Source: Yahoo Finance

Owens-Illinois (NYSE:OI) has significantly underperformed the S&P 500 for over a year. It is difficult to forecast that OI, as a premium market leader in the glass packaging industry, cannot even trade on par with the market. However, this kind of misalignment in performance provides great entry point for patient investors to load up stocks which are fundamentally sound and have positive catalysts, such as restructuring program to save costs. The business strengths of OI should be apparent for any prospective investors in my opinion. Nevertheless, some might argue that glass is expensive relative to other materials for packaging. Although it is a valid point, OI, as a leader, is more than capable of adjusting its costs and projecting its products as higher quality to help compensate for the costs. Several surveys indicate that consumers prefer glass; they view glass as better taste, higher quality and organic. For instance, baby foods are packaged in glass to provide the premium perceptions for parents. As there is a rising middle class in emerging markets, glass packaging should demand a good portion of the overall packaging demand. All in all, my projected more than 40% upside potential should be enough to compensate for the risk and leave sizable returns for OI's prospective shareholders.

Business Overview

(click to enlarge)

OI is a global leader in glass packaging. It has the number one position in numerous countries, including Europe, North America, Brazil and Andean region, Australia and New Zealand.

The following helps to give a snapshot of the global influence of OI.

- Founded in 1903 as Owens Bottle Company

- Merged with Illinois Glass Company in 1929 to become Owens-Illinois, Inc.

- Worldwide headquarters: Perrysburg, Ohio, USA View our locations

- $7.0 billion in net sales in 2013 View our financial reports

- 77 plants in 21 countries View our locations

- Joint ventures in China, Italy, Malaysia, the United States and Vietnam

- 22,500 employees worldwide

- 1,900-plus worldwide patents

- 49,000-plus customers in 86 countries

OI is committed to invest in innovation for long-term value. OI can assist in enhancing customer brands through new glass packaging. It has unique craft beer designs and initiates broader use of black glass. Even for the smallest component, like screw cork, OI launched trademark Helix's screw cork. This makes it easier to open the bottle and enhances customer satisfaction.

Why did OI decline?

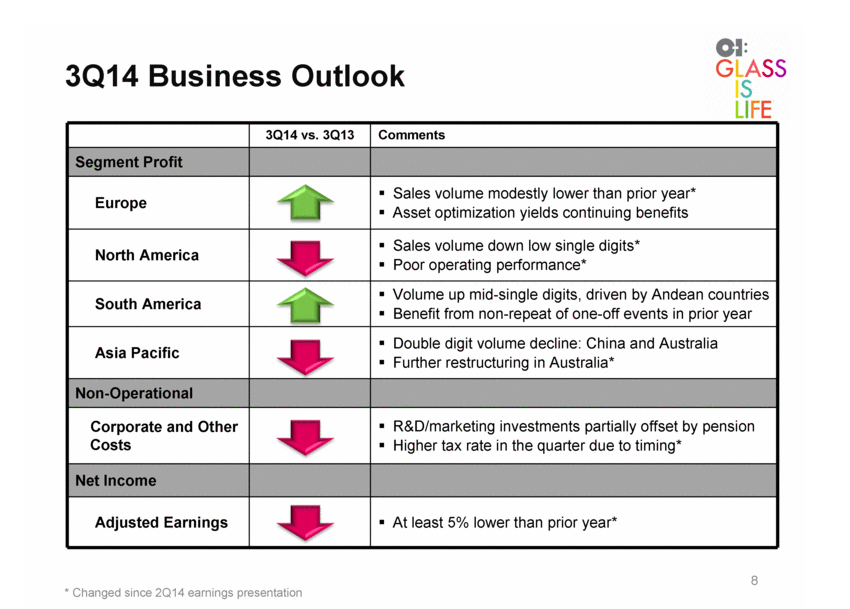

(click to enlarge)

Source: Edgar Filing

The above chart holds most of the answers. The bottom line, adjusted net income, is expected to be at least 5% lower than prior year compared to prior estimations of up approximately 10%. As I listened to today's conference call, I found that the main reason for the decline in earnings came from the sales volume down single digital in North America versus flat volume in prior estimations. Furthermore, the sales volume in Europe was previously expected to be modestly positive while the latest update forecast for "modestly lower than prior year." As OI is highly sensitive to the sales volume, the revised downward guidance clearly gives reason for OI to decline in excess of 6% today.

However, I am delighted that management is proactively acknowledging the weakness it sees in the industry. With the expectation clearly reset to the downside, I would like to stress that there are still many positive initiatives, such as its self-helped restructuring program. Plus, OI is still a leader in the glass container industry. With 40% upside potential, I believe the risk/reward profile is still favorable for OI shareholders.

Valuation

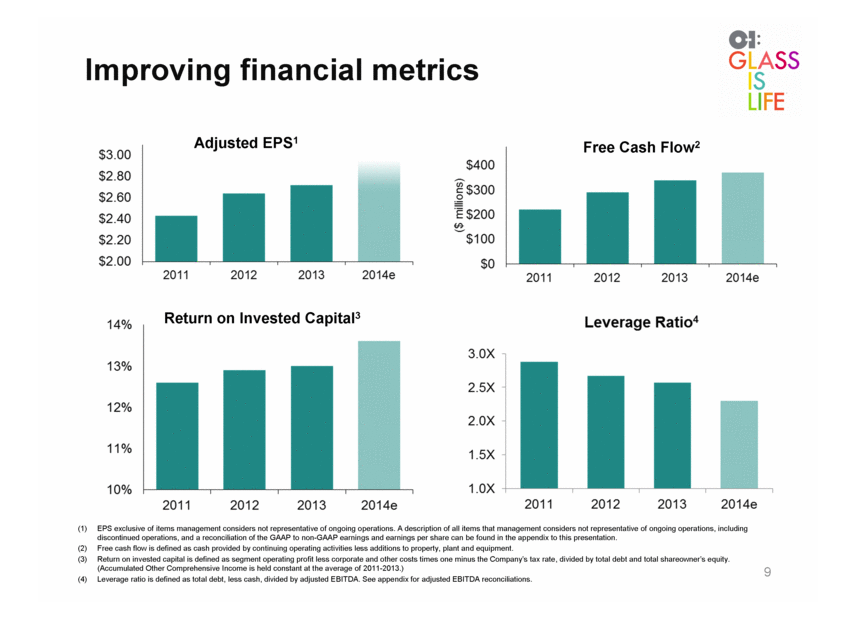

(click to enlarge)

Source: Edgar Filing

For financial strengths, OI decreased its leverage ratio from about 2.7x to today's approximately 2.4x through utilizing 90% of its free cash flow to pay off debts and the remaining to repurchase stocks. In the latest conference call, the management team of OI reiterated the repurchase target of at least $100 million. As we can see from the chart above, the adjusted earnings, free cash flow and return on invested capital are all on the uptrend since 2011. This shows the financial stewardship of OI's management team to manage the company.

In addition, the free cash flow is expected to reach $350 million in 2014, and this has been stressed in the latest conference call. Indeed, this implies that OI is currently trading at 7.2% free cash flow yield. With the ever-increasing free cash flow since 2011 showing the financial discipline of OI, the 7.2% free cash flow gives comfort for patient long term investors to hold onto OI given that the 10-year treasury yields about 2.57%.

Furthermore, during the latest conference call, OI also stated that there would be $5-$10 million less payment contribution for the asbestos payments. This helps to free up more cash flow to return back to shareholders in the future.

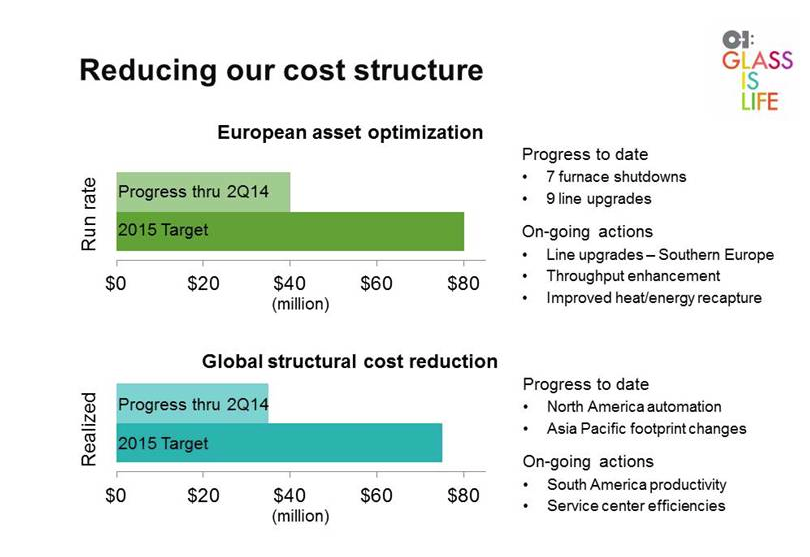

As we all know, the macro environment about whether consumers will consume more beers, which indirectly increase glass packaging sales, is out of the control of OI. However, what the management team can do is to control the costs and optimize all their resources to remain the leader in the glass packaging industry. As shown below, there has already been a clear restructuring plan put in place, and it has been on targets to meet the anticipated cost savings.

(click to enlarge)

Source: Edgar Filing

The financial discipline, 7.2% free cash flow yield, and self-help restructuring program are all solid reasons to own OI. Now, let's calculate the valuation of OI. Upon the consensus EPS in 2015 reported by Yahoo Finance, OI is expected to earn $3.34. With today's negative guidance, I reduce the 2015 EPS by 5% to $3.17. Since OI is a mature company and predicted to grow around 8.5% for the next five years, I would like to apply a more modest 13x P/E multiple to attain my target price as $41. This nevertheless still implies in excess of 40% upside potential.

Management team

The company website gives a good overview of all the senior management team members.

What catches my attention is the profile of Albert P. L. Stroucken. He has been the executive chairman and chief executive officer of OI since 2006. His long tenure serving senior roles in OI and his leadership through the recent recession in 2008 give credibility for Mr. Stroucken to continue leading OI in the future. Researching through the experience of Albert Stroucken, I found that he had extensive experience serving senior roles in related companies, such as Fuller H B (Canada) Inc and Bayer AG. With diverse experience managing different companies, It is no wonder that, when I listened to his conference call, I found that he was knowledgeable and possessed great leadership in steering the direction of the company.

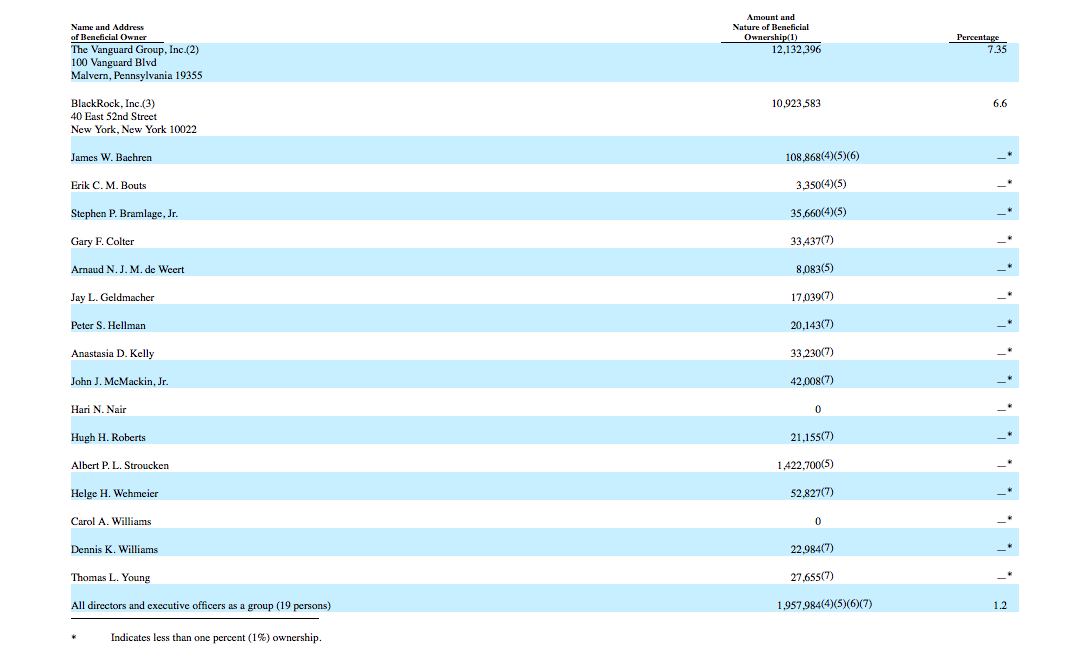

(click to enlarge)

Source: Proxy Statement

To be fair, some relevant information looks negative. For instance, the combination of ownership in OI for all the directors and executive officers is only about 1.2% of outstanding shares. This is relatively low. However, as the stock price has decreased significantly since the latest proxy statement released, I would pay close attention to any future filings about insiders ownership to see whether any officers will find values and purchase OI at today's near 52 week low share price.

Risks

First, if consumers embrace better alternatives to replace glass containers, the sales and margins of OI will definitely be adversely affected. Currently, there is no such expectation or valid reason to support such substitution argument. Second, OI might pursue dilutive acquisitions to drive away competitions; or a price war will greatly impact the profitability of OI. Third, there is foreign exchange risk. As the earnings from oversea translated back to OI for less value due to the strengthening of the U.S. dollar, the earnings of OI will be negatively affected. Forth, please refer to the risks section of the 10K to further understand the business risk investing in OI.

The bottom line

It is clear to me that OI has enduring market power in the glass packaging industry as it has had 100 years of operating history. Since OI operates in a cyclical industry, it is undeniable that OI will go through ups and downs in different business cycles. However, I believe that OI has implemented the right strategy to create shareholder value through paying down debts and returning any remaining back to shareholders through stock buyback program. As I pointed out above, the 7.2% free cash flow yield helps to give great comfort for patient shareholders to hold onto OI even in today's brutal sell-off. In addition, OI implemented a self-help restructuring program to further enhance shareholder returns. Regardless of any market environment, the earning power and the free cash flow generation capacity of Ol are very solid. For long-term value investors, today's weak guidance should help to provide a great entry point to accumulate a business leader, Owens-Illinois.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.