Over the years, Crocs Inc. (CROX, Financial) has expanded its product styles from summer-only clogs to become a footwear maker for all seasons. However, investors have run away from Crocs recently since it has missed several earnings estimates and provided weak guidance. But fortunately today's share price has already reflected a fair amount of pessimism in CROX. If we can look through the current turmoil, my optimistic scenario implies that investment in CROX can double our money. Aside from my best-case scenario, CROX can still help investors to earn respectable return under my normalized 5-year forecast. With a significant amount of cash on the balance sheet and $100 million free cash flow generation capacity, I believe that CROX is an investment worth the risk. In addition, I am happy to have such an investment opportunity alongside Blackstone Group.

Business overview

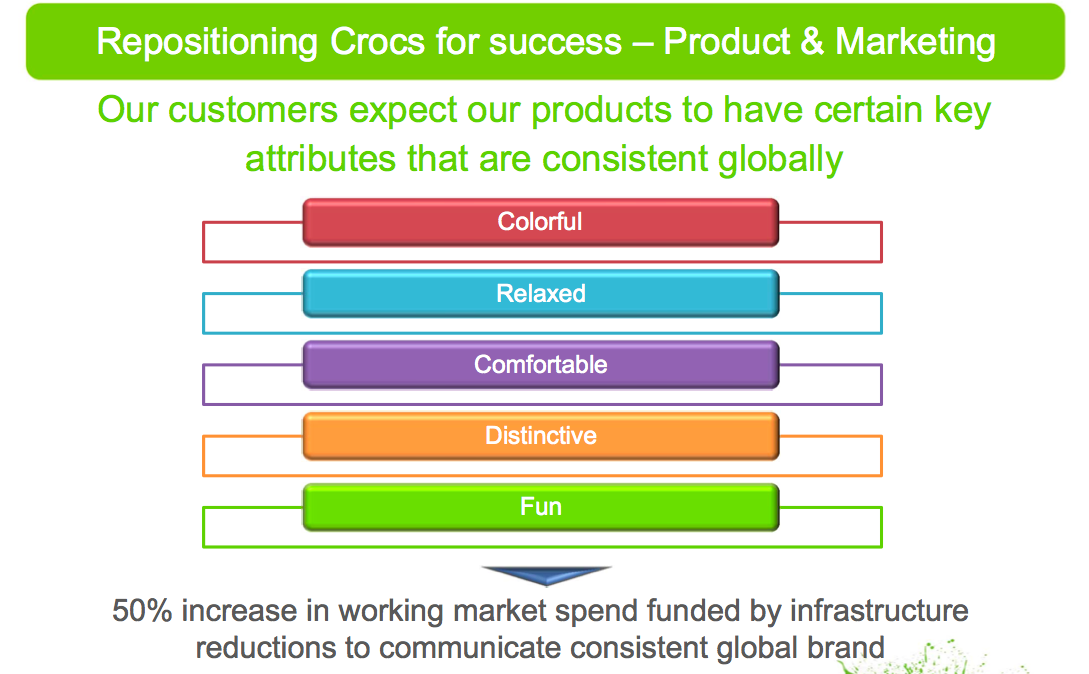

CROX is a world leader in innovative casual footwear for men, women and children. From the product and marketing perspective, CROX is a colorful, relaxed, comfortable, distinctive and fun footwear as shown below:

(click to enlarge)

Source: Company Presentation

In addition, the business website provides more details about CROX.

Turnaround plan

(click to enlarge)

Source: Company Presentation

The above provides detail about how CROX would transform itself with a specific action plan. CROX implemented a cost-saving program by eliminating 183 noncustomer-facing positions. Furthermore, CROX will close 75-100 underperforming stores and pare back its product offerings. In other words, CROX strives to reduce SKUs and streamline its operations.

SWOT analysis

I would like to share my SWOT analysis below:

Strengths:

- Pristine balance sheet combined with shareholder friendly policy: CROX has $408 million in cash and equivalents as of June 30, 2014. The cash and equivalents are about 35% of its market value. With so much idle cash, the board of directors initiated the repurchase of stocks to retire approximately 20% of the common outstanding shares last year. But please note that the majority of the cash is held overseas and is restricted for shareholder benefit with tax implication.

- Defensive EV/FCF: The Enterprise Value (about 775 million) divided by the average FCF (about 78.1 million) results in about 10x EV/FCF. With such a low EV/FCF, the downside risk should be limited.

| Â |

12 months Dec-31-2009 |

12 months Dec-31-2010 |

12 months Dec-31-2011 |

12 months Dec-31-2012 |

LTM 12 months Jun-30-2013 | Average |

| Â | USD | USD | USD | USD | USD | Â |

| Cash from Ops. | 61.1 | 104.3 | 142.4 | 128.4 | 116.4 | Â |

| Capital Expenditure | (20.1) | (31.3) | (27.7) | (39.8) | (43.1) | Â |

| Free Cash Flow | 41.01 | 72.97 | 114.68 | 88.56 | 73.28 | 78.10 |

Weaknesses:

- Recent "Miss-and-Miss" quarter earnings: Most investors and analysts got frustrated with CROX about the recent earnings and sales below guidance. However, there have been major overhauls making progress. First, CROX understands that it cannot solely rely on summer clogs, but has to diversify product lines to appeal to a variety of customers. This kind of major change will definitely require time for customers adapting to new Crocs styles. With the strong balance sheet and FCF, CROX has the financial power to wait for its customers to adapt to its new Crocs styles in the future. Second, CROX finally realized that the retail strategy negatively impacted the bottom line. In fact, the wholesale segment has grown over 40% per year since 2010. What goes wrong is that the old management team, led by previous CEO John McCarvel, focused more on the retail stores and alienated the wholesale segment. As a result, the profit margins declined significantly, and this eventually led to the resignation of CEO John McCarvel. As CROX has already implemented a new turnaround plan, the benefits of the restructuring should improve the profit margins.

- Weakness in Japan and North America: Revenues in Japan and North America have declined 9.4% YoY and 3.2% YoY, respectively. Thankfully, CROX is a global company having strong results from Asia Pacific and Europe to offset the majority of the weakness from lagging areas. As a result, the year-over-year net revenue change was a gain of 3.6% for the three months ended June 30, 2014.

Opportunities:

- Newly installed ERP technology pairing up with new shoe styles can drive sales growth higher: If CROX can utilize its newly implemented ERP technology to analyze customers' preferences, it has a better chance to find another popular shoe style to rejuvenate its brand and make its customers excited again. If this happens, it is quite likely that CROX can regain its 20%+ sales growth, just like the growth CROX used to have in 2010 and 2011.

- Having the flexibility to offer full-priced clogs in the upcoming holiday season: CROX had $191 million inventories at June 30, 2014, compared with $161 million prior year. In addition, backlog at June 30, 2014 was $206 million compared with $161 million in the prior year period. Given the rising backlog to offset the same amount of increases in inventories, CROX won't need to be promotional in the upcoming and challenging holiday season to liquidate its inventories and has the flexibility to offer more full-priced items at its discretion.

Threats:

- Polarized brand: CROX is a brand you either love or hate, partly due to clogs' awkward appearance. However, CROX is aware of the problem embedded in its brand and strive to include the comfort of its signature shoe soles with more causal and normal looking styles.

Valuation analysis:

First, I will assume that CROX can achieve 7.5% net profit margins. Margins have ranged from 20% in the heyday of 2007 to 6.2% in 2013, excepting the loss years of 2008 and 2009 during the financial crisis. As the management team stated the goal to achieve 12% operating margins, I believe that the 7.5% net profit margins are achievable given all the negative headwinds and execution risk.

Second, I will assume that sales growth will be close to 0% for the first two years and then gradually increase to about 5% per year in year 5. CROX achieved 22.3%, 26.7% and 12.2% sales growth in 2010, 2011, and 2012 respectively. However, with the negative earnings and sales revisions in the past few quarters, I would like to be conservative and lower my sales growth assumptions to take into account the current headwinds CROX face.

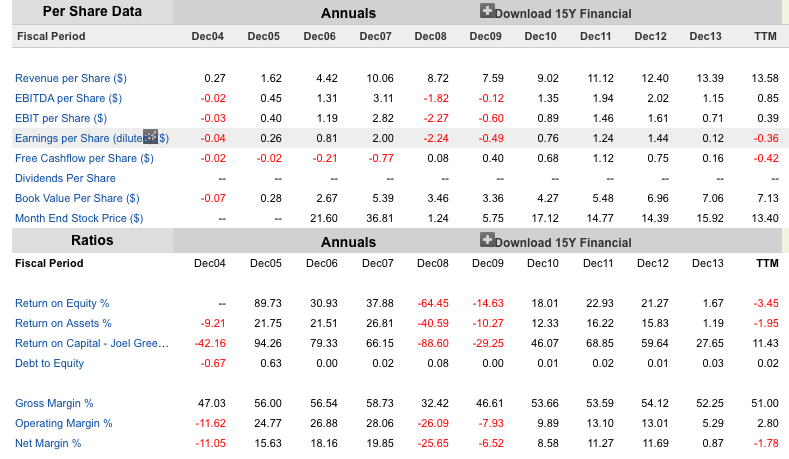

My target price will end up to be about $20. From another perspective to look at the valuation of CROX, we can study the financial data provided by Gurufocus.com below:

(click to enlarge)

Currently, CROX is trading at $13.41 while the revenue per share is around $13 per share, too. If CROX can successfully restore its normalized net profit margins about 7.5%, CROX is producing earning yields close to 7.5%. As CROX does not leverage up with debts currently, if CROX can add some debts when its business stabilizes, the rate of return for prospective investors should be in excess of 7.5%.

In the meantime, as CROX has 35% market value as cash, the financial strengths of CROX are solid. As a result, 7.5% rate of return for a company with probable turnaround opportunity charged by well-respected Blackstone Group is attractive relative to the risk being taken.

From the free cash flow perspective, CROX can generate on average around $75 million per year. It is not a stretch to assume that CROX can generate close to $100 million free cash flow when it stabilizes its operations by scaling back its retail strategy. Given the enterprise valuation of CROX is $765 million, CROX is currently trading close to 8-10x FCF, which should be attractive for investors with long term horizon. I suspect that this lucrative valuation attracts Blackstone Group to get involved in the turnaround plan with CROX. Plus, Blackstone Group is confident enough to take a 13.5% ownership stake in CROX.

Optimistic scenario

As CROX is going through a restructuring period, I understand that most investors will focus on how CROX executes on the turnaround plan. However, if we look out 5 years, CROX might be able to regain its brand popularity and earn back its 20% net profit margins, which CROX has already obtained in 2007. For any prospective investors, we might consider ourselves a chance to see CROX return to the highest margins. If that happens, CROX can earn close to $2 per share. With a premium P/E multiple, it is possible that CROX can trade up to $30 per share. To be prudent, investors should not invest just to hope for such optimistic scenario. Nevertheless, the possibility of CROX trading back up to $30 should be considered.

Management team

After the resignation of John McCarvel, Andrew Rees, a consumer brand management expert, joined CROX and became the interim CEO until a right CEO is appointed. Andrew Rees founded and led LEK's retail and consumer products practice for 14 years. He also held senior leadership roles at Reebok international.

In the search for the permanent CEO, there is uncertainty involved. However, since Blackstone Group owned 13.5% stake and held two board seats, there is a good chance that Blackstone Group will help to find the right CEO to lead CROX to profitability. Once a credible CEO with great track record is named for CROX, one big uncertainty will definitely be removed. And hopefully investors might shift their focus more onto the long-term earning potential of CROX instead of the near-term sale and margin disappointments.

Risks

First, the turnaround plan might be delayed or not achieve the anticipated benefits. This poses execution risk for prospective investors. Second, I have identified the weakness in both Europe and Japan. If the deteriorating sales trend continues, CROX might lose more and more money in those two regions without the offsetting benefits from other growth regions. Third, as a global company, CROX faces foreign exchange rate risk. Fourth, CROX is a summer brand with more sales from May to August depending upon the weather. Hence, the weather and seasonality poses additional risk for prospective investors to consider. Finally, please refer to the risks section of the 10K to further understand the business risk investing in CROX

The bottom line

I understand that there are many uncertainties involved in the investment of CROX. But given the free cash flow generation capacity and 35% cash relative to the market cap, the reward should be enough to compensate for all the risks. I personally believe that the journey with CROX will be very profitable, and I would like to invite you to be in the same shoes - er, clogs - with me and CROX.

Disclosure: I am not a securities broker/dealer or an investment adviser. You are responsible for your own investment decisions. All information contained should be independently verified with the companies mentioned, and readers should always conduct their own research and due diligence and consider obtaining professional advice before making any investment decision.