It is January and activist fund Starboard Value decided to get busy. Just last week the board of Yahoo (YHOO) received a harshly worded letter, and today the board of Macy’s (M, Financial) received one. The latter, however, received a letter that is much more mild in tone and more typical for the coöperative engagement style of Starboard Value. It is accompanied by a presentation on the real estate value within Macy’s, which is the focus of the fund. I’ll highlight several interesting points made by the fund (emphasis is mine):

We were pleased to see the Company announce an immediate reduction in operating expenses of $400 million, with a target of $500 million in expense reductions by 2018. As we have shared with you in other presentations, we, along with our retail- and operations-focused consultants, have identified more than $500 million in cost reductions through a combination of improved labor productivity and SG&A reductions, as well as other EBITDA improvement opportunities

These cost cuttings are most likely realistic in which scenario the company can take its EBITDA from $3.67 to approximately $4 billion. With an enterprise value of just $18 billion, that’s already quite interesting. But there is more:

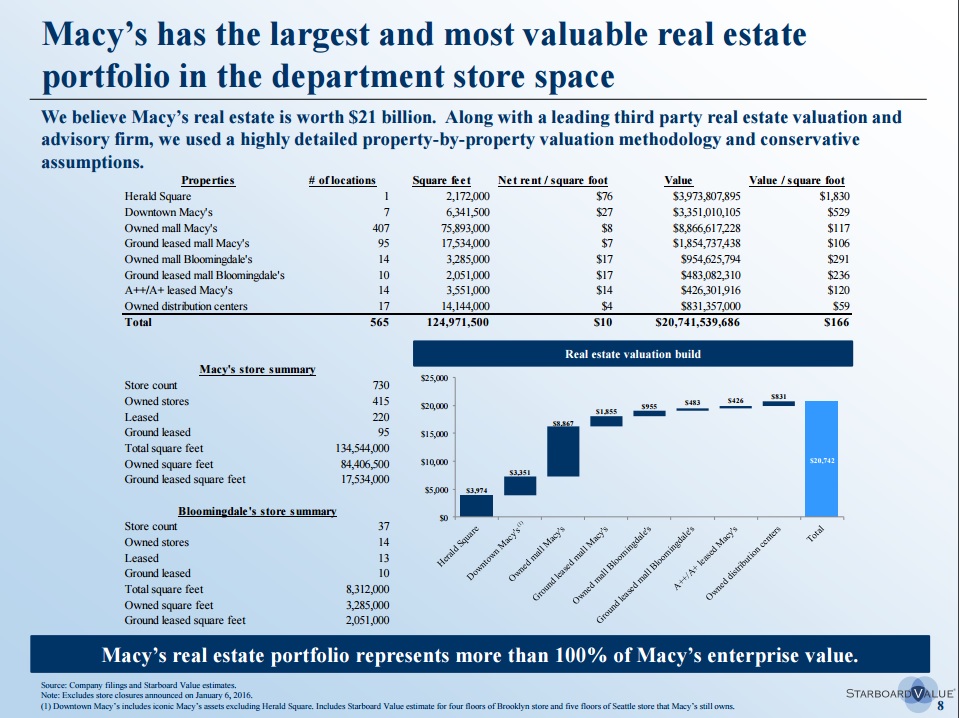

The firm has a sizeable and high quality real estate portfolio. So much so that Starboard Value believes it to be worth more than the entire enterprise value (~$21 billion versus ~$18 billion) of the company. That means the operating company is currently valued at zero or even negative. The company's plan involves the creation of two joint ventures:

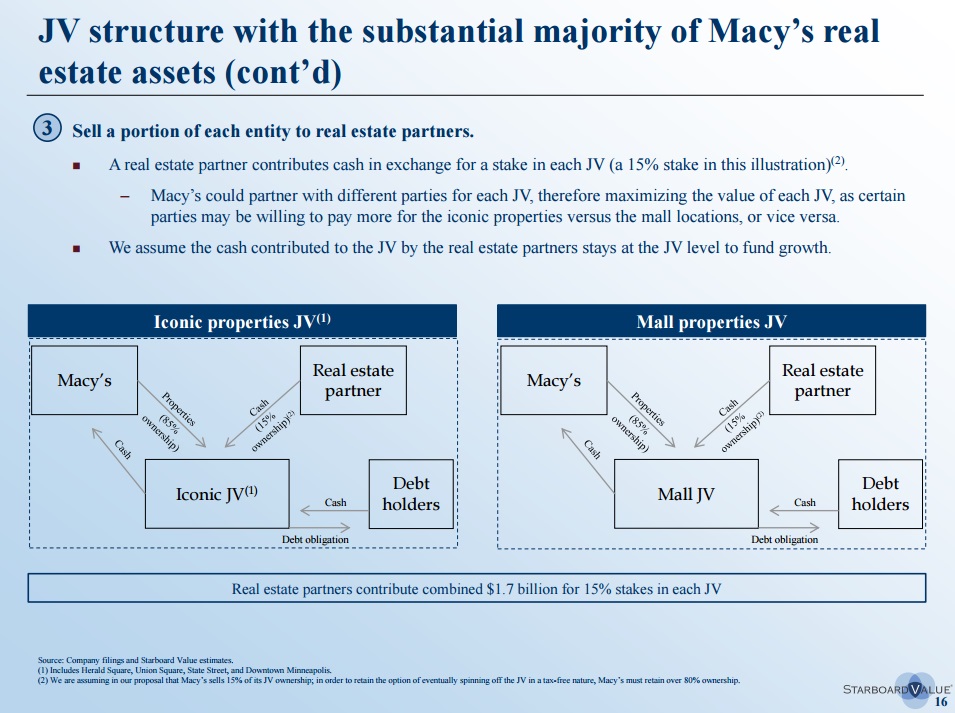

We believe that a JV, or series of JVs, can crystallize the value of Macy's real estate while bringing in a partner with substantial capital and real estate expertise that will enable the JVs to grow and diversify their real estate holdings. The structures that we have proposed, which appear to be in-line with what you are actively exploring, would enable Macy's to:

Highlight the value of Macy's underlying real estate, via the price paid by a well-respected real estate investor for a substantial minority interest;

Immediately take in cash to pay down debt such that Macy's OpCo could achieve a net cash balance, if desired, or more likely, substantially less funded debt;

Retain almost all of its cash flow availability at the parent company level, through distributions from the JV(s) (if desired at the time), resulting in the Company continuing to generate over $1 billion in free cash flow per year;

Maintain the current investment grade rating and the current (or higher) dividend;

Further monetize minority interests in the JV(s), if more cash is needed to fund a major operating project or other investment; and

Maintain flexibility to further separate or monetize its real estate JV(s) via a future IPO after more seasoning of the JV strategy, more comfort with the financial position of Macy's and the JV(s), and increased clarity on the retail outlook.

The key to the value creation Starboard Value is after is the company putting its real estate in JV with high profile and capable real estate operators. This is something of a first step towards a real estate spin-off into a REIT, a transaction that is now commonly done. In order to be able to execute such a move later on, the company has to be careful not to decrease its stake in the JV below 20%. In Starboard’s presentation it looks like this:

Ultimately, the Starboard proposed transaction and cost cutting would allow Macy’s to maintain control of its properties. It will allow it to maintain all of its cash flow at the Macy’s operating company level, and maintain its investment grade rating and even leave the operating company debt-free or with much less funded debt. Macy’s appears to be engaged and cooperative, and the company even asked for the presentation materials, implying they want to go over them again or study them in more detail.

In the aggregate I view this as a huge positive for Macy’s shareholders. If this can ultimately result in a Macy’s with little or no debt and EBITDA of $4 billion, it is a steal at the current level $37 per share level with a market cap of just $12 billion. In Starboard's view the company can go to $70 per share after the transaction.