I predict that "Game of Thrones," adapted from the books in the series "A Song of Ice and Fire" by George R.R. Martin, will most certainly outlive the current bull.

Having been told repeatedly by scores of analysts that “winter is coming” to this particular market and that the White Walkers will surely destroy the market, we can be forgiven if we have tired of their bearish chatter. So like most residents of the lands south of The Wall, many investors have decided White Walkers (and bear markets) are only myths, and we should go on about our business of seeking wealth and the power wealth brings. ("Game of Thrones" haters, you may read on; I promise to stop making references to the TV serialization or the books.)

The point is that bear markets may still occur in our lifetime. At some point it behooves us to perhaps take some profits off the table, accepting the “possibility” that as much money might be made, going forward, in solid income-producing securities, as might be gained by buying index funds and such.

Indeed, if the bear is more than a correction and truly awakens from hibernation, such an approach might not only provide reasonable returns in times of turmoil but may actually protect capital so as to provide truly exceptional entry prices at some point a bit down the road. I place myself squarely in this camp.

Regular readers have seen a trend since we began to see our trailing stops execute at an accelerating rate in January and February. It seems ever clearer to me that mid-2016 is not likely to be a good time for “risk-on” investing. Why not? There are many reasons, but for this issue let me elaborate on two I have not discussed in as much depth in my previous articles on this subject. Both are strategic issues that must be addressed if the markets are to be trusted and the economy is ever to get out of the current government-induced doldrums. I’ll then provide some ideas for how to protect your capital in this environment.

Reason #1: Companies have for years been able to use pro forma rather than GAAP accounting, merrily buying their own shares back to goose the earnings “per share” figures and therefore give their managers massive bonuses. Some analysts think this is a good idea — after all, it’s only stock, not dollars, and the number of shares is diluted over so many shareholders that the dilution isn’t as evident. But just as water flowing over a rock will not visibly alter it, over many years that rock will become “river rock,” not only rounded but smaller.

It is the same with individual shareholders’ holdings. Drip by drip, hired administrators and their favored cronies are making as much or more than those few with real talent. The dizzying escalation in executive pay, and worse, stock options, has made a mockery of corporate “governance,” with a few at the top of public companies making hundreds or thousands of times as much as the workers in those companies.

This practice is beginning to catch up to these firms as their boards of directors begin to realize their erstwhile golden boys, now retired with a similar-colored parachute, have left the companies far behind in research and development and far behind in capital expenditures. They have paid massive capital-draining salaries and bonuses and are now left behind the curve.

Now the current crop of administrators must make hard decisions. Having paid up to and including top dollar for shares selling at new highs, they need to conserve funds for R&D and CapEx or they will lose market share to those who spent their money more wisely. As this quarter’s results so painfully show, for many large and once-successful companies, their top-line revenues are down, their earnings are down; for those realizing they can’t keep playing funny-money games, even their earnings per share are down.

This leaves just one final illusion to perform. As quarter end approaches, they flurry to the Wall Street analysts who tout their shares and suggest the analysts (who want to look good to get their own bonuses) lower their quarterly earnings “estimates.” This incestuous relationship ensures that the analyst looks good and both Wall Street and the reporting company can trumpet that while revenues may have been down they once again beat the earnings estimates.

You ask, they can’t really believe we’re so stupid we don’t notice the sleight of hand, can they? I respond: I assume your question is rhetorical. Not only do they believe it, but enough market players (I can’t bring myself to call them “investors”) swallow it hook, line and sinker that the game can go on. But by now, it is going on with decreasing volume. As more catch on, I fear for the aging bull.

Reason #2: Regulations and red tape are strangling American entrepreneurs. Are we becoming just another tired and bloated European-style social welfare republic? The facts would support this argument. The American Dream of prior years is further and further out of reach of the average American. Red tape is now strangling the entire nation.

Do you wonder why the elites in the boardrooms and corporate corner offices, the White House, Congress, the Fed, the SES’s (“Senior Executive Service”) administrators, etc., all tout how wonderfully the economy is doing while any cross-country road or rail trip will show just how poorly “the rest of us” beyond the Beltway are doing? It’s because “their” economy is doing fine. With what they make and with whom they associate all doing exceedingly well, they just don’t understand why the rest of the nation doesn’t get it.

We do. They don’t.

They aren’t trying to start or run private or growing businesses, or earn an honest day’s wage for an honest day’s work at such a company. In many cases, they aren’t even subject to the onerous regulations they have imposed. They have their own “special” plans for special people.

I am indebted to a new study by the Mercatus Center at George Mason University, whose authors (Patrick McLaughlin, Bentley Coffey and Pietro Peretto) have put in dollar terms what those of us running a business or working for a living know: even Nazi Germany or Communist Russia never had this many regulations to run afoul of and, consequently, keep voracious government gorging itself on new fees, fines, licenses, lawsuits and taxes.

The Mercatus Center paper looked at regulations imposed since 1977 on 22 different industries, those industries’ real growth rates and what might have happened if all those regulations had not been imposed. Of course there have been benefits to some of these regulations, fines, fees and so on. We have cleaner air, safer workplaces, more (though perhaps increasingly difficult to obtain) health care, etc. And I’m sure we’d all be happy to pay an extra, oh, call it a trillion dollars, for those benefits.

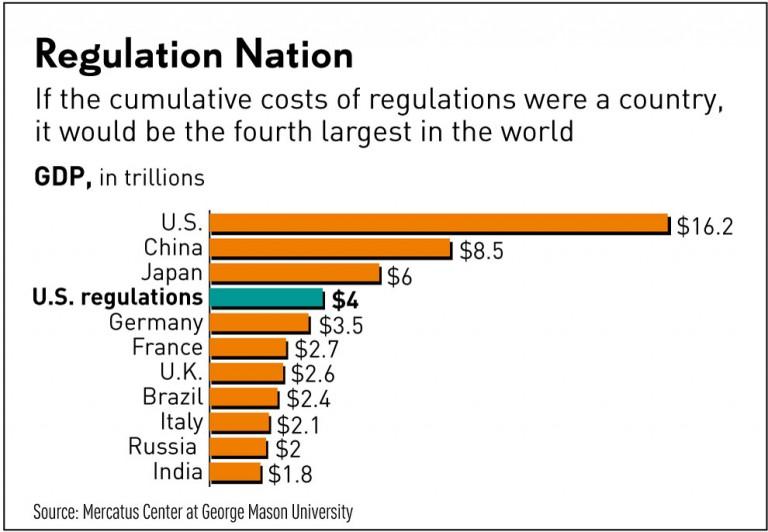

But $4 trillion, including only federal regulations, not even counting the additional burdens imposed by states, counties and cities? Four trillion dollars. That’s how much we taxpayers have given up since 1977 to support the imperious and bloated federal bureaucracy.

(click to enlarge)

The chart above shows that, if the economic growth lost to regulation in the U.S. were its own economy, it would be the fourth largest in the world! That’s not our GDP, it’s not our debt, it’s just our regulatory burden. Are we descending to the Third World model of central planning and economic misery? If ever there was a self-inflicted wound, this is it! Our Code of Federal Regulations is now more than 81,000 pages long!

It wasn’t always this way. To cite just one example, in 1939, even after six years of the New Deal, our tax code consumed just 504 pages. Today that has mushroomed to 74,608 pages! Who can understand all of this? No one. Who gets to interpret little bits and pieces of it? Clerks within the bureaucracy and lawyers within and outside.

The problem has hugely accelerated since 2008. The George Mason study notes that President Barack Obama has imposed 85 more “economically significant” regulations than did President Bill Clinton and 100 more than President George W. Bush. (A total of 372 new pieces of suffocating red tape, 172 during his first term and now, with the finish line of his vision in sight and an acquiescent Congress, 200 more since then.)

The cumulative effect of all these diktats are appalling. Not only have they hemmed in our freedom to move, to act and to live, they have cost each of us financially. The Center’s findings include that if the regulatory regime in place in 1980 was still in evidence today, the U.S. economy in study year 2012 would have been $4 trillion bigger. That would be equal to almost $13,000 per person in that one year alone. Lop off a trillion for the truly worthwhile regulations, and it still comes to nearly $10,000 per person.

Could you have used an extra $10,000 a year for the past four years? Would the country be growing jobs and wages better with an extra $3 trillion in the real world of workers, innovators and businesses than in salaries for lawyers and administrators in federal agencies where more regulations mean more power and money for them?

The Tax Code alone directs pork subsidies to allow the already-rich to buy Tesla (TSLA, Financial) “Electric Vehicles” (which, by the way, run on electricity produced by – coal, gas, oil, etc.) and to buy insurance from a select list, to turn good food corn into more expensive gasoline, to replace our windows, adopt kids, pay for day care, go to college, and the beat goes on.

The latest stifling new batch of regulations includes picking favorites from the health care industry, ensuring the survival of the banking and financial services industry and making sure utilities (read: consumers) pay through the nose for natural gas if they don’t immediately switch to far less efficient wind or solar.

We need a complete zero-based review of the cost and benefit of these mandates and dictates.

It could happen with the sweep of a new broom in November. Until there is greater clarity there, however, I’ll take the “risk-off” approach that allows our clients to sleep well with fine income holdings. Here are a couple we are currently buying.

A fine income holding

Starwood Property Trust (STWD, Financial) is a commercial real estate lending, servicing and investing company. It is the largest commercial mortgage REIT in the U.S. and one of the biggest and most successful in the world, yet its price has been under pressure lately. This may be because most people don’t believe rates will rise again (ever???). For whatever reason, I believe the current price of Starwood offers us a unique opportunity to own a great company at a great price.

Formed as the 2007-2009 recession ended and taking full advantage of the decimated commercial lending landscape, the company has yet to lose a dollar, yen or pound in commercial lending, which comprises 61.3% of its total assets. Being formed when it was, the assumption must always be that rates will (someday) rise. That’s why 82% of its loans are indexed to LIBOR; the interest charged will rise as LIBOR rises.

Because of its current low valuation (the share price has fluctuated between about 16½ and 24½ the past 52 weeks), Starwood currently yields an excellent 9.9% yield. That’s not unusual for mortgage REITs, but it is unusual for one of this heritage and quality. Despite the rebound as a result of somewhat improved investor sentiment toward high-yield stocks, Starwood Property is still down so far this year. It sells for just above 10x earnings, a hair above book value, enjoyed a return on equity (ROE) of just under 13% in the last reported quarter –Â and sells at a stellar 7.4x operating cash flow.

I need to remind readers that what you are buying with a mortgage REIT is cash flow. Unlike equity REITs, 100% mortgage REITs have no opportunity for capital appreciation. Their stock may appreciate based on undervaluation, increased cash flow or a favorable change in investor sentiment, but the company basically makes lending decisions and collects payments on the money it has lent out. Of course, how smart a company is in assessing and assigning risk is key. In Starwood’s case, its “loan to value” hovers right around 63% and consists primarily of first mortgages. In other words, if it believes a purchase, renovation or other activity will create an asset value of $1 billion, it might loan $630 million. Here is one example of the kind of upscale property it has financed:

Starwood may benefit from all three possibilities cited above for its stock to appreciate. Now the kicker: while Starwood has 61% of its assets in commercial mortgage lending, the other 39% is in small equity positions and servicing fees for other lenders. It has the scale to service loans cheaper than many originators do.

All this leads me to believe there is an additional possible wind at Starwood Property’s back, and that is a dividend increase. With cash flow numbers like these and the likelihood that, in Europe, rates will not go further negative but begin to come back above zero, I think increased cash flow from all segments will mean an increase in the dividend. The company can afford it now and, as a REIT, it must pay at least 90% of its earnings as dividends.

Finally, because of Dodd-Frank induced “risk-retention” rules, which force more firms to keep a portion of whatever they package as mortgage-backed securities, I see the number of competitors falling off over the next year or so. This places Starwood Property Trust in a great position. It has the experience, the head start and the right management team to be able to capitalize on the shrinking number of packaging sponsors.

A fine income holding, part II

Preferred shares might well lose value in a protracted bear market. In which case, we would simply add more. As long as they are bought at or below par and they are issued by companies with a future we believe to be secure, we’ll always get that nice, steady return. Bought below par, the return is better, of course.

Every now and again the market will seriously overreact, as it did in late 2008 and early 2009, and provide us with a cornucopia of delightful offerings. I purchased one such one-time good deal on March 6, 2009 (by chance, not prescience, the absolute lowest day of the entire decline). I purchased to provide some ballast for the Aggressive Portfolio, 500 shares of Silicon Valley Bancshares 7% preferred, $25 par value (SIVBO) for $10 a share. At the time, the prevailing panic was that all banks would go belly up. I figured if any survived it would be a bank that catered to the best innovators.

It worked out. I list SIVBO’s current yield as 6.9% since it sells for a little above par now. But on a “yield-to-cost” basis, we are getting 20% a year in interest on this preferred. If it never moves a penny in capital appreciation, and there is little reason it should, over the past seven years we have received $4,900 in interest on our $5,000 investment and now own something worth an additional $12,850. These opportunities don’t come along often but when they do, when the markets look bleak, hearken back to this article and take the plunge.

Regrettably, I find no such bargains in preferreds today. It seems everyone has caught on to their benefits. But I have been buying a speculative preferred that is, at least, slightly below par. It is the Qwest Corp 6.125% Notes due 2053 (CTU) a synthetic preferred in that it is really a piece of a bond. It is callable at par (in this case, $25) any time after June 1, 2018 by the parent company. Because it is part of a bond offering, the income is classified as “interest” and not as a “dividend.” These notes are unsecured and unsubordinated obligations of the company and will rank equally with all existing and future unsecured and unsubordinated indebtedness of the company.

Qwest doesn’t exist as an independent company any more. It was purchased 100% by CenturyLink (CTL, Financial). The CenturyLink website refers to itself as “a global communications, hosting, cloud and IT services company enabling millions of customers to transform their businesses and their lives through innovative technology solutions. CenturyLink offers network and data systems management, Big Data analytics and IT consulting and operates more than 55 data centers in North America, Europe and Asia. The company provides broadband, voice, video, data and managed services over a robust 250,000-route-mile U.S. fiber network and a 300,000-route-mile international transport network.” So it isn’t AT&T (T, Financial) or Verizon (VZ, Financial), but neither is it a small fry.

It operates in a tough neighborhood but, so far, seems to be holding its own. The company is a fair bet to last in its various niches. It has assumed the responsibility to repay the “preferred” shareholders of CTU at maturity. Currently selling for $24.70, we buy when we can. Of course, that goes for all preferreds we favor – below par, we’ll nibble, well below par we’ll back the truck up!

Basic, boring, dull and profitable

Owning a merger and arbitrage mutual fund or ETF is every bit as exciting as watching paint dry on a too-cool day. But they do reward us with small but steady profits in most market environments. And they tend to be almost completely uncorrelated to what happens in the general markets while still allowing us to benefit from extraordinary events in the markets.

Among the funds I have researched, Vivaldi Merger Arbitrage has been rising to the top. My first caveat is that this is a load fund. It is waived for those broker-dealers and others who have an agreement with Vivaldi to waive the load for (among others?) registered investment advisers, the theory being that we will, for our clients, quickly reach the zero-fee breakpoint anyway. So for our clients, and maybe your adviser, there is no fee.

Vivaldi provides a dose of what we want for the immediate future: low to no correlation with the market and low volatility during what probably will be volatile times. Merger and arbitrage (M&A) funds don’t buy companies they think “might” be taken over or “hope” will be acquired. Instead, they purchase the stock of a company which has already announced it is being acquired (the “target” company) while at the same time shorting the stock of the company acquiring the target’s stock. The fund profits from the difference in price between the current trading price of the target company following the announcement of the merger (which is usually “close” to the acquisition price), and the acquisition price to be paid for the target company at that future point when the acquisition is consummated.

In other words, Vivaldi is betting that the spread between the price the target jumps to on the news and the price ultimately paid for it justifies the time and attention. Often, of course, even if the deal falls through, there is a contractual fee paid to the target if the acquiring firm is forbidden by the regulators or finds it really wanted a different company or can’t get financing or whatever. In this case, I particularly like the experience level of the principals in knowing “when to hold 'em and when to fold 'em.” And I like what the following two charts so clearly show.

It’s always, always about risk and reward. You can’t really compare an M&A fund to the Standard & Poor's when it comes to performance in a bull market. But performance over time is another matter! As you can see Vivaldi compares, quite favorably, to both bonds and the S&P. More importantly, given my concerns for the next few months, is where it falls on the risk continuum, which is to say, it barely registers. We are buyers.

I also see opportunity for income investors from the exodus of smart money from China and other less-stable, overregulated regimes in Asia. That will be the subject of my next article.

Disclaimer: As ”‹a ”‹registered investment adviser, ”‹it is essential to advise that ”‹I do not know your personal financial situation. The information contained in this communiqué represents the opinions of the staff of Stanford Wealth Management and should not be construed as "personalized" investment advice.

Past performance is no guarantee of future results, rather an obvious statement but clearly too often unheeded judging by the number of investors who buy the current No. 1 mutual fund one year only to watch it plummet the following year.

I encourage you to do your own due diligence on issues I discuss to see if they might be of value in your own investing. I take my responsibility to offer intelligent commentary seriously, but it should not be assumed that investing in any securities my clients or family are investing in will always be profitable. I do my best to get it right, and our firm "eats our own cooking," but I could be wrong, hence my full disclosure as to whether we or our clients own or are buying the investments we write about.”‹

Start a free seven-day trial of Premium Membership to GuruFocus.