Diageo is a leading global producer of spirits and other alcoholic beverages.

-Seven Year Revenue Growth Rate: 7%

-Seven Year EPS Growth Rate: 8%

-Seven Year Dividend Growth Rate: 5.6%

-Current Dividend Yield: 2.48%

-Balance Sheet Strength: Leveraged but Stable

Overall, Diageo is a solid dividend stock but at the current price of over $111 for the ADR, I calculate it to be moderately overvalued.

North America

In 2012, North America continued to be the largest market for Diageo and accounted for 33% of net sales. Volume was up 2% for the year, and sales were up 6%.

Europe

Europe is the second largest market for the company, contributing 28% of net sales, but it was the only geographic area with poor numbers, with both volume and net sales being down 1% for the year. Not all that bad, considering the circumstances.

Asia/Pacific

Diageo has had solid growth in Asia, and the region now accounts for 14% of net sales. For 2012, volume was up 2% and sales were up 8%.

Africa

Africa accounts for 13% of Diageo’s net sales. For 2012, volume was up 5% and net sales were up 11%.

Latin America

Latin America accounts for the remaining 12% of net sales, but volume and net sales were up 10% and 19%, respectively.

The category breakdown is as follows:

Diageo has been divesting wine assets in favor of pursuing acquisitions in emerging markets and focusing on strengthening their core brands.

(Chart Source: DividendMonk.com)

Net sales are presented after excise duties are subtracted from total sales. Diageo’s net sales grew by approximately 7% per year over the last seven years despite the relative anchor that Europe has been on their top line.

(Chart Source: DividendMonk.com)

Earnings have grown by 8% per year on average over the last seven year period, while the dividend has grown by 5.6% per year. These figures are in pounds, so the dividend to American investors can differ from this figure.

The current payout ratio is somewhat conservative for such a stable company, at under 60%. The company pays two dividends per year; an interim dividend and a final dividend.

Overall, I view the balance sheet as rather leveraged, but not to an unsafe degree. The company has an immense and defensive global position, and takes advantage of that safety by taking on substantial leverage to increase returns on equity.

Leverage of this degree should modestly reduce the stock valuation compared to the hypothetical case where the balance sheet is very clean with little leverage. But other than having an implied impact on valuation, the leverage doesn’t appear to be an issue.

The company is the largest premium drinks business in the world, and controls more than 1/4th of the total global market share through top brands such as Johnnie Walker, Smirnoff, Captain Morgan, Crown Royal, Guinness, Bailey’s, Kettle One, and Ciroc. A host of other brands, including a small wine portfolio, round out their top brands.

Categories include “Ultra Premium”, with names like Johnnie Walker Blue Label Scotch Whiskey and Ciroc Vodka, “Super Premium”, a lower tier with names like Captain Morgan Private Stock Rum, “Premium” with the best known names like Smirnoff Vodka, Captain Morgan Original Spiced Rum, Guinness Beer, and then lower tiers of popular/value brands.

Diageo’s defensiveness comes from two primary things. The first is, the sheer scale and diversification of their distribution efforts protect against isolated problems or geographic issues. So while the market for their products in Southern Europe isn’t too solid, it’s not currently pulling down too hard on the whole business.

The second is that throughout the large geographic scope of their operations, they have several #1 or #2 brands. Some of them are the top worldwide (Johnnie Walker, Smirnoff, etc), while others are the top in their key regions. Alcoholic beverages are a category where I believe brand strength matters even more than normally. A person’s favorite whiskey or vodka or whatever their drink of choice is tends to be rather specific, and probably less likely to change than a soda brand or a food brand. This could be related to the relatively high price of the product, the memories that people have while consuming it, and the genuine differences between products.

Divesting the wine assets can make sense for such a large company that focuses on popular brands. When a person looks for a wine, they’re often interested in getting something new almost every time, and a key aspect of wine is that a given vintage is unique. A big draw for the whole experience of it is to note the subtle differences with each selection. Wine is such a broad mix, and to become semi-knowledgeable about wine means drinking many different types.

That’s not good for a global brand-based business. Buying Captain Morgan or Johnnie Walker every time due to brand loyalty is good for a brand-based business.

The company pays significant excise duties, and changes in regulation or taxation can affect their alcohol sales.

Diageo has significant albeit stable leverage, which can be a problem in a bad financial scenario. The interest coverage of around 5x should give them reasonably comfortable margins for any setbacks.

Unfortunately, I think the stock price has gotten a bit ahead of itself at $111. The dividend yield used to be decent, but now is below 2.5%.

For a stable company like this, the Dividend Discount Model can work well. The company generates low single digit volume growth and mid single digit sales growth. Over the medium term, according to the 2012 annual report, the company is targeting 6% sales growth and low double digit EPS growth (which would come due to their goal of improved margins on top of their sales growth).

With a payout ratio near 60% and a medium rate of core growth, EPS growth over the long term will likely be medium at best. After dividends are paid, the remaining cash is essentially going to acquisitions, so not all of this growth is organic. This is probably a good thing, because using the remaining cash for share repurchases at this valuation wouldn’t be very lucrative and wouldn’t boost EPS growth and dividend growth by very much.

So if we’re looking at low single digit volume growth, 6% sales growth as predicted, and a temporary burst of low double digit EPS growth followed by a more relaxed EPS growth that matches sales growth (because margin improvement would be assumed to be exhausted at that point, and the company isn’t doing noteworthy buybacks, so EPS will follow net income and net income will follow revenue), then we have a good set of estimates for the DDM. The dividend has actually been growing more slowly than EPS, but over the long term it would be expected to increase roughly in line with EPS.

Using the dollar and the ADR in my calculations on a currency-neutral basis, a two-stage Dividend Discount Model calculation with a 10% discount rate results in a fair price of about $80 if 7% annual dividend growth occurs over the next 10 years followed by 6% annual dividend growth thereafter. This figure of around $80 is approximately where I considered it to be fair last year.

To work backwards from the current $111 price, investors are either expecting something more like 10 years of 8% dividend growth followed by 7% thereafter with a 10% discount rate, or the same 7%/6% set of growth rates and only a 9% discount rate.

In other words, to justify the current price of $111, we need to either lower the discount rate (the target rate of return for this purpose) into the single digits, or assume rather generous growth rates with no margin of safety.

Diageo is an appealing and steady company, but with a yield below 2.5%, I’d want a 10+% potential rate of return in order to consider investing in the stock, and therefore view the stock as moderately overvalued.

Full Disclosure: As of this writing, I have no position in DEO.

-Seven Year Revenue Growth Rate: 7%

-Seven Year EPS Growth Rate: 8%

-Seven Year Dividend Growth Rate: 5.6%

-Current Dividend Yield: 2.48%

-Balance Sheet Strength: Leveraged but Stable

Overall, Diageo is a solid dividend stock but at the current price of over $111 for the ADR, I calculate it to be moderately overvalued.

Overview

Formed in 1997 as the result of a merger between Guinness and Grand Metropolitan, Diageo (LGE: DGE, NYSE: DEO) is the world’s largest producer of premium spirits. Headquartered in London, the company is traded on the London Stock Exchange and has an ADR on the NYSE.North America

In 2012, North America continued to be the largest market for Diageo and accounted for 33% of net sales. Volume was up 2% for the year, and sales were up 6%.

Europe

Europe is the second largest market for the company, contributing 28% of net sales, but it was the only geographic area with poor numbers, with both volume and net sales being down 1% for the year. Not all that bad, considering the circumstances.

Asia/Pacific

Diageo has had solid growth in Asia, and the region now accounts for 14% of net sales. For 2012, volume was up 2% and sales were up 8%.

Africa

Africa accounts for 13% of Diageo’s net sales. For 2012, volume was up 5% and net sales were up 11%.

Latin America

Latin America accounts for the remaining 12% of net sales, but volume and net sales were up 10% and 19%, respectively.

The category breakdown is as follows:

| Category | Sales |

|---|---|

| Scotch | 29% |

| Beer | 21% |

| Vodka | 12% |

| Ready to Drink | 7% |

| Whiskey | 6% |

| Rum | 6% |

| Liqueur | 5% |

| Wine | 4% |

| Gin | 3% |

| Tequila | 3% |

| Other | 4% |

Diageo has been divesting wine assets in favor of pursuing acquisitions in emerging markets and focusing on strengthening their core brands.

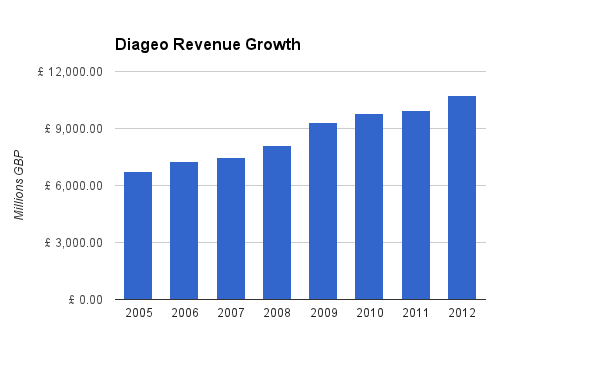

Revenue

(Chart Source: DividendMonk.com)

Net sales are presented after excise duties are subtracted from total sales. Diageo’s net sales grew by approximately 7% per year over the last seven years despite the relative anchor that Europe has been on their top line.

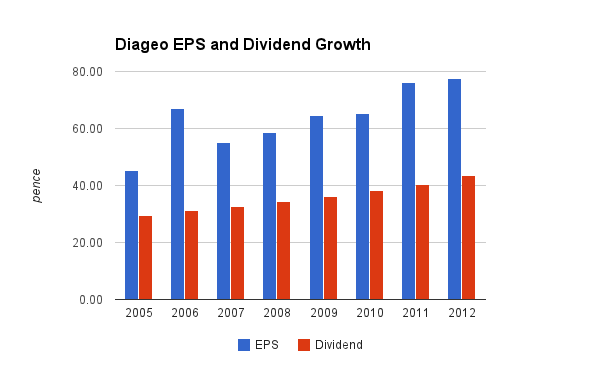

Earnings and Dividends

(Chart Source: DividendMonk.com)

Earnings have grown by 8% per year on average over the last seven year period, while the dividend has grown by 5.6% per year. These figures are in pounds, so the dividend to American investors can differ from this figure.

The current payout ratio is somewhat conservative for such a stable company, at under 60%. The company pays two dividends per year; an interim dividend and a final dividend.

Balance Sheet

Diageo has a total debt/equity ratio of a bit over 150%, and goodwill is a rather low figure compared to total shareholder equity. Total debt/income is under 4.5x, and the interest coverage ratio is around 5x.Overall, I view the balance sheet as rather leveraged, but not to an unsafe degree. The company has an immense and defensive global position, and takes advantage of that safety by taking on substantial leverage to increase returns on equity.

Leverage of this degree should modestly reduce the stock valuation compared to the hypothetical case where the balance sheet is very clean with little leverage. But other than having an implied impact on valuation, the leverage doesn’t appear to be an issue.

Investment Thesis

Diageo’s medium term goals are to grow sales by 6% per year and achieve double digit core EPS growth through net margin improvement.The company is the largest premium drinks business in the world, and controls more than 1/4th of the total global market share through top brands such as Johnnie Walker, Smirnoff, Captain Morgan, Crown Royal, Guinness, Bailey’s, Kettle One, and Ciroc. A host of other brands, including a small wine portfolio, round out their top brands.

Categories include “Ultra Premium”, with names like Johnnie Walker Blue Label Scotch Whiskey and Ciroc Vodka, “Super Premium”, a lower tier with names like Captain Morgan Private Stock Rum, “Premium” with the best known names like Smirnoff Vodka, Captain Morgan Original Spiced Rum, Guinness Beer, and then lower tiers of popular/value brands.

Diageo’s defensiveness comes from two primary things. The first is, the sheer scale and diversification of their distribution efforts protect against isolated problems or geographic issues. So while the market for their products in Southern Europe isn’t too solid, it’s not currently pulling down too hard on the whole business.

The second is that throughout the large geographic scope of their operations, they have several #1 or #2 brands. Some of them are the top worldwide (Johnnie Walker, Smirnoff, etc), while others are the top in their key regions. Alcoholic beverages are a category where I believe brand strength matters even more than normally. A person’s favorite whiskey or vodka or whatever their drink of choice is tends to be rather specific, and probably less likely to change than a soda brand or a food brand. This could be related to the relatively high price of the product, the memories that people have while consuming it, and the genuine differences between products.

Divesting the wine assets can make sense for such a large company that focuses on popular brands. When a person looks for a wine, they’re often interested in getting something new almost every time, and a key aspect of wine is that a given vintage is unique. A big draw for the whole experience of it is to note the subtle differences with each selection. Wine is such a broad mix, and to become semi-knowledgeable about wine means drinking many different types.

That’s not good for a global brand-based business. Buying Captain Morgan or Johnnie Walker every time due to brand loyalty is good for a brand-based business.

Risks

Diageo’s European market has had mild sales decreases due to the macroeconomic problems in that area. For as long as the debt and economic problems persist or deteriorate, they will act as an anchor on Diageo’s total growth prospects, since Europe is Diageo’s home base and second largest market.The company pays significant excise duties, and changes in regulation or taxation can affect their alcohol sales.

Diageo has significant albeit stable leverage, which can be a problem in a bad financial scenario. The interest coverage of around 5x should give them reasonably comfortable margins for any setbacks.

Conclusion and Valuation

Back in November 2011 when I last analyzed DEO, I concluded that the company appeared to be a decent investment at the then-current price (low $80”²s for the ADR), but that it I’d prefer to pick up shares at $75. Specifically, I stated that paying 17x earnings for a balance sheet with that level of leverage was a bit much. The lowest the stock went since then was $80, and has since steadily climbed to over $111 for the ADR. More importantly, the core company performance continued slow and steady growth, so the investment over that period has been a good one.Unfortunately, I think the stock price has gotten a bit ahead of itself at $111. The dividend yield used to be decent, but now is below 2.5%.

For a stable company like this, the Dividend Discount Model can work well. The company generates low single digit volume growth and mid single digit sales growth. Over the medium term, according to the 2012 annual report, the company is targeting 6% sales growth and low double digit EPS growth (which would come due to their goal of improved margins on top of their sales growth).

With a payout ratio near 60% and a medium rate of core growth, EPS growth over the long term will likely be medium at best. After dividends are paid, the remaining cash is essentially going to acquisitions, so not all of this growth is organic. This is probably a good thing, because using the remaining cash for share repurchases at this valuation wouldn’t be very lucrative and wouldn’t boost EPS growth and dividend growth by very much.

So if we’re looking at low single digit volume growth, 6% sales growth as predicted, and a temporary burst of low double digit EPS growth followed by a more relaxed EPS growth that matches sales growth (because margin improvement would be assumed to be exhausted at that point, and the company isn’t doing noteworthy buybacks, so EPS will follow net income and net income will follow revenue), then we have a good set of estimates for the DDM. The dividend has actually been growing more slowly than EPS, but over the long term it would be expected to increase roughly in line with EPS.

Using the dollar and the ADR in my calculations on a currency-neutral basis, a two-stage Dividend Discount Model calculation with a 10% discount rate results in a fair price of about $80 if 7% annual dividend growth occurs over the next 10 years followed by 6% annual dividend growth thereafter. This figure of around $80 is approximately where I considered it to be fair last year.

To work backwards from the current $111 price, investors are either expecting something more like 10 years of 8% dividend growth followed by 7% thereafter with a 10% discount rate, or the same 7%/6% set of growth rates and only a 9% discount rate.

In other words, to justify the current price of $111, we need to either lower the discount rate (the target rate of return for this purpose) into the single digits, or assume rather generous growth rates with no margin of safety.

Diageo is an appealing and steady company, but with a yield below 2.5%, I’d want a 10+% potential rate of return in order to consider investing in the stock, and therefore view the stock as moderately overvalued.

Full Disclosure: As of this writing, I have no position in DEO.