So, on Monday I wondered why Citi (C) has so little interest in a Goldman Sachs (GS) deal. Hint: It starts with a "D" and Goldman does not have them.

On the last earnings call CFO Gary Crittendon said regarding potential uses for the TARP funds, "And it does present, then, the possibility of our taking advantages of opportunities that otherwise might have [inaudible] to us. Now, as we think about that, the way we approach it is in the same disciplined manner that we’ve approached these other opportunities over the last few weeks. So I think in total now we have looked in detail at the possibility of acquiring three institutions, two of which you’re aware (Wachovia (WB) and Washington Mutual (WM)) of and one that we haven’t talked about publicly in any way.

And as we approached that, we did it with a very well-defined set of parameters. There is only a certain set of circumstances which made sense for us to do that. We will think about the use of this capital in the same way. It is an attractively priced amount of equity capital, and as you correctly said, an attractively priced amount of fixed income, that can match with that."

In response to another question about the "next opportunity" he replied:

"Here is what I think we would say internally, what we are saying to ourselves. Basically we had a strategy that we outlined at Citi Day that had us focused on growing five businesses. Two of those are asset businesses, our Card business and our markets and banking business; and three of those are liability gathering businesses, deposit gathering businesses. That is our Wealth Management business, our Consumer retail business, and our GTS business.

Our focus is behind those businesses; and that remains exactly as it was before. In order to fund those businesses, we have the program underway that you just talked about. We are cutting our expenses; we are showing good traction on that. We are moving assets out of categories that don't fit with that profile. We have been selling businesses that didn't match there. We have carefully managed down our headcount.

So we have worked very hard to execute against that strategy -- and that is our strategy. Now opportunistically, we had the chance, obviously, to acquire Wachovia. For all of the reasons you are aware of, that is not going to happen.

But the net result of that is not a change in our strategy."

So, the question then becomes. Where does Goldman fit? Answer? It doesn't. Citi wants deposits and neither Goldman nor Merrill (MER) have any. Sources at Citi indicated to me if it does a deal it will be with a depository institution that has minimal branch over lap with current operations, not a broker.

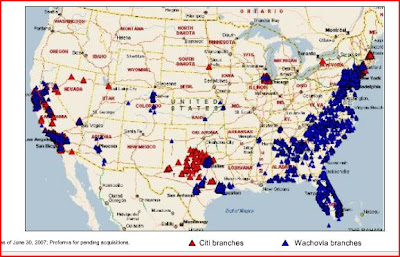

So, then the next, obvious question is "who fits the bill"? In order to figure that out, let's look at what Citi was trying to accomplish with the Wachovia deal. The following image has the Red (Citi) and Blue (Wachovia) branch coverage post then proposed merger.

Who then, could give Citi this type of coverage?

With 1600 branches throughout DC, Alabama, Tennessee, Virginia, Florida, Georgia, Maryland, Arkansas, Mississippi, N. & S. Carolina, Ohio and West Virginia SunTrust Banks (STI) looks to fit the bill.

SunTrust is fresh off a $3.5B Treasury infusion. Last Thursday it reported that Q3 profit fell 25 percent, hurt by the effects of the credit environment. Net income fell to $307.3 million, or 88 cents per share, from $412.6 million, or $1.18 a share, a year earlier. Revenue rose 20.7 percent to $2.46 billion. SunTrust set aside $503.7 million for loan losses, up from $147 million a year earlier.

Earlier this year, SunTrust announced plans to dispose of its 43.6-million-share stake in Coca-Cola (KO), worth roughly $2 billion to bolster capital. It has held the soft drink maker's shares since 1919. That move would make it more appealing to a potential suitor.

Citi seems intent on doing something, Suntrust may just be the best of what is still out there...

On the last earnings call CFO Gary Crittendon said regarding potential uses for the TARP funds, "And it does present, then, the possibility of our taking advantages of opportunities that otherwise might have [inaudible] to us. Now, as we think about that, the way we approach it is in the same disciplined manner that we’ve approached these other opportunities over the last few weeks. So I think in total now we have looked in detail at the possibility of acquiring three institutions, two of which you’re aware (Wachovia (WB) and Washington Mutual (WM)) of and one that we haven’t talked about publicly in any way.

And as we approached that, we did it with a very well-defined set of parameters. There is only a certain set of circumstances which made sense for us to do that. We will think about the use of this capital in the same way. It is an attractively priced amount of equity capital, and as you correctly said, an attractively priced amount of fixed income, that can match with that."

In response to another question about the "next opportunity" he replied:

"Here is what I think we would say internally, what we are saying to ourselves. Basically we had a strategy that we outlined at Citi Day that had us focused on growing five businesses. Two of those are asset businesses, our Card business and our markets and banking business; and three of those are liability gathering businesses, deposit gathering businesses. That is our Wealth Management business, our Consumer retail business, and our GTS business.

Our focus is behind those businesses; and that remains exactly as it was before. In order to fund those businesses, we have the program underway that you just talked about. We are cutting our expenses; we are showing good traction on that. We are moving assets out of categories that don't fit with that profile. We have been selling businesses that didn't match there. We have carefully managed down our headcount.

So we have worked very hard to execute against that strategy -- and that is our strategy. Now opportunistically, we had the chance, obviously, to acquire Wachovia. For all of the reasons you are aware of, that is not going to happen.

But the net result of that is not a change in our strategy."

So, the question then becomes. Where does Goldman fit? Answer? It doesn't. Citi wants deposits and neither Goldman nor Merrill (MER) have any. Sources at Citi indicated to me if it does a deal it will be with a depository institution that has minimal branch over lap with current operations, not a broker.

So, then the next, obvious question is "who fits the bill"? In order to figure that out, let's look at what Citi was trying to accomplish with the Wachovia deal. The following image has the Red (Citi) and Blue (Wachovia) branch coverage post then proposed merger.

Who then, could give Citi this type of coverage?

With 1600 branches throughout DC, Alabama, Tennessee, Virginia, Florida, Georgia, Maryland, Arkansas, Mississippi, N. & S. Carolina, Ohio and West Virginia SunTrust Banks (STI) looks to fit the bill.

SunTrust is fresh off a $3.5B Treasury infusion. Last Thursday it reported that Q3 profit fell 25 percent, hurt by the effects of the credit environment. Net income fell to $307.3 million, or 88 cents per share, from $412.6 million, or $1.18 a share, a year earlier. Revenue rose 20.7 percent to $2.46 billion. SunTrust set aside $503.7 million for loan losses, up from $147 million a year earlier.

Earlier this year, SunTrust announced plans to dispose of its 43.6-million-share stake in Coca-Cola (KO), worth roughly $2 billion to bolster capital. It has held the soft drink maker's shares since 1919. That move would make it more appealing to a potential suitor.

Citi seems intent on doing something, Suntrust may just be the best of what is still out there...