Our emerging markets team isn’t too keen on following crowds. Part and parcel of Templeton’s contrarian approach is traveling to places others aren’t, and thinking about the long-term potential in specific industries and companies that may not be on others’ radar screens. One place we’ve had our eye on for several years now is Iskandar, Malaysia, which has recently been attracting more investor attention. I think it could be viewed as an example of the potential we see in Southeast Asia.

Iskandar is an economic development zone covering 221,634 hectares (2,217 sq km) within the southernmost part of Johor, Malaysia, and is named after the late Sultan of Johor, Almarhum Sulton Iskandar. The region, which includes the city of Johor Bahru, encompasses an area about three times the size of Singapore and twice the size of Hong Kong. A product of Malaysian government planning, it contains five development zones and includes a vision for a city that incorporates the latest environmentally friendly or “green” technology in its buildings and landscapes, including renewable energy sources. There are hopes that by 2025, some three million people will be living in the area, according to the Iskandar Regional Development Authority.

In 2012, LEGOLAND opened its first Asian theme park within the region and a diverse variety of business, education, and entertainment venues from petrochemicals to food processing to a motor-speedway are opening or in development. It’s encouraging that demand is spread across retail, residential and industrial properties, the latter of which particularly should help bring more economic and job growth to the area. Of course, when people flock to a place, particularly foreign investors, it can drive up real estate prices beyond the reach of local residents, but we don’t see a bubble building in Iskandar at this time, and property prices are currently reasonable. In the long run, local people in Johor who currently own property could benefit from a potential rise in their property asset values.

Singapore’s Vested Interest

We think Iskandar is a good example of diligent planning and foresight on the part of the Malaysian government and that the area has now reached what could be described as a “take-off” point. Developments should start to become self-generating, creating the potential for a virtuous circle. Singapore, located across a narrow waterway, has a vested interest in Iskandar’s success. We think as long as the close cooperation between Malaysia and Singapore continues, it could be a win-win situation for both countries. Recently, the two countries announced plans to strengthen economic ties via plans including further cooperation developing Iskandar, and a high-speed rail link between Kuala Lumpur and Singapore. We think there’s great potential for intra-regional trade and development in Southeast Asia, and this is a prime example of that trend.

I’ve been to Iskandar many times over the past few years, and I’ve seen an incredible change in the area since the government built a new complex there and the LEGOLAND theme park opened, which really put the area on the map. More than a million visitors are expected to visit the park in 2013, and plans are in the works for a nearby hotel and waterpark.

Emerging Asian Growth + Demographics = Potential Opportunity

Iskandar is an example of why we find emerging Asia to be an exciting investment destination. If you look at Asian economies’ growth expectations versus the developed markets generally, you’ll see the divergence. For 2013, the International Monetary Fund projects GDP growth in developing Asia at 7.1%, vs. 1.2% for advanced economies.1 In the long run, we believe strong economic growth should eventually translate into higher earnings growth in developing Asia.

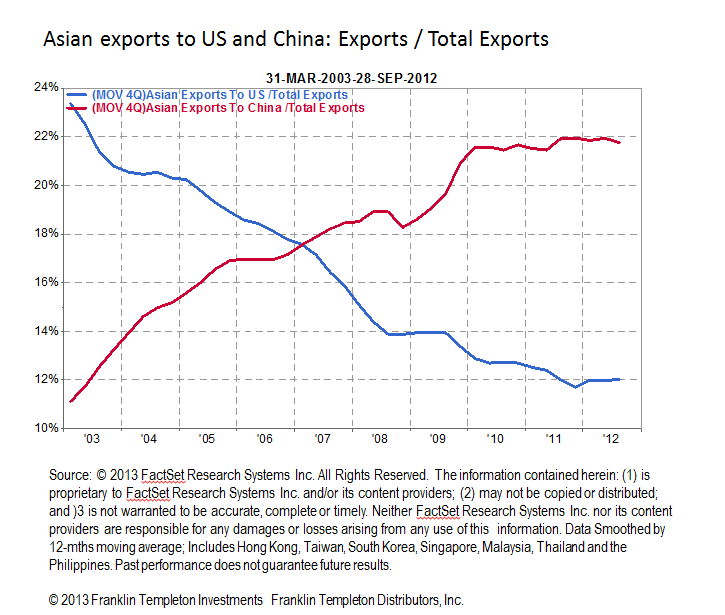

Inter-Asian trade is on the rise, which we also find to be an encouraging trend. We’re seeing increased exports from Asia to China, with exports to the U.S. falling as a percentage of the total. Meaning, there is less dependence on the U.S. for export growth, and buoyant demand from emerging economies could help offset the influence of weakness in the developed world.

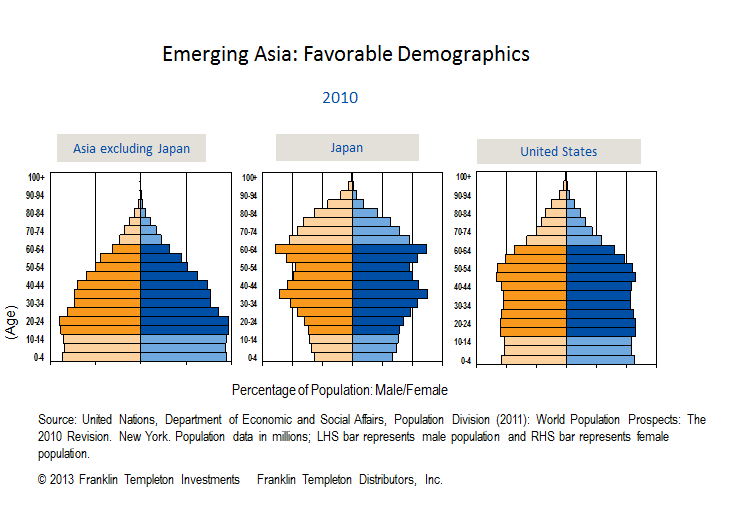

Demographics represent another interesting trend which creates a variety of potential investment opportunities, particularly related to the consumer sector. If you examine population pyramids, you’ll see that the demographics of emerging Asia indicate a great number of young people, which equates to a lower dependency ratio; that is, more people fall into working population by age so there are less dependents. As of 2010, the pyramid was skewed younger, whereas in Japan and the U.S., the elderly were a larger percentage of the total population. These trends are expected to continue diverging.

Japan Effect

An issue that could be a double-edged sword for Malaysia and its Asian neighbors is Japan’s recently more aggressive policy stance to re-inflate its economy. Some believe a weaker yen could create a so-called “currency war” as other nations try to devalue their own currencies to remain competitive in the export market. However, greater yen money supply could also drive Japanese investor flows into emerging Asia. We are already seeing stock markets around the world absorbing a lot of the impact of all this central bank money printing, and Japan is adding more fuel to the fire. So as equity investors, we view these actions as potentially positive for flows into regional stock markets, at least in the short run.

We believe the fundamentals support our optimism about emerging Asia broadly, but I have to emphasize that we don’t apply a top-down approach in our stock selection process. Iskandar is just one example of how we’ve literally seen a city grow from the ground up, and with it, investment possibilities.

The original article is here.

Iskandar is an economic development zone covering 221,634 hectares (2,217 sq km) within the southernmost part of Johor, Malaysia, and is named after the late Sultan of Johor, Almarhum Sulton Iskandar. The region, which includes the city of Johor Bahru, encompasses an area about three times the size of Singapore and twice the size of Hong Kong. A product of Malaysian government planning, it contains five development zones and includes a vision for a city that incorporates the latest environmentally friendly or “green” technology in its buildings and landscapes, including renewable energy sources. There are hopes that by 2025, some three million people will be living in the area, according to the Iskandar Regional Development Authority.

In 2012, LEGOLAND opened its first Asian theme park within the region and a diverse variety of business, education, and entertainment venues from petrochemicals to food processing to a motor-speedway are opening or in development. It’s encouraging that demand is spread across retail, residential and industrial properties, the latter of which particularly should help bring more economic and job growth to the area. Of course, when people flock to a place, particularly foreign investors, it can drive up real estate prices beyond the reach of local residents, but we don’t see a bubble building in Iskandar at this time, and property prices are currently reasonable. In the long run, local people in Johor who currently own property could benefit from a potential rise in their property asset values.

Singapore’s Vested Interest

We think Iskandar is a good example of diligent planning and foresight on the part of the Malaysian government and that the area has now reached what could be described as a “take-off” point. Developments should start to become self-generating, creating the potential for a virtuous circle. Singapore, located across a narrow waterway, has a vested interest in Iskandar’s success. We think as long as the close cooperation between Malaysia and Singapore continues, it could be a win-win situation for both countries. Recently, the two countries announced plans to strengthen economic ties via plans including further cooperation developing Iskandar, and a high-speed rail link between Kuala Lumpur and Singapore. We think there’s great potential for intra-regional trade and development in Southeast Asia, and this is a prime example of that trend.

I’ve been to Iskandar many times over the past few years, and I’ve seen an incredible change in the area since the government built a new complex there and the LEGOLAND theme park opened, which really put the area on the map. More than a million visitors are expected to visit the park in 2013, and plans are in the works for a nearby hotel and waterpark.

Emerging Asian Growth + Demographics = Potential Opportunity

Iskandar is an example of why we find emerging Asia to be an exciting investment destination. If you look at Asian economies’ growth expectations versus the developed markets generally, you’ll see the divergence. For 2013, the International Monetary Fund projects GDP growth in developing Asia at 7.1%, vs. 1.2% for advanced economies.1 In the long run, we believe strong economic growth should eventually translate into higher earnings growth in developing Asia.

Inter-Asian trade is on the rise, which we also find to be an encouraging trend. We’re seeing increased exports from Asia to China, with exports to the U.S. falling as a percentage of the total. Meaning, there is less dependence on the U.S. for export growth, and buoyant demand from emerging economies could help offset the influence of weakness in the developed world.

Demographics represent another interesting trend which creates a variety of potential investment opportunities, particularly related to the consumer sector. If you examine population pyramids, you’ll see that the demographics of emerging Asia indicate a great number of young people, which equates to a lower dependency ratio; that is, more people fall into working population by age so there are less dependents. As of 2010, the pyramid was skewed younger, whereas in Japan and the U.S., the elderly were a larger percentage of the total population. These trends are expected to continue diverging.

Japan Effect

An issue that could be a double-edged sword for Malaysia and its Asian neighbors is Japan’s recently more aggressive policy stance to re-inflate its economy. Some believe a weaker yen could create a so-called “currency war” as other nations try to devalue their own currencies to remain competitive in the export market. However, greater yen money supply could also drive Japanese investor flows into emerging Asia. We are already seeing stock markets around the world absorbing a lot of the impact of all this central bank money printing, and Japan is adding more fuel to the fire. So as equity investors, we view these actions as potentially positive for flows into regional stock markets, at least in the short run.

We believe the fundamentals support our optimism about emerging Asia broadly, but I have to emphasize that we don’t apply a top-down approach in our stock selection process. Iskandar is just one example of how we’ve literally seen a city grow from the ground up, and with it, investment possibilities.

The original article is here.