- Einhorn may present new research on GMCR at the next Value Investing Congress in September

- Multiple ways through which the company can deteriorate

- Stock is ~20% higher than where Einhorn shorted it & stock market overvaluation provides additional headwind

- Out-of-the-money PUT options are a good play on GMCR's binary return profile

I'm going to make the case here to short Keurig Green Mountain, a manufacturer of Keurig Coffee machines & branded coffee pods. David Einhorn (Trades, Portfolio) first publicly announced his short of GMCR at Value Investing Congress in October 2011, but the share price is now close to an all-time high.

This article will not contain much original research on the company itself. Why? A couple of years of experience have taught me that I am rather mediocre at doing my own research. Reading 10Ks doesn't turn me on and I have a bad tendency to read from sources that confirm my position. As the market is a zero-sum game, with a lot of effort expended by participants to attain the illusory alpha, I don't think I would add much value by myself.

Einhorn's Greenlight Capital, on the other hand, has made 19.7% net over an 18 years period. The thorough analysis he (and the analysts that work for him) does, his grasp of probabilities and focus on a margin of safety, among others, gives me confidence that a meaningful portion of that performance is due to skill, and will thus likely persist in the future (though there are reasons to believe that performance will be less going forward, including the combination of luck and skill often involved in outliers, its ~$10 billion AUM that makes it harder to beat the market and the large caps it invests in now). It hurts my ego to say it, but I think it's more rational to depend on his research than mine.

Tools like AlphaClone (see this, this, this & this), mutual fund studies (see this & this), and short-seller studies (see this) also indicate that a reasonable portion of a fund's returns can be captured through coat-tailing (without having to pay the fees). Another study shows how following public announcements on Buffett's investments would have beaten the market by 10.7%. There may be differences though between following 13Fs and short announcements.

Please read Einhorn's VIC 2011 and VIC 2012 presentations, as well as his quarterly letters (Q3 2011, Q1 2012, Q2 2013 & Q3 2013), for background info on his short-case. Great commentary can also be found from Whitney Tilson of Kase Capital, Herb Greenberg, Jesse Eisinger and fraud detective Sam Antar. See below for a summary:

A Stock with Bad Fundamentals

A number of factors could lead to the stock's collapse:

- GMCR has allegedly moved around its inventory to fraudulently increase stated sales, as well as other accounting tricks to beat earnings estimates and reduced disclosure of important metrics like number of K-cups sold.

- Since crucial patents on it's Keurig pods expired in september 2012, competitors (including multinationals like Starbucks & Nescafe) can now make their own or negotiate better supply contracts with GMCR, which threatens to reduce lucrative margins. Keurig 2.0 coffee makers introduce DRM technology, but it's a question if customers would be attracted to such a closed system, and whether competing manufacturers will hack it to be able to make their own 2.0 pods.

- Current and previous executives have a history of hyping up stocks & insiders have been selling

- GMCR has limited growth opportunities left, given that it has a 72% share of single serve market & relative expensiveness of pods vs filter coffee

- The stock is richly priced (with an EV / EBIT of 21.7) in terms of price-to-earnings multiples, and has had no free cash flow in its 'good' years

Earlier this year, Coca-Cola invested an accumulative 16% stake in the company (GMCR bought back shares at a higher price to supposedly compensate for extra shares outstanding) and is partnering on the Keurig Cold system, which makes carbonated beverages from Keurig Pods. I personally think this is a negative for the short case and introduces risk of an acquisition (however, please refer to previous mediocrity reference), but I would point out even if a value of SodaStream's (bubbly) enterprise value of $650 million was added to GMCR in a couple of years, it would be 3.3% of GMCR's current market cap. Further, that making your own soda drink vs. taking a bottle out of the fridge does not add as much value to a customer as instant fresh roasted coffee.

Now Even More Overvalued

At Einhorn's first presentation in October 2011, the share price stood at $92. After a huge fall to a bottom of $18, it has now gone up again close to an all time high at $120.

Einhorn appears to have been adding to his shorts since Q4 2012 (at least in Greenlight Re portfolio), and he noted that he added to GMCR in Q3 2013 (at ~$80). Since shorts (apart from puts) are not disclosed in 13F filings, we can't pin down his average price, but let's conservatively assume that it is around $100.

This means ~3 years after Greenlight's first shorting GMCR, you can short it yourself at a 20% higher price and with the company in an arguably more fragile state due to accumulated earnings overstatements, patent expiration and increased competition.

Short-seller veteran Jim Chanos (Trades, Portfolio) has also independently gone short GMCR. In his smaller hedge fund, this is a pairs trade with Starbucks, so as long as he reports SBUX in 13Fs he likely still is short GMCR. By the same logic, we can say he has likely been short GMCR at least since 30 september 2012, for which the first filing of SBUX appears, which in turn implies that he must have decided that GMCR was a good short at a price far below today's $120.

I can't find any meaningful stakes in GMCR by good value investors, apart from investments made by tiger cubs Lee Ainslie and Steve Mandel in 2012, possibly sold at at loss.

With Bullish Sentiment

I also personally think that there has generally been a complacent, optimistic sentiment on GMCR this year (though this is subjective and prone to confirmation bias). Searching through the internet, contrary to late 2011 and early 2012, I can find little negative publicity (apart from Chanos' interview). In my view, Motley Fool is the prime example of this stance. StockTwits today shows a 92% bullish sentiment.

Analyst recommendations consensus is also "overweight". Not that analysts are inherently inferior stock pickers, but I would argue seeing these factors together indicates an overbought stock.

Source: MarketWatch

Finally, it has been a tough market for short-sellers in the past two years. Speculative growth stocks like GMCR, HLF, CMG and TSLA as well as in other areas like biotech, 3D printing, apps and social media have forced some to cover. I would argue that these tend to be the most profitable times to start shorting the high-flyers yourself.

In an Expensive Stock Market

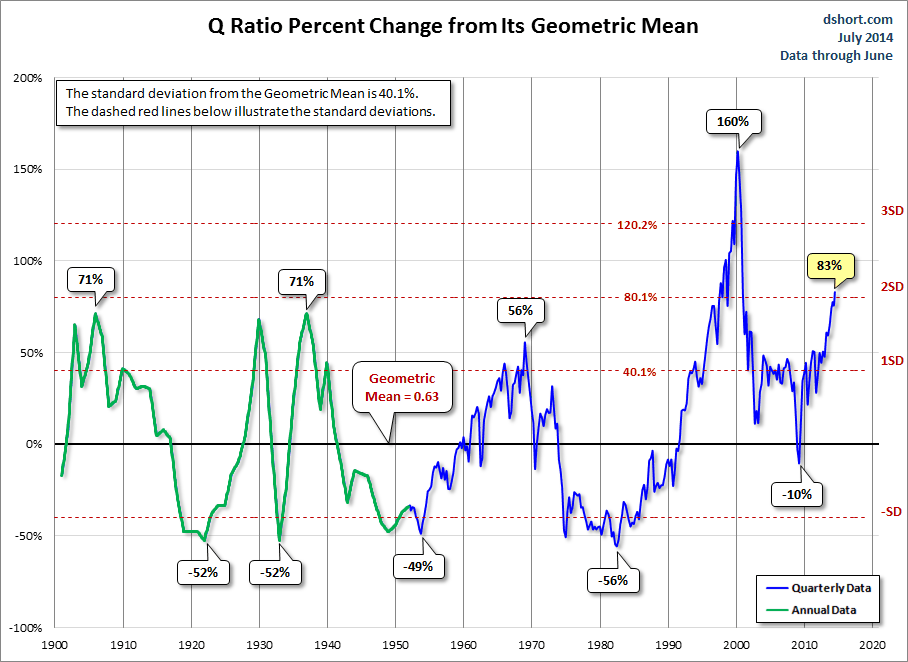

Using Tobin's Q, which appears to have been one of the best valuation-based predictors historically (see this & this), the stock market (excl. financials) is around 83% above its geometric average valuation (credit to Doug Short). Historically, this resulted in an average return of -1.03%.

(click to enlarge)

Source: Doug Short

One can make the case for the use of a range other indicators, such as market/GDP or GNP, CAPE (better yet - CAPER), Crestmont PE, GMO's 7 year predictions or Alpha Architect's Complicated Forecasting Process, or some combination thereof, or you could listen to Ray Dalio (Trades, Portfolio) saying that we will have 4% returns in the next decade. They all tend to converge though around a low to negative single digit number.

This means I think the stock market has a headwind which is a positive for our short.

However, these indicators tend to be most predictive for a period of around 7 to 10 years. Go out one or two years, and you've only slightly increased the chance that the stock market will do less well at its current valuation. Stock market turning points are notoriously difficult to predict. I have seen John Hussman (Trades, Portfolio) predict a recession in may 2010, along with John Mauldin, and then write that the market is Overvalued, Overbought and Overbullish ever since 2011. Likewise, Andrew Smithers used Tobin's Q in part to say that there was a good chance that the market wouldn't go up more, in November 2009. This doesn't mean that these are bad investors (quite the opposite), but that complex and adaptive stock markets are easily predictable only in hindsight.

I would also point out that great investors like Howard Marks (Trades, Portfolio), Warren Buffett (Trades, Portfolio) and David Tepper (Trades, Portfolio) have either argued that the market is not in a bubble yet or think it will continue on for a while.

There is a short-term metric however, that seems to be suggesting a market correction in the latter half of this year, which is Richard Duncan's Liquidity Gage, a measure of how much liquidity is pumped into the US economy.

Note: unfortunately, as I don't have a subscription, this is the latest update I could get.

Source: Richard Duncan Economics, March 2014

While I think Richard Duncan sometimes uses hyperbolic narratives, it does seem that the lowering of short-term interest rates and iterative QE by the Federal Reserve has facillitated (Note: Bridgewater requested original article to be withdrawn) the rises in asset prices in the last 15 years.

The Federal Reserve's taper, and ensuing loss of liquidity, means to me a somewhat higher chance of a significant drop in stock prices by the end of this year.

Source: Richard Duncan Economics, March 2014

With A Catalyst

Ever since Allied Capital in 2002, Einhorn's short presentations have tended to solicit unusually large stock drops. They seem driven by speculation, because there are plenty of other performing short-sellers out there who don't get this level attention. It appears to me to be largely caused by a combination of Einhorn's reputation with a positive feedback loop of speculators anticipating big drops, based on past instances.

I've made a table now of Einhorn's shorts and their day's return (based on internet sources) when he presented them (1 month returns after the presentation would give a better picture, but I don't have the data).

| ||||||||||||||||||||||||||||||||||||||||||||

Note: I've ignored shorts in Einhorn's 2012 Ira Sohn presentation, for the reason that he was all over the place.

Green Mountain's short drop on VIC 2012 and immediate reverse back up was a doozy and marked a bottom. Nevertheless, I would argue that at today's elevated price and with the possibility of a GMCR-only presentation, with new, relevant research, the impact would be greater.

A number of factors point to the possibility that Einhorn will make another presentation about GMCR at VIC 2014 New York on 8 - 9 September.

1: Einhorn has regularly presented at VIC New York (not at any other VIC location, which makes sense as Greenlight is New York-based, about 20 min. away from this year's location), in 2006, 2007, 2009, 2010, 2011 & 2012. As far as I can tell, VIC 2011 & 2012 have been the only public conferences where Einhorn has presented on GMCR (though he answered a question on it at CIMA).

2: This is what he mentioned in Greenlight's Q1 letter to investors:

"Our Keurig Green Mountain (GMCR) short, which jumped from $75.54 to $105.59, was our only significant loser. The company announced a major strategic partnership with Coca Cola. We have lots to say about this, but we'll defer that discussion to another time and, perhaps, another format."

"Another format" suggests he might do his regular thing of presenting at a conference, but it could of course also be a self-organised event, webcast, article or interview.

In last week's Q2 letter, Einhorn remained hush, writing only the following:

"Finally, there's Keurig Green Mountain. We will again keep our thoughts about GMCR and Coca Cola's minority investment (with rumors of a possible takeover) to ourselves."

To me, this suggests that Greenlight may have accumulated a large amount of new research after VIC 2012, that is more suited to being presented in a lengthier / public format.

3: The block below is displayed on the right side of the VIC 2014 webpage.

"More to come" suggests there would still be space for a high-profile investor like Einhorn. At the bottom of the speaker page it also says the following: "Many more speakers to come. Check back often! " (though maybe they've just forgotten to remove these texts).

18 speakers have been listed so far. Last year's New York congress had 25. This year's and 2013's Las Vegas congress had 21 & 26 respectively.

Whether these are representative though of this year is another question as the VIC NY in years before that (in order of newest to oldest) had 14, 16, 16, 18, 16, 17 & 17 speakers respectively, so there's no clear growth trend there.

Also notable is that he was late to enter for his VIC 2011 presentation (see Wayback Machine's before and after, he was announced 20 days before), as well as in 2006 (62-69 days before), though not in 2007, 2009, 2010 or 2012.

Putting all of this together as well as an incentive for Einhorn to disclose his research on a long underperforming short, I'm going to say there is a 40% chance that Einhorn will present a big fresh slide deck on GMCR at VIC NY 2014. Seeing that there are still 41 days left, and using 20 days as our lower bound, we should see within the next 3 weeks whether Einhorn is joining the congress.

Of course, using this as part of my investment thesis makes me no different than the speculators mentioned above. However, I'm not going to be such a value puritan to leave this aside.

Naturally, another catalyst could be dissapointing earnings results on quarterly release dates, including the one upcoming on August 6.

With a Binary Return Profile Suited for Puts

I think GMCR's future appears to resemble a binary return profile (a herding panic ensues after Einhorn makes an impression / fundamentals deteriorate OR the stock keeps chugging along / Coca-Cola acquires it) and I think this can be played well with out-of-the-money PUT options (if the stock goes up 50% your loss remains limited to the price of your options, but it's a multi-bagger if it goes down a lot). Mystery investor Quoth the Raven has done great research on Herbalife, and now has an interesting article on GMCR being able to go both ways.

The other advantages of PUTS, compared to traditional shorting is the way it can protect you from negative tails and Black Swan events (e.g. huge market crisis that hasn't happened before), and I think this isn't unwelcome with the decades of debt build-up Western economies put unto themselves and the danger of complex societies collapsing. These are all tiny probability, huge outcome events and thus difficult to weight properly, but I think it's sufficient to say these characteristics add some value.

Personally, I've bought a range of out-of-the-money PUT options at a strike price of $25 - $80 with expiration dates of jan 2015 and later. I want to emphasise though that this is a risky proposition, with a significant chance of being wiped out completely.

That is Not At All a Certain Short

A lot of things could happen that would mess with this short, so I'll mention a few risks / negatives I've come up with below:

- Shorting is generally expensive

Generally, shorting appears to be done in some part to reduce portfolio volatility and market risk, and often yields less return than longs. I think its more complicated and therefore requires an additional, specialized skill set, and listening to Buffett's or Munger's commentary (less applicable to options) doesn't make me any more optimistic.

As mentioned, I'm shorting GMCR with PUT options. I don't know much about how to short short the traditional way, and it scares the hell out of me.

Options can be expensive, as there are big players on the other side, and PUT options seem to tend to have worse return / loss characteristics (starting with returns being capped) than CALLS. I've read some explanation about people being more averse to losses / wanting portfolio insurance, but this is quite beyond me.

Psychologically, buying a lottery ticket that can either go up 50 times or leave you with nothing (the latter of course happening most of the time) can be dangerous (in terms of taking more risk than is good for you). I know about myself that I'm quite drawn to this, and it has an eerily similar feeling to gambling.

GMCR's PUTS also appear to be more expensive in terms of stock / PUT price of similarly out-of-the-money options (percentage-wise) compared to shorts of other reputable short-sellers (I'll add a table later comparing them). I don't use Black-Scholes or other volatility-based valuation methods, so I'd be glad if someone could enlighten me there.

Another question would be why Einhorn isn't shorting GMCR with PUTS himself, according to 13F filings. Surely, Einhorn would be a lot better at judging this? An argument could be made that Einhorn morally / reputationally can't buy a heap of PUTS just before he gives a presentation. And perhaps the long-term value philosophy (hold it till it mean-reverts), leaves some blind spots. Still, this doesn't satisfy me, and Jim Chanos (Trades, Portfolio) has also mentioned PUTS being expensive.

- Market sees something Einhorn doesn't

The stock price being at this level indicates investors at the other side believe something that Einhorn doesn't believe. Einhorn is known for first investigating opinions of investors before making his own, differentiating case, but he could still be wrong, as he has been in the past.

- Einhorn gets out of position before it's known to us, leaving us shorting something that he is no longer keen on

- Keurig Cold does better than expected

- People really buy Keurig 2.0 / competition stays idle

- International expansion helps sales

- Scary case - Coca-Cola buys company

Continuing in this trend, there's a distinct possibility that much larger Coca-Cola takes over GMCR for new growth opportunities. This would likely not be at a large premium, I think, so cause only some loss for short-sells - but the entire position would be wiped out with out-of-the-money PUTS. Einhorn explains in his latest letter how this is an ideal environment for big companies to make dumb acquisitions.

But Is Rare Enough that I'm Betting Big

Feel free to ask questions or give feedback. I'd also appreciate substantiated arguments against my thesis. :-)

Note: For full transparancy, I made a couple of edits within the week after the July 30 upload, including adding the Einhorn stock drop table and when he was announced for previous presentations. On August 5, I added Richard Duncan's Liquidity Gage section, so after the S&P had fallen 2.5%, though I had been thinking about this before the article. Further updates I will post in new articles.

As mentioned, I own out-of-the-money puts on GMCR, which may bias my analysis somewhat.