World Fuel Services is a $3.44 billion company. I first learned about this company by reading the research material put out by Horizon Kinetics, which is lead by Guru Murray Stahl (Trades, Portfolio). His writing is incredibly consice and his ideas powerful, which is why I try to read everything the firm releases. World Fuel Services supplies businesses with fuel. For example, if American Airlines needs its planes fueled and does not want to keep the activity in-house, it can become a client of World Fuel Services and the company will provide their planes with fuel on every airport their planes travel to. I do not know if American Airlines is an actual client, but you get the picture. The company does the same thing for fleets of cars and ships. With oil prices getting smashed, the company’s revenue is under pressure, although in my opinion, the market is overreacting to the decline in revenue this is causing.

Revenue for the first quarter came out at $7.3 billion, down 25% sequentially and 30% compared to the first quarter of 2014. The aviation segment generated revenues of $2.9 billion. That is a 26% sequential decline and a 32% year-over-year decline. The marine segment revenues came out to $2.3 billion, which is a 25% sequential decrease and a 33% year-over-year decrease. The land segment, which is the smallest segment, generated revenues equal to $2.1 billion. That is a 23% sequential decline and a 25% year-over-year decline. All of the YoY declines and sequential declines find their root cause in the oil price decline.

The key is the company is growing volume and will continue to do so. The aviation segment is the only segment where volume went down. Volume declined 3% sequentially to 1.45 billion gallons. This was caused by fewer selling days during the quarter, which is not a structural thing. The YoY number still looked good with the segment volume showing 10% growth of 125 million gallons. Volume in the marine segment increased to a record 7.7 million tons, up more than 500,000 tons, 7% as compared to the prior quarter and up 1.6 million tons, which translates to 27% YoY.The land segment booked revenue on 1.1 billion gallons in the first quarter, which is flat sequentially. Compared to the same quarter last year, that is still a 16% increase.

Given the hit the company took to its revenue, you would expect gross profit to fall dramatically for the first quarter. But it did not. Excluding a deferred revenue accounting adjustment, the gross profit came out at $217 million. The $217 million is only a decrease of $2 million or 1% sequentially, and still an increase of $29 million or 16% YoY.

The fact that the huge decrease in revenue was not accompanied by a huge decrease in profitability is a testament to the company’s strong business model. The company can deliver fuel very cost effectively because it only builds the infrastructure once in a location and can serve multiple clients. For example, it builds the infrastructure up to serve American Airlines, but it can at almost no additional cost serve Ryanair at that same location. With the company having so many hubs across the world, their solution is a very cost efficient option for customers. The company maintains this competitive advantage even when oil declines. There is even something to be said for the company’s competitive advantage becoming stronger when oil declines. As the infrastructure costs of fuel servicing increase in relation to the fuel cost, airlines or other operators become more sensitive to the cost of the infrastructure. When the infrastructure cost is merely a rounding error, they don't care to control it as much.

Financial strength

The company is financially sound. It could even benefit by getting rid of some of the cash on its balance sheet. I suspect management is on the lookout to make acquisitions and build its global network of fuel-nodes to strengthen its competitive advantage further and keeps some cash around to pay for these. The company has $700 million in debt and roughly $400 million in cash. With $330 million in EBITDA, the debt load is quite manageable and most of the cash is excess cash. Because the market is very fragmented with lots of small competitors, historically the company has employed a roll-up strategy. I expect that to continue although increasingly the targets will be bigger and deals probably less favorable.

The slide below is from a 2014 company presentation (the company does not give a lot of presentations, to its credit but to my chagrin as a writer for Gurufocus).

Source: company presentation

Management

Chairman and CEO Mr. Kasbar co-founded Trans-Tec Services, Inc in 1985, which is now the company’s World Fuel Services Americas. He served at various executive positions in the fuel business with an emphasis on marine fuel business, which may explain why that segment is currently doing so well. The management team owns a fair amount of shares, most likely representing a fair bit of their net worth.

The fact that insiders have been selling shares at the current level of the stock price makes me a little bit nervous, but not enough to deter me from buying into this long term growth story at a value price.

Risk

The company is exposed to various risks, including a slowdown in air traffic or naval movement. Although not exposed to an economic slowdown to the extent Airlines or shipping companies are themselves, it could nonetheless hurt World Fuel Services' growth rate. Examples of events that could really hurt the company are global warfare and volcanic eruptions that shut down air traffic in a major part of the globe. The U.S. military is a customer though, so warfare can sometimes mean additional business as the company is contracted to supply military vehicles.

Valuation

World Fuel Services trades at just 13x forward earnings and 11x EV/Ebitda. Meanwhile, the S&P 500 average P/E is 19. Just based on that comparison, given the fact the company has a strong competitive advantage because of the network effect its hubs produce, I will say it is cheap.

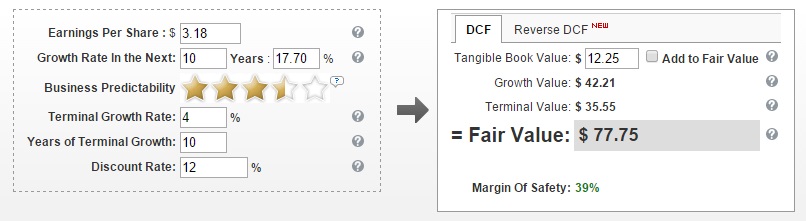

If you want to throw a DCF at it, the company will also come out looking fairly cheap. Below you can see the results when you put in various metrics in the DCF calculator provided here at GuruFocus. Ofcourse, you can disagree with any of the figures used and come up with your own model. The problem with DCF’s is that results can vary so much when you change a couple of % points or project a few additional years out. Nonetheless, it is instructive to put in the most accurate numbers you can come up with and evaluate the result:

Source: GuruFocus

The figures I put it lead me to believe the net present value of a share is worth something like $77 per share. A 39% premium over today’s price and that is why I own a few shares. It is not a major position for me, but at this price, I think it is worth owning.

Outlook

I expect the company will continue to execute on its roll-up strategy and build its competitive advantage by building out its global network of fuel nodes. Something that worried me before looking into it more is the potential impact of crude volatility. Obviously a hot topic after oil got hammered. As I have pointed out in the opening paragraph, it left World Fuel Services with nothing more than a scratch. Besides the company’s solid competitive advantage, the CEO adressed this issue and why crude volatility is advantageous to the company on a prior earnings call:

If everyone knows what something costs and where it is, well, okay, maybe you don't need a solutions provider as much as you do in more volatile environment. So we now have got a change in that dynamic. The shale oil is just extraordinary. You created some disruptions in terms of the flow of oil. West African product is now going to the Far East, and you've got a lot of very strange things in terms of dislocation of product. You've got coal that's going to Europe. Any number of different things. And certainly that change is what we thrive on.

When crude prices are volatile, having low turnover of inventory at locations hurts a business which is what happens to self-servicing providers. If Royal Dutch Airlines KLM takes care of its own fuel, it is just sitting there in a tank until one of its planes arrives while World Fuel Services has a higher turnover and less static exposure to price changes of its inventory. If you own a lot of inventory as a in-house fuel service company, you probably need to take more writedowns. Consequently, a volatile oil price environment is something where World Fuel Services can thrive. An environment with stable and elevated prices is an environment where it will struggle more.