Dreamworks Animation (DWA, Financial) makes animated movies and is headed by owner/operator Jeffrey Katzenberg. Through one of these detestable second share classes founders Katzenberg, Steven Spielberg, David Geffen, and Paul Allen control the vote. The company is famous for its large franchises: Shrek, Madagascar, Kung Fu Panda and How To Train a Dragon. Katzenberg is 63 years old. Tabloids (Hollywood Reporter) say he is interested in a sale. Last year two takeover discussions fell apart between Hasbro (HAS, Financial) and Dreamworks and between Softbank (SFT, Financial) and Dreamworks.

You probably think of Dreamworks Animation as a producer of animated movies and that is how I introduced it. However, Dreamworks derives its cash flow from several different segments outside of feature movies. True, these sources are somewhat dependent on the feature movie business, but not entirely. Fazal Merchant (CFO) has indicated 50% of revenue is going to come from non-feature movies in 2015. The key sources of revenue besides feature movies are:

- TV content: YouTube, Verizon (VZ, Financial) and Netflix (NFLX, Financial) deals, as well as deals in Europe and Asia

- Library: 30+ feature movies. Cash flow falls for the most part to the bottom line

- Consumer articles: Toys, licensing deals of the character IP.

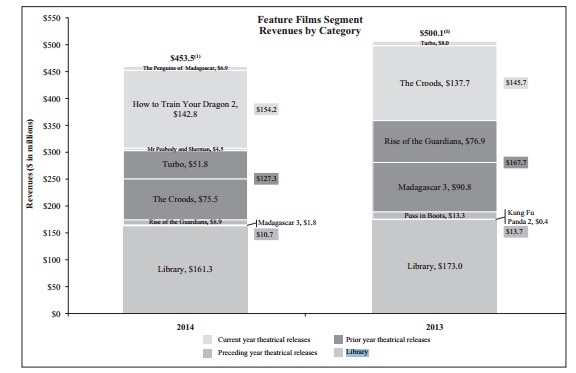

This investment idea depends on the non-feature movie revenue, which is more consistent, growing fast and not valued appropriately by the market, which focusses on the latest feature movie box office. If half of revenue over 2015 comes from non-feature movies, I expect the ratio to be more like 66% in 2017. In the graph below you can view how material the contribution of library revenue already is:

Source: Dreamworks annual report

Financial strength

Dreamworks has been in better shape financially. Producing movies is a volatile business. If you hit a blockbuster and can milk it with a couple of sequels you are swimming in dough. If you miss a couple of times, the entertainment industry looks like a terrible business to be in. Expensive production costs, and everyone and his mother in the chain is taking their cut. When movies finally hit your library and produce free cash flow unencumbered by expenses, no one wants to watch your library of flops. Dreamworks produced a string of movies with a bloated expense structure and failed to produce a true blockbuster. This put pressure on the finances and the company has engaged in major cost cutting to combat any further slide of its financial position. Production costs have decreased by tens of millions of dollars per production. Long-term debt equals $563 million which the company should be able to serve.

Management

Katzenberg has upped his involvement at the production level and is taking a more hands on approach with the animation company. The creative team has been overhauled, and he is looking over its shoulders again. Katzenberg owns a ton of stock and is heavily incentivized to see the company do well. Meanwhile, he does not appear to be one of those owner/operators not interested in a buyout. Instead he would rather see Dreamworks as part of a larger conglomerate. Softbank approached the company last year but that did not work out. Softbank’s Masayoshi Son is known to be a savvy capital allocator. Meanwhile, Katzenberg is probably acutely aware Dreamworks intrinsic value exceeds its current market price. Perhaps Softbank did not want to pay a fair price but tried to get it on the cheap?

Image: Jeffrey Katzenberg

Valuation

Currently earnings are terrible. It takes quite a bit of work to see through these and arrive at a more accurate estimate of intrinsic value. I have spent weeks looking at the company, it is one of my larger positions, and the easiest way to show the value embedded in the company is to model what earnings can look like a few years out broken out by segment.

To get to a normalized scenario for 2017, I worked out an earnings estimate by segment within the company. I left out the one-time release of the Captain Underpants movie (a special case) and a number of extremely upredictable sources of revenue; Oriental Dreamworks and a few others. Overall, I would say my earnings scenario for 2017 is on the conservative side because of those exclusions.

| Segment | Estimated Net Earnings (million $) | Multiple |

| TV | $65 | 20x |

| Consumer article | $30 | 10x |

| Library | $90 | 10x |

| Feature movie | $125 | 10x |

Source: author's normalized earnings scenario 2017 DWA

Because the blockbuster business is so unpredictable actual results can miss my estimate by a wide margin either on the upside or the downside.

If you look at Dreamworks this way it is clearly undervalued. When you apply reasonable multiples to its core segments this shows the company could easily be valued at around $3.75 billion in 2017. That is with me relying on conservative valuation multiples. The TV multiple is the only high one, because that segment is showing tremendous growth rate and there is little reason to expect it to stall. Both management guidance and independent research is indicating that high growth is likely to continue.

Risks

The big risk with Dreamworks is that it just publishes one terrible movie after another. Before Home, which did quite well, the company had a bad run with its non-sequels. That goes to show how hard this kind of thing is to predict because I watched Home (beginning to end) and it is a terrible movie.

The one good thing about box office misses is that the company regularly sells off beyond what is reasonable after box office results. So if you are interested but want to underpay, you can get lucky after a bust. With Dreamworks decreasing its number of releases per year from 3 to 2 (this year releasing just one!), this puts a lot of pressure on the movies it does release. The upside of that is that the company can be more picky in when to release its movies. A favorable release date with less competition can make all the difference.

Nowadays, a strong dollar is not good news for Dreamworks. International sales are growing faster than domestic sales. With the global infrastructure for streaming content improving this dynamic will only strengthen. Obviously, overall a global marketplace is an advantage but it does introduce currency risk. Right now Dreamworks is at the short end of that stick.

Outlook and optionality

At its core, the company derives its value from the feature movie/TV/library and consumer products segments. Especially, the library and TV segment are undervalued by the market in my opinion. The revenue generated by the library of intellectual property is dropping almost 100% to the bottom line so its size is quite relevant. The TV segment is growing like crazy and stabilizing the companies cash flows. A stable cash flow is generally valued at higher multiples.

Finally, there are a few sources of hidden value. These hidden options pose very little risk on the downside but can turn out to be incredibly relevant to future cash flows. There is so much uncertainty surrounding these options that I did not include them in my valuation analysis done earlier. These ventures produce no cash flow so it is extremely hard to tell what their ultimate contribution will amount to.

Google recently set up YouTube premium and will charge users $10 per month. This is a terrific fit for some of Dreamworks' content. YouTube's usual revenue split is 55/45. The content creator takes the larger cut. I think there is a possibility (TV) revenue will go up by quite a bit on the back of this partner model change. CEO Katzenberg stated on the latest earnings call:

As of Feb. 20, DreamWorksTV is now the number 1 family entertainment channel on YouTube with monthly viewerships and subscriber growth exceeding the Disney Channel, Nickelodeon ((and)) Cartoon Network,

DreamworksTV Asia

Q2 2015, Dreamworks launches a 24x7 DreamWorksTV channel in Southeast Asia. The channel will be broadcast in 17 countries. HBO Asia will manage the channel so Dreamworks is not risking a lot of time/effort/capital on this but it generates a revenue stream of a 3,000+ hours of its TV ready content library.

ODW Joint Venture

The Oriental Dreamworks JV (Joint Venture) is an effort to conquer the Chinese market, which will soon be the nr.1 entertainment market in the world. By partnering up with a local tycoon the company gets access to capital and Chinese know-how while giving up very little. Although the venture effectively means 55% of revenue is going to the Chinese partners, China’s attitude to foreign media companies is so hostile this is in practice a great trade-off. The JV is going to produce a feature film per year from 2016 and on. The JV is full capitalized. Co-producing with its Chinese partners means the distributor box office sales take goes up from 25% to 43%. The latter is in line with global International box office takes. This JV is currently producing nothing and actually only cost money. The market could be taken by surprise when this revenue stream suddenly comes online in 2016.

I started accumulating Dreamworks in the low 20s after disappointing releases but continue to like it even now it is trading in the mid-20s. Although I reserve the right to change my mind at any time, I now expect to ride the company to the mid-30s at least. That is where I will re-evaluate and base a decision on the progress that has been made by that time and the company’s updated prospects. I am not going to like selling before I am convinced the market has correctly priced in the Oriental Dreamworks cash flows coming online in 2016.