American Express (AXP, Financial) was originally an express mail service started back in 1850. In the 1900s the company started a financial services branch. First the famous Travelers Cheques were a big hit and later the American Express card in 1958. Today the company is providing charge and credit card products, travel services, network services, loans and other services both in the BTC and BTB markets on a global scale.

The firm benefits from a tremendous network effect created by a large constituency of cardholders and merchants where the cards can be used. It is worth noting that American Express is focused on the high average annual spending side of the market. American Express is the iPhone of credit cards so to speak. The average amount charged to its cards is significantly higher than the amount charged to major competitors' cards. This helps to make the company an attractive partner to sellers who like to serve this demographic. This in turn enables American Express to leverage its position to charge sellers a sweet fee and also powers higher rewards to the holders of its cards which in turn reinforces the ties between the card users and the company.

There are two major paradigm shifts going on that affect American Express. 1) The progress that is made in the processing and utilization of big data, and 2) a possible revolution in how payments are being made.

The company may very well be in a terrific position to profit from the increased utilization of big data. This may add another source of revenue to the existing ones while adding comparatively little in additional operating expenses. The capabilities to collect vast amounts of highly valuable data on spending are already in place. The infrastructure to utilize this most effectively by others in the value chain is only starting to materialize.

A revolution in the way payments are made can threaten American Express’ competitive advantage. Brands like Google (GOOG, Financial)(GOOGL, Financial) and Apple (AAPL, Financial) are trusted by consumers. They occupy slots on people’s bodies through watches and smartphones. If they are able to build payment solutions that are attractive to consumers and are widely accepted, American Express may have a gigantic problem. Creative solutions are being developed by lots of different companies like PayPal (PYPL, Financial), Venmo etc. It is important to keep track of how these threats develop. It will not be impossible for American Express to navigate the environment successfully, but it may require defensive buyouts and adaptation.

The firm has both a fair amount of net debt equal to $37 billion. The gross amount is a fair bit higher, but the company also holds many billions of cash. Its market cap is about $77 billion and gross operating profits are close to $6 billion. The weak point in its financial affair lies most likely with the credit it extends to consumers.

Management

American Express is headed by CEO Kenneth Chenault who worked at the company for more than 30 years in various roles. He first started back in 1981 and worked his way up to president of the U.S. division of American Express Travel Related Services in 1993. Then vice chair of American Express in 1995, president and COO in 1997 and finally CEO in January 2001. He is also a director with IBM (IBM, Financial) and Procter & Gamble (PG, Financial) and holds various other board memberships.

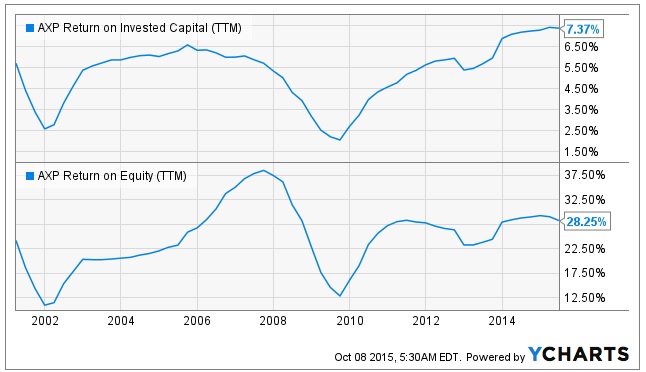

Returns have been rather spectacular. It is hard to ask for better RoE compared to what American Express achieved over Chenault’s tenure. How much can be chalked up to him and his team and how much to American Express’ incredible competitive advantage is a question that is hard to answer. It is hard to argue Chenault is not a good caretaker of the franchise. I am confident he is not going to do something really stupid, and he could very well be an excellent CEO.

Risk

The biggest risk to the American Express model is being out-innovated by tech startups. Digital wallets or other payments solutions could start taking away market value and also make it more difficult for the firm to leverage its power over sellers and merchants, resulting in deteriorating margins. American Express still has a multitude of defensive options at its disposal, but the threat should not be downplayed.

Valuation

Because American Express is a company with a fairly stable revenue stream and a relatively stable cost structure, a DCF calculation works reasonably well to value the company. DCF models can produce enormous differences in results if you use other inputs. To get to a realistic net present value I used TTM earnings as a base value and assume 10 years of growth at the company’s historical EPS rate*, use a terminal value of 0% and discount against the Standard & Poor’s 500 historical return of 11%. The net present value I arrive at is $83.32.

GuruFocus allows you to run a DCF calculation very easily by using its built-in calculator. The advantage of playing around with the model is that you can arrive at a net present value that you think is realistic by changing the parameters.

The caveat I have with the DCF I put together is that it does not really account for the somewhat unusual capital structure of the company. There is quite a bit of debt and a large cash hoard. You could argue some of that cash justifies a premium on top of the net present value but how much is debatable given the debt level. Some of the cash is most likely also required to maintain historical EPS growth rates. The cash is most likely not entirely redundant. Overall, I think the result of my net present value calculator is rather conservative.

A second way to look at the company is by comparing it to its peers or the overall market in terms of valuation and the expectations that are implied by it. I don’t like to compare American Express to its peers (see image below) –Â Visa (V, Financial), Discover (DFS, Financial) and others –Â because the entire industry is being cast as under siege as tech upstarts try to revolutionize the payment industry. Much more interesting is how does American Express compare to the market and is the threat it faces really that much bigger than those faced by other industries?

| Ticker | Company Name | Financial Strength | Profitability Rank | Market Cap (Mil) | P/E (NRI) | P/S Ratio | Oper. Margin (%) | ROA (%) | ROE (%) | Debt-to-Rev. | Current Ratio |

| American Express | American Express Co. | 4/10/2015 | 7/10/2015 | 77,279 | 13 | 2.36 | 26.78 | 3.81 | 28.1 | 1.73 | 0 |

| CIT | CIT Group Inc. | 7/10/2015 | 8/10/2015 | 7,235 | 7.5 | 3.02 | 25.34 | 2.13 | 11.13 | 6.7 | 0 |

| COF | Capital One Financial Corp | 6/10/2015 | 7/10/2015 | 40,660 | 10.3 | 1.84 | 26.26 | 1.34 | 8.82 | 1.93 | 0 |

| DFS | Discover Financial Services | 7/10/2015 | 7/10/2015 | 24,051 | 10.8 | 2.91 | 40.91 | 2.71 | 19.37 | 2.79 | 0 |

| LC | LendingClub Corp. | 4/10/2015 | 2/10/2015 | 5,395 | 0 | 3.59 | -8.32 | -0.73 | -4.17 | 9.44 | 0 |

| LEAF | Springleaf Holdings Inc. | 4/10/2015 | 3/10/2015 | 6,284 | 13.8 | 3.04 | 38.93 | 2.96 | 16.99 | 8.12 | 0 |

| MA | MasterCard Inc. | 7/10/2015 | 7/10/2015 | 107,753 | 28.2 | 11.48 | 52.84 | 25.29 | 58.23 | 0.16 | 1.58 |

| PYPL | PayPal Holdings Inc. | 4/10/2015 | 3/10/2015 | 39,463 | 99.5 | 4.75 | 15.8 | 2.04 | 5.36 | 0.14 | 1.32 |

| SYF | Synchrony Financial | 5/10/2015 | 5/10/2015 | 26,789 | 12.1 | 2.02 | 30.23 | 3.01 | 21.97 | 2.46 | 0 |

| TSS | Total System Services Inc. | 5/10/2015 | 7/10/2015 | 8,659 | 26.4 | 3.32 | 19.38 | 8.66 | 18.85 | 0.52 | 2.38 |

| WU | Western Union Co. | 6/10/2015 | 8/10/2015 | 9,615 | 11.5 | 1.78 | 20.04 | 8.48 | 68.37 | 0.67 | 1.12 |

| Data: | GuruFocus | Â | Â | Â | Â | Â | Â | Â | Â | Â | Â |

American Express is trading at a P/E of 13, P/S of 2.36 and 7.6x FCF. Compare that to the S&P 500 which is trading at an average P/E of 18, 1.7x sales and 10.8x FCF. American Express is looking quite cheap compared to the average constituent of the index, and don’t think for a second the average company in there is consistently providing you with RoE in the low 20s. Not even close.

Outlook

The threat from mobile technology payment solutions is not going to go away overnight. I don’t expect a few good quarters of earnings are going to dissuade the market. An investment in American Express is one of slowly grinding out much more value than the market is accounting for. It is going to take years, but it may well be quite a few percentage points above market return. This will happen because of earnings just not falling as expected, the company defending itself from some threats by integrating them in its own network, coöperating with others all the while its traditional business model is degrading slower than expected. Although the growth rate of the business is not going to be superb, lots of value can be created for shareholders through dividends and buybacks. It is going to be a slow grind but it may very well be a profitable one.

*over the past 10 years