My approach to investment is to first identify a good business and then assess what is a reasonable valuation for the business. In general, I will come across some near-term risks, which cause my target companies to trade below my targeted valuation. For some of my targeted companies, I can anticipate whether the near-term issues can be resolved soon. For some others, I might not know whether the near-term issues will be resolved. However, the valuations sometimes have already reflected a good degree of negatives in the stocks. Today, Hanger (NYSE:HGR) is one of my targeted companies under the latter scenario. My analysis illustrates that HGR trades close to the bottom range of its historical valuation metrics, and HGR is a very solid company with good demography macro trend in its favor. For high-risk tolerant investors, I believe that HGR should be able to navigate through the current tough medical environment and the auditing issues. With patience and an eye to the long-term horizon, HGR should be able to reward its shareholders with more than 38% potential returns.

Business overview

Hanger, Inc. provides orthotic and prosthetic (O&P) patient care services, distributes O&P devices and components, manages O&P networks and offers therapeutic solutions in the United States. It operates in two segments:Â Patient Care (83% of sales) and Products & Services (17% of sales). HGR has a history dating back to 150 years ago. A history timeline from the company website can give more details about how HGR evolves over time.

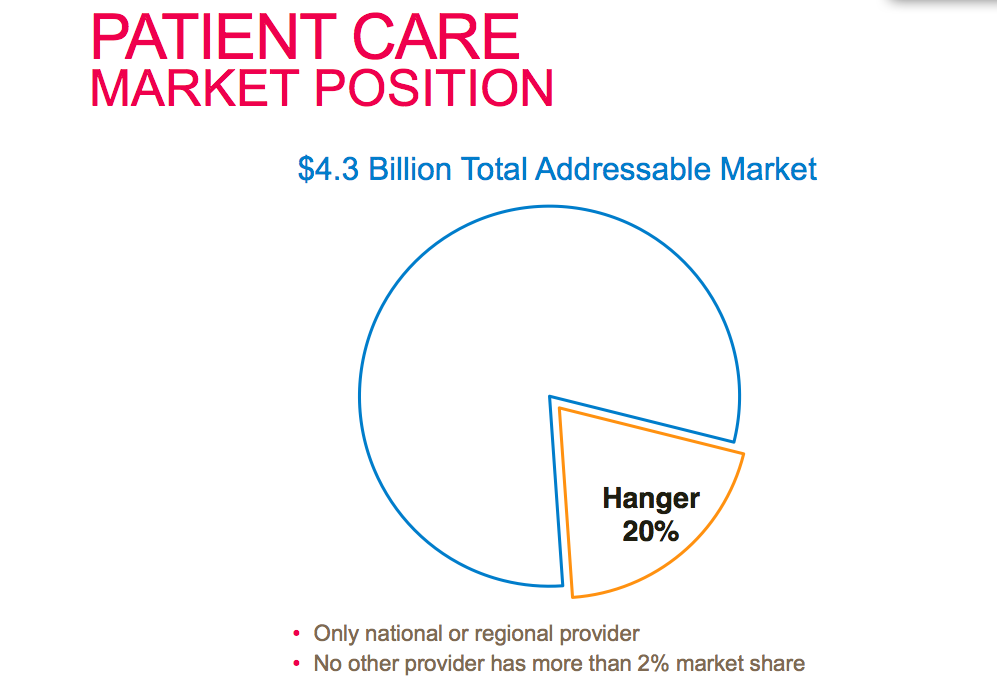

Nevertheless, what catches my attention is the chart below. HGR has already taken 20% of the patient care market while none of its competitors has more than 2% market share. As a market leader, HGR deserves to trade at a premium to the broad market valuation. However, HGR only trades at less than 12x forward P/E multiple today, and I expect that HGR should trade at least up to market multiple of 16x P/E multiple, if not more for its market leadership position.

(click to enlarge)

Source: Company Presentation

For patient care, HGR has over 740 O&P centers in 45 states and over 1,350 O&P certified and licensed clinicians. Its service is delivered through clinics, hospitals and physician offices.

Management team

Vinit Asar, the CEO of HGR, has joined HGR since 2008. He has taken various roles within HGR and eventually became the CEO on May 21, 2012. He has nearly 20 years of extensive global experience developing new health products and service businesses. Plus, he has experience in doing acquisitions and successfully grown business organically.

George McHenry, the CFO of HGR, joined HGR in 1987. He served various roles in HGR and finally became CFO on October 15, 2001. Nevertheless, he has announced plans to retire at the end of 2014 after a successor is found.

Positive outlook

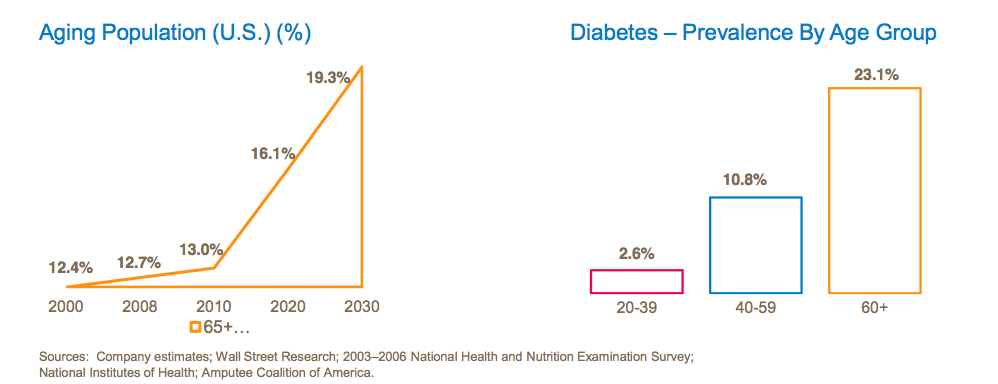

(click to enlarge)

Source: Company Presentation

In the near term, HGR is facing volume challenges since heightened payer scrutiny and lengthened pre-authorization requirements delay revenues from being realized. However, the work backlog remains healthy. Plus,the long term prospects of HGR business look bright. As we can see from the chart above, there is a favorable aging demography trend for HGR. The aging population will reach 19.3% in 2030. The older the population is; the higher the probabilities they are diabetes patients with the need for O&P services. Therefore, HGR should be able to enjoy the long runway of healthy growth based on aging demography for the next twenty years.

Valuation

(click to enlarge)

Source: GuruFocus

HGR used to trade between 12x P/E and 20x P/E. I would like to take an average and assume 16x P/E multiple for my target price. With $1.95 EPS in 2015, my target price of HGR is $31.5, implying 38% upside potential. Not to mention that HGR used to trade at 20x P/E multiple, if HGR can resolve all the risks, which I will discuss in the risks section below, HGR will likely return to its 52 weeks high of $40.

From another perspective to verify whether $1.95 EPS is attainable, I would need to first assess the possibility of the projected 2015 revenue of $1.13 billion, which implies 6.6% growth from $1.06 billion revenue in 2014. Based on the historical 8.6% CAGR revenue growth since 2009, I believe that the $1.13 billion sale in 2015 is achievable.

Source: Company Presentation

Historically, the net margins are 6.1%, 6.5% and 5.9% in 2013, 2012, and 2011 respectively. The average of the three years' net margins is 6.2%. Combining $1.13 billion revenue and 6.2% net margin, I calculate approximately $70 million net profit. With 35.47 million outstanding shares, the 2015 EPS comes up to be $1.96, which confirms that $1.95 expected EPS in 2015 is achievable.

As we know that $1.95 EPS in 2015 is highly attainable, I am positive that my target price of $31.5 is within reach for the prospective investors in HGR.

Risks

First, the CFO of HGR will retire at the end of 2014. This might cause uncertainty related to the management team, and the search for a successor might take longer than anticipated. Second, HGR is still working to remediate the material weakness in the audit report for the year ended December 31, 2013. The management team commented that they have made good progress in their remediation efforts. However, there is risk that HGR might miss future deadlines to file important SEC documents, and the audit issues can be more severe than anticipated. If so, the loss of shareholders' confidence in the accounting statements will have severe negative impacts in the share price of HGR.

The bottom line

HGR is appropriate only for high-risk tolerant investors mainly due to the uncertainty related to the auditing issues. However, I believe that HGR is an outstanding business with significant market shares in the O&P patient care market. HGR should be able to withstand the current headwinds and reward its patient shareholders with more than 38% upside potential.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.