As of my writing about Continental Building Product (NYSE:CBPX), it has already risen more than 3% today. I would like to further present my analysis about the company's business and valuation to show why CBPX deserves to trade an additional 30% higher.

Company Overview - Favorable Industry Dynamics

CBPX is a manufacturer of gypsum wallboard focusing its business in the eastern Unite States. It also manufactures and sells complementary finishing products for the new residential, repair, and remodel, and commercial construction markets.

Source: Company Presentation

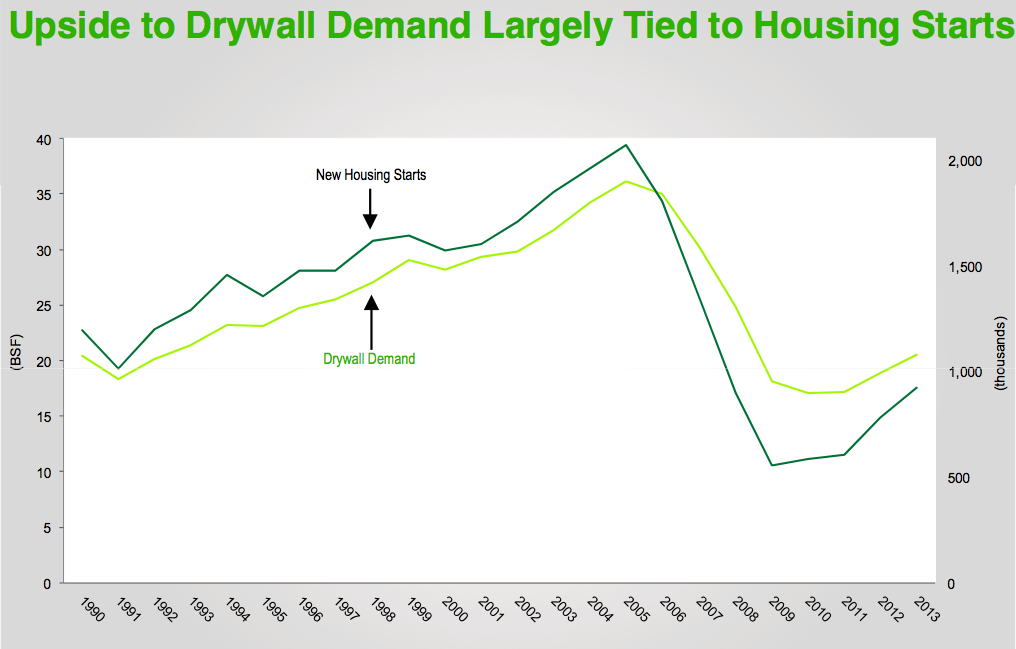

As shown above, the demand for drywall is highly correlated to the housing start. With the housing start still has plenty of room to advance, there should be good growth potential for the demand of drywall, which will greatly benefit the sales of CBPX.

(click to enlarge)

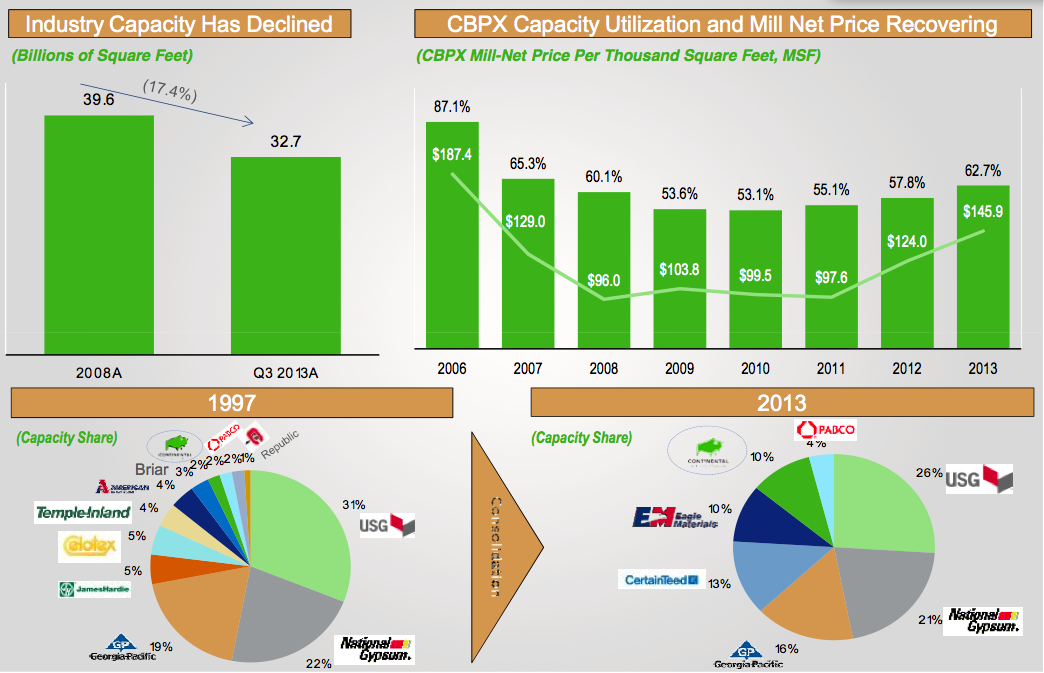

Source: Company Presentation

Other than the expected growth demand, CBPX also undergoes a favorable industry transformation. There have been consolidations in the drywall industry since 1997. CBPX has grown from 2% market share to 10% as of 2013, and most marginal competitors have already left the industry resulting in CBPX ranked as the 6th largest industry player.

In addition, the industry capacity has shrunken from 39.6 billions of square feet to 32.7 billions of square feet. This helps industry players to gradually increase their prices as illustrated by the chart above of the title named "CBPX Capacity Utilization and Mill Net Price Recovering." The shrinking number of industry players and gradual net price recovery are the tailwinds for CBPX.

CBPX has highly focused on operational excellence. It has right sized the company by reducing its headcount by 35% from 2007 to 2013. Furthermore, it invested $500 million in the state-of-art manufacturing facilities and closed down inefficient ones. This resulted in lower energy consumption per MSF by 16% from 2007 to 2013. Another critical component for CBPX to generate excellent operational is that its plants are near raw materials and major markets. Its plants has close proximity to major metropolitan areas allowing CBPX to offer same-day delivery service to many of its key metropolitan markets. This kind of superior service also enables CBPX to secure long-term contracts to effectively procure raw material inputs with favorable terms.

Management

Source: Company Presentation

One important take-away from the above is that most senior managers, including the CEO, have at least a decade of experience with CBPX. This is a great testimony to the continuity of the management success, especially for the management team to go through the most serious downturn in 2008. With the expected industry shifting to CBPX favor, I expect much more achievements for the management team and an appreciation in share price to reward its shareholders.

Valuation

Based on Yahoo Finance's expected $1.33 EPS in 2015, CBPX trades at approximately 10x PE multiple. If CBPX can trade close to the average of its peers' PE multiple of 13x, it has at least 30% upside potential. It is also worth mentioning that the 52 weeks high of CBPX is $20.4. If CBPX trades back up to its previous high, there will be a 42% upside potential.

What's more, CBPX has high capability to convert operating cash flow to free cash flow. The reason is that CBPX has already invested over $550 million in capex since 2003 in the sate-of-the-art manufacturing facilities. Hence, the expected capital expenditures will be around $6-7 millions in the near future. As the net income will grow with increasing industry demand and appreciation of drywall price, the expected free cash flow can rise as high as $75 million in 2015.

Although CBPX has about $430 million debts, the expected $150 million EBITDA in 2015 put the net debts/EBITDA to a manageble 3x multiple. With $413 million debts maturing in 2020, there are 6 years for CBPX to pay down its debts, and I believe that CBPX has sufficient free cash flow to cover its interest payments and pay down its debts on schedule.

Risks

First, any economic slowdown will adversely affect CBPX, and the uncertainty in the housing start recovery will pose additional risk for prospective investors. Second, CBPX has significant leverage with sizable debts, but the risk has been reduced by the fact that most of the debts will not mature until 2020. Third, if there might be any price war in the drywall industry, the profitability of CBPX will be significantly reduced. Nevertheless, since the industry has recently been consolidated with fewer players, there is no expectation for price competition in the near future.

Guru Ownership

Source: Gurufocus

Only one guru, Steven Cohen (Trades, Portfolio), has held 83k shares according to the latest filings. With relatively little buy/sell information in the guru section, investors cannot gain too much insights from the guru ownership.

The Bottom Line

CBPX is a cyclical business subject to the health of the housing market. What is most attractive reason to buy CBPX is that the pricing power of all drywall manufacturers has already been increased and forecasted to continue due to the industry consolidations and the rising demand from housing recovery. In addition, CBPX has done a lot to improve its operational efficiency, including reduced energy consumption, lower headcounts, and state-of-the-art facilities with minimal expected capital expenditures in the near future. With the 30% upside potential, CBPX should be able to trade at least on par with its peers without considering all the positive self-initiated improvement from CBPX. For risk-tolerant investors, CBPX should be an investment opportunity not to be overlooked any more.