Pandora Media (P) is an Internet radio company that can be heard on smartphones, tablets, computers and car audio systems. Even after correcting by more than 50% over the last 12 months, we believe Pandora will continue to underperform the S&P 500 over the next 12 months due to the company's still-frothy valuation, its horrible price momentum and consistently negative return on equity. Additionally, the "smart money" on the street is bearish on the stock, and the company's earnings miss last quarter could very well be the start of a trend. Lastly, we don't see any big companies coming to the rescue of Pandora through a takeover offer, and the business environment is getting more competitive by the week.

In this report, we'll be outlining why investors could use the recent rally back above $16 in Pandora's stock price to close any long positions or increase current short positions. Based on traditional value metrics that have been empirically shown to predict stock returns, Pandora is still very overvalued relative to the market. Pandora doesn't have the growth profile to justify the valuation and has actually started to miss analyst estimates recently. Again, the metrics used to highlight this have been empirically shown to predict returns, and are thus are extremely important to analyze. As we go through the report, we'll provide links to the academic papers that underpin our analysis so investors can see themselves why each metric is important. Investors looking to dig deeper into academic research, can check out our post here, which outlines the major academics and their research.

Valuation breakdown

We'll start with an analysis of Pandora's valuation profile, looking at five valuation metrics each with a strong predictive ability. This is important to look at as Nobel Laureate Eugene Fama showed that "value stocks have higher average returns than growth stocks." Some people say that valuation doesn't matter for a growth stock like Pandora. But that is the entire point of empirical testing, to identify whether it has been a historically good decision to buy stocks with a similar relative valuation. Because Pandora doesn't make money, we'll start with an analysis of Pandora's valuation from a book value basis, using price-to-book as our measure. While not the best measure of value for an internet company, price/book is the most fundamental measure of value (after the price/earnings ratio).

There's not much of a margin of safety from a book value basis with Pandora trading at 5.85x book value. This is almost 50% higher than the Internet Software and Services industry group, in which the average stock trades at 4.1x book value. This industry group is significantly higher than the Technology sector average (3.3x) and overall market average (2.54x). Investors playing Pandora are betting on the stock growing at a big rate into the valuation, though it's worth knowing that the stock has a long way to go and is already more expensive than industry peers, many of whom actually make money.

At first glance, Pandora's sales yield of 27% roughly falls in line with the Internet Software & Services industry group average of 24.2%. But from a revenue basis, this industry group is one of most expensive industry groups in the entire market. Even with fears of another tech bubble, the overall technology sector trades at an average sales yield of 37%, while the overall market trades at an average sales yield of 50%. Both are much higher than the current sales yield of the Internet Software & Services group.

While Pandora doesn't earn a profit currently, analysts expect them to generate $0.20 of EPS during fiscal 2015. Using this number and the stock's current price of $16.5, we get a forward P/E of 82.5x. Keep in mind that we used the analyst consensus from Thomson Reuters, and not the Zacks consensus, which is calling for -0.35 EPS. The numbers for 2016 are slightly better for the next year, with Zacks calling for -$0.13 EPS and Thomson consensus calling for $0.51. Keep in mind that Zacks tends to be much more selective in how it builds its consensus earnings estimates, preferring to rely on a small number of high-quality analysts compared to Thomson's broad approach. Using Thomson's 2016 number of $0.51, we still get a forward P/E of 33x. This is a high number to pay for a stock that is facing intense competition and a slew of downward earnings estimate revisions.

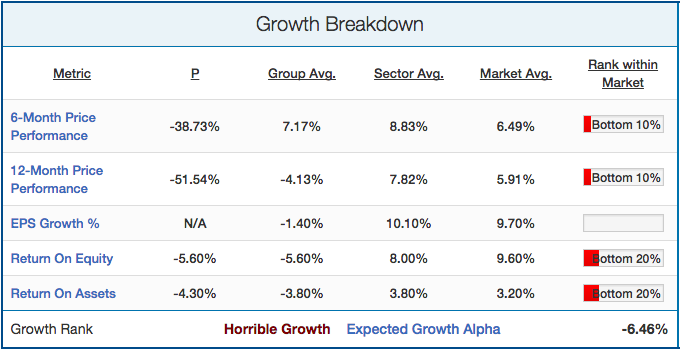

Growth breakdown

There are a variety of different growth metrics that have been shown to predict stock returns. Most important among them is price momentum. Winning stocks keep winning (based on six-month price performance), and losing stocks keep losing. As outlined in James O'Shaughnessy's book "What Works on Wall Street," EPS growth and return on equity/assets were also shown to have predictive ability, albeit to a lesser extent. Pandora's growth breakdown is shown below:

(click to enlarge) Source

Source

Pandora has severely underperformed the market recently, shedding 39% of its market cap over the last six months. This is during a time when its industry group gained over 7%, its sector gained 9%, and the overall market gained 6.5% on average. While the stock has lost 52% over the last 12 months, it hasn't made the stock cheap. At the very least, if one was to try to catch the proverbial "falling dagger," one would expect the stock to be cheap at least. The company is constantly losing money, and thus its return on equity and return on assets are both solidly negative at -5.6% and -4.3%. This actually reflects a general trend in the Internet Software industry group, which has an average ROE and ROA of -5.6% & -3.8%.

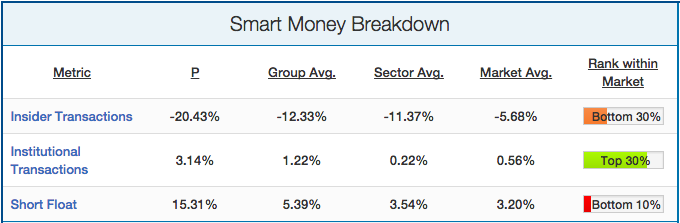

"Smart money" breakdown

In addition to value and momentum, we will also analyze how the "smart money" on the street is playing Pandora. We consider the "smart money" to be short sellers, company insiders and institutions. Each of these stakeholders tends to be much more sophisticated than the average investor and thus their transactions give good clues of what is to come. We have found loads of academic research showing that short sellers, company insiders and institutions all predict stock returns. This "smart money" breakdown for P is shown below:

(click to enlarge) Company insiders have been selling Pandora stock hand over fist the last six months, with company ownership decreasing by 20%. Again, this reflects a general industry group and overall market trend, though its particularly bad at Pandora. Company insiders know their company best, so it's clearly not a good sign that they are selling stock like this. Short interest in the stock continues to be in the top 10% decile of the market, making it one of the most shorted stocks in the entire market. Short sellers have been right so far with the stock, so it definitely makes sense to heed their warning. Institutions have slightly increased their position in the stock lately, though it's not a significantly large increase to really draw conclusions. Overall, it's clear that the "smart money" on the street is bearish on the stock and, historically it pays to follow them.

Company insiders have been selling Pandora stock hand over fist the last six months, with company ownership decreasing by 20%. Again, this reflects a general industry group and overall market trend, though its particularly bad at Pandora. Company insiders know their company best, so it's clearly not a good sign that they are selling stock like this. Short interest in the stock continues to be in the top 10% decile of the market, making it one of the most shorted stocks in the entire market. Short sellers have been right so far with the stock, so it definitely makes sense to heed their warning. Institutions have slightly increased their position in the stock lately, though it's not a significantly large increase to really draw conclusions. Overall, it's clear that the "smart money" on the street is bearish on the stock and, historically it pays to follow them.

Conclusion and qualitative analysis

Now that we've analyzed the numbers, it's time to take a qualitative look at the business environment that Pandora operates in. As we've said multiple times throughout the report, the online music marketplace is becoming extremely saturated. Everybody knows about the increasing dominance of Spotify, but Apple (AAPL), Amazon (AMZN), and Google (GOOGL) have all recently launched, or will launch music streaming businesses of their own. Apple's iTunes radio is particularly worrisome, as the company has the financial firepower (over $150 billion in cash, or about 50 Pandora's), industry brand (iTunes revolutionized music), and now talent (acquisition of Beats management team). Throw in fringe entrants like Jay-Z's WiMP among others, and its clear that the online music streaming business is about to get extremely competitive. As the business environment becomes more competitive, Pandora will have greater pressure to cut the amount of ads they show. This is because with the option of dozens of free alternatives, customers will have little patience for an ad-heavy music-streaming platform. This is crucial as Pandora generates the vast majority of its revenue from ads. This is in contrast to Spotify, which has over 25% of its total users paying.

Given that Pandora has existed for 15 years and yet still accrued a deficit north of $200 million, it becomes clear why company insiders and short sellers alike have been dumping stock. We don't see any major Tech companies coming to the rescue of Pandora with a takeover, as most major tech companies (Amazon, Apple and Google) have streaming businesses of their own. We don't see anybody big enough to take over a company with a $3.5 billion market cap that hasn't already copied its business model already.

Overall, we believe Pandora is an attractive short candidate as it has an attractive combination of expensive valuation, horrible growth profile and "smart money" bearish sentiment and operates in an increasingly competitive business environment. We give Pandora a "Strong Underperform" and expect its returns over the next 12 months to severely lag the S&P 500.