A) Introduction

Ballard Power Systems (BLDP, Financial) is engaged in the design, manufacturing, and sale of fuel cell products for a variety of different applications. We think Ballard offers a great shorting opportunity for investors due to the company's extremely weak growth profile, expensive valuation, history of missing analyst estimates, high level of external financing, and the bearish sentiment of "smart money". Our quantitative models are quite bearish on a number of other names in the fuel cell industry, such as Fuelcell Energy (FCEL, Financial), but we chose Ballard because of what we feel is an attractive entry point.

Before we begin, investors should know that we tend to have a very quantitative style of analysis and only look at metrics that have been academically verified to predict stock returns. We will provide the links to the academic papers we rely on as we analyze Ballard but investors can also get a summary of the papers here.

B) Valuation Breakdown

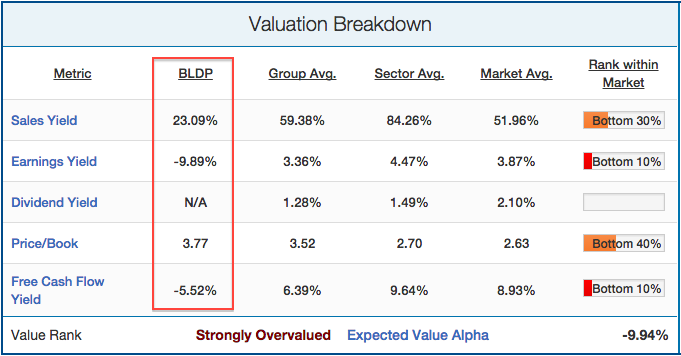

We'll start with an analysis of Ballard's valuation from a relative basis, as valuation measures have the best historical track record of predicting stock returns (see here). Ballard's valuation profile is shown below:

(click to enlarge) Source

Source

Even after a long-term decline in its stock price, Ballard still looks expensive from every measure of value. From a revenue basis, its sales yield (ttm revenue / market cap) of 23.1% is less than half the industry group (59%), sector (84%), and overall market (52%) averages. Ballard's earnings yield of -9.9% implies that its income deficits over the last 12 months are equal to one-tenth of its market cap. That's a sign of a zombie company if there ever was one. Downside is not limited either by the balance sheet, as the company's market cap is almost 4x book value. Lastly, free cash flow was also firmly negative, coming up to 5.5% of its market cap. Overall, our value model rates Ballard as "Strongly Overvalued." Holding everything else equal, we expect huge underperformance (-9.94%) from Ballard just due to the company's expensive valuation.

C) Growth Breakdown

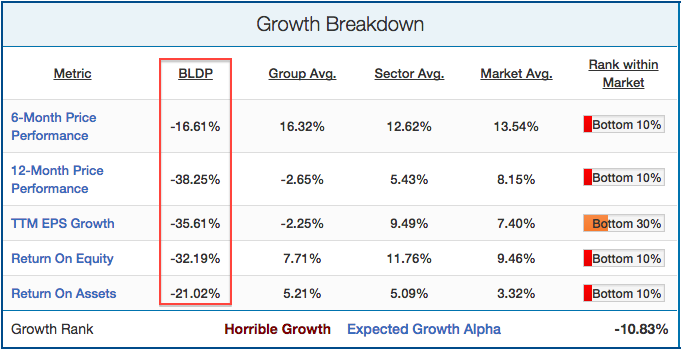

Next, we'll take a look at Ballard's growth breakdown, specifically focusing on price momentum, EPS growth, and profitability efficiency. Price momentum is particularly important, as the momentum anomaly is almost as strong as the value anomaly (see here). EPS growth & profitability also have predictive power to a lesser degree, as initially outlined in James O'Shaughnessy's seminal book "What Works On Wall Street." Companies with expensive valuations can still be good investments if growth is strong enough. Ballard's growth breakdown is shown below:

(click to enlarge) Source

Source

Even with the big spike in stock price in February, Ballard has shed 16.6% of its market cap over the last six months and 38.25% over the last twelve. This is during a time when the average stock in the market gained 13.5% over the last six months, and stocks in its industry group gained 16.3%. Clearly, the long-term trend is firmly downward for Ballard, which is not a good sign when the valuation doesn't look cheap either. EPS growth is pretty bad as well, with ttm EPS decreasing by 35.6% over the previous twelve months. Return on equity & assets are firmly negative, with ROE at -32.2% and ROA at -21%. Again, the average stock in the industry returned 7.7% on equity and 5.2% on assets. Overall, our growth model rates Ballard as a "Horrible Growth" stock. Holding everything else equal, our model sees tremendous 12-month price underperformance (-10.8%) for BLDP as a result of its poor growth profile.

D) Upcoming Earnings Breakdown

We also like to consider how a company's earnings have come out relative to analyst estimates, as we've found through historical testing that stocks that beat estimates are far more likely to keep beating them in the future. This is crucial as stocks see huge movements in their price depending on how earnings come out relative to expectations. Ballard's track record of earnings is shown below:

(click to enlarge)

As we can see, Ballard has a long history of missing analyst estimates. Last quarter, Ballard missed EPS consensus estimates by 50% and revenue estimates by 1.6%. This was its second miss in a row for both EPS and revenue. Ballard has only beaten analyst estimates in 3 out of the last 10 quarters, which is amazing when you consider that stocks, on average, beat analyst estimates 65% of the time. Ballard releases earnings next on April 28th, with analysts expecting $0.14 EPS and $13.10 million in revenue.

E) Conclusions

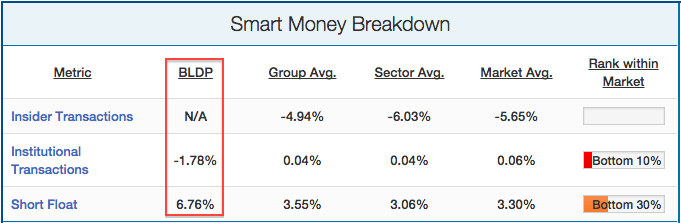

Now that we've broken down Ballard's valuation, growth, and earnings profile, we'll look at how the "smart money" is playing the stock. To do this, we'll analyze the short float and institutional transactions, as historical testing has shown both to be good predictors of subsequent future returns (see here &here). Ballard's "smart money" breakdown is shown below:

(click to enlarge)

Institutions have been selling stock recently, though to a small degree, with the institutional ownership decreasing by 1.78% over the last 3 months. Short interest is also pretty high at 6.76%, which is double the sector (3.1%) and overall market (3.3%) averages. Short sellers clearly see downside in the stock, and historically it pays to follow them when they pile into a stock.

Another warning sign is the level of external financing that the company has taken relative to its asset base. Academic studies have shown that a high level of external financing (debt & equity issuances) tends to lead to bad future returns, and vice versa. Ballard's level of external financing relative to the industry group, sector, and market averages is shown below:

As we can see, external financing over the last 12 months is equal to over 13% of Ballard's assets. This is a huge amount when the average external financing makes up less than 1% in the industry group, and less than 0.50% of the average stock in the market. Ballard is taking out unsustainable amounts of external financing that is likely to hurt the company in the future. The box below highlights our concluding summary on the stock:

In conclusion, we hold a "Strong Underperform" rating on Ballard and have it rated in the absolute last percentile of the +3300 US equities that we cover. We expect their stock price to underperform the S&P 500 by 24.68% over the next twelve months. We feel now is a good time to take a bearish position in Ballard as the company's stock price is artificially inflated in the short-term due to the divesture of the company's highly valued IP to Volkswagen (VLKAY) for $80 million, though the stock has since drifted down from the news.