiting Teekay LNG Partners’ required equity investment to $138 million. The MLP raised almost $180 million in a secondary unit offering at the end of 2011.

Based on management’s proposed higher distribution, units of Teekay LNG Partners now yield about 6.9 percent–well above the rate of return offered by the Alerian MLP Index. Check out my free report to uncover more MLP Investment picks.