Micron Technology Inc. (MU, Financial) provides semiconductor solutions worldwide in the form of Dynamic Random Access Memory (DRAM) and NAND flash memory products. Per GuruFocus, a number of notable investors own MU including David Einhorn, Seth Klarman, Joel Greenblatt, and more. David Einhorn (Trades, Portfolio) has a sizable position and recently made some interesting comments. Per the Wall Street Journal, Einhorn predicted that MU will be worth more than Netflix “sometime in the next few years” (Einhorn is bearish on Netflix). From what we can tell, Einhorn began purchasing MU in 2013 Q3 and his average price per share is $18.58/share. His latest batch of purchases was in 2015 Q2 is estimated to be at $26.66/share. Of course, we don’t know what hedges, if any, he used.

David Einhorn (Trades, Portfolio) MU holding trend:

Recent Events

- Weak Q3 ‘15 earnings call and poor guidance led to a sell off

- Stock rebounded back to $21/share after Chinese firm, Tsinghua, tendered an offer to take over the company

- MU announced a joint project with Intel (INTC) called 3D XPoint. See here.

- The company held an investor day for analysts on 8/14, and the stock fell another 4% to current price of $16.95/share

Company and Industry

- In Q3’15, Micron Revenue split was

- 61% DRAM

- PC’s made up low 30% of DRAM revenue

- High 20% for Mobile

- Low 20% for Servers

- 32% NAND

- 61% DRAM

- Gross Margin of 31% in Q3’15 vs 33% in FY’14

- Samsung is the largest player in the DRAM industry

- In FY 2014, DRAM made up 68% of MU’s revenue as Apple was a major customer. Earlier this year, it lost Apple’s business as Samsung supplied DRAM for the Iphone 6.

- In 2013, Micron purchased Elpida, a major competitor. The Elpida purchase put Micron behind on this generation of DRAM chips as management focused on closing the deal.

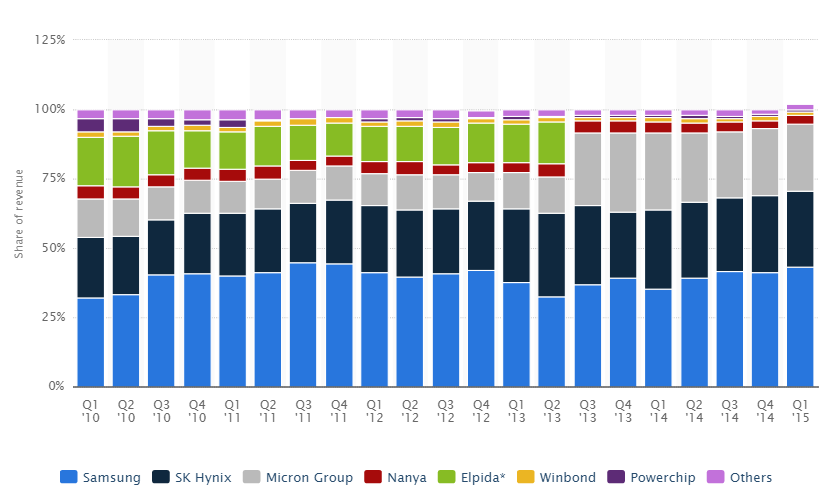

- DRAM Market Share Per Statista

| Supplier | Q1’15 |

| Samsung | 43.10% |

| SK Hynix | 27.70% |

| Micron | 24.00% |

| Other | 5.20% |

| Total | 100.00% |

- Market share trend going back to 2010.

- DRAM spot pricing trend from thememoryguy.com demonstrates price volatility

Bear Arguments

- ASP’s and shipments going down because of continued weakness in PC’s

- From the Q3’15 earnings call, “DRAM gross margins for the fourth quarter using quarter-to-date ASP and projected mix for the quarter should be down mid-single digits compared to the third quarter”

- ~40% of the company’s revenue comes from China and China bears expect weakening demand

- At some point, China may enter the DRAM market. Tsinghua's bid for Micron demonstrates China's interest.

- 3D XPoint will cannibalize existing DRAM chips. This point is difficult to handicap given that specifics like price have not been disclosed.

- Management is poor at communicating to the investment community

Bull Arguments

- Chinese firm’s takeover attempt establishes a valuation floor at $21/share

- The industry has consolidated, Samsung and other players will behave rationally, and ASP’s will stabilize

- Windows 8 was universally hated. There’s pent-up PC demand from consumers and corporations.

- Demand is diversifying with mobile and server revenue increasing

Current TTM Financial Ratios Per GuruFocus

On a backward looking basis, MU looks cheap.

- PE Ratio of 5.68

- Price to Book of 1.46

- EV / EBIT of 6.09

- Current Ratio of 2.19

- Debt to Equity of 0.61

Final Thoughts

- Net income through the first 3 quarters of FY’15 comes out to $2.04/share. Based on management’s feedback, I estimate $0.10/share for Q4’15. That would give Micron a PE of ~8 for FY’15.

- If I model FY’16 by keeping revenue flat and lowering DRAM gross margin percent in mid single digits (in line with management’s guidance for Q4’15), I can easily get to $1/share which would explain the pessimism of short term oriented market participants. That would be quite a drop compared with FY’14 EPS of $2.54.

- Micron is an unpredictable situation. The unpredictable elements include customers, suppliers, competitors, price, quantity, cost, etc. For example, there was a fire at Hynix’s fabs a couple years ago which affected DRAM prices.

- With that said, the need for memory going forward is predictable. Data is being generated at an unprecedented rate.

- My belief is that DRAM prices will revert to the mean eventually.

- Tsinghua’s bid on MU at $21/share also provides rationalization to MU’s value.

- I don’t agree with the bear argument that PC demand will continue to tank and MU should be $10/share. I also don’t think this is a no-brainer situation like the bulls say. There’s too much uncertainty.

- Instead, I consider this to be a medium risk, high reward opportunity.

Disclosure: I’m long MU and short puts.