China has many problems, a number of which are structural, not transitory. These are not merely growing pains, though at one time, they could have gone in that direction.

After Mao's death, new leader Deng Xiaoping recognized that the country was failing under its communist economic system. His visits to Thailand, Malaysia and, in particular, Singapore (where he met with Prime Minister Lee Kuan Yew, the capitalist architect of Singapore's resurgence) convinced him that drastic change was needed.

Impressed with Singapore's economic development, respect for the environment and quality housing, he sent tens of thousands of Chinese to Singapore to learn from their experience. Lee advised Deng to stop exporting bankrupt communist ideologies to Southeast Asia, advice that Deng chose to follow.

However, everything changed after Deng's 14 years of leadership, during which China opened itself to the world, followed a path of living with its neighbors and lifted itself from the poverty and destruction of communism. Deng's final years were weakened by his association with Tiananmen Square in 1989 and, upon his resignation, the ensuing power struggles resumed among the elites who had lived so well under the old totalitarian system.

These struggles continue behind the scenes today. China is still, on paper, a socialist nation (the Chinese press still refers to it as socialist/communist but is increasingly dropping the latter term), but like so many other "people's republics" it is divorced from the needs of most of its people and fails to enjoy any republican principles. It has become, instead, just another autocracy, founded upon oligarchic striving for individual power and individual wealth.

What does this have to do with investing in U.S. real estate and real estate securities? During the transition from communism, hundreds of thousands of well-placed insiders and Communist Party members were handed significant shares of state-owned companies, often based solely upon their position of power or loyalty to a winning faction. Along the way, as the Chinese stock markets sizzled, they were able to sell their shares to less sophisticated investors who believed stocks would only rise forever.

Of course, as easily as all this wealth was granted, it can as easily be clawed back, as today's much-publicized seizures of wealth for either real or trumped-up transgressions makes readily apparent.

This minority who possess such assets realize the party may be coming to an end and are looking for a safe haven for their money. They are increasingly sending it to Europe and the Americas, with the lion's share of the latter coming to the U.S. and Canada.

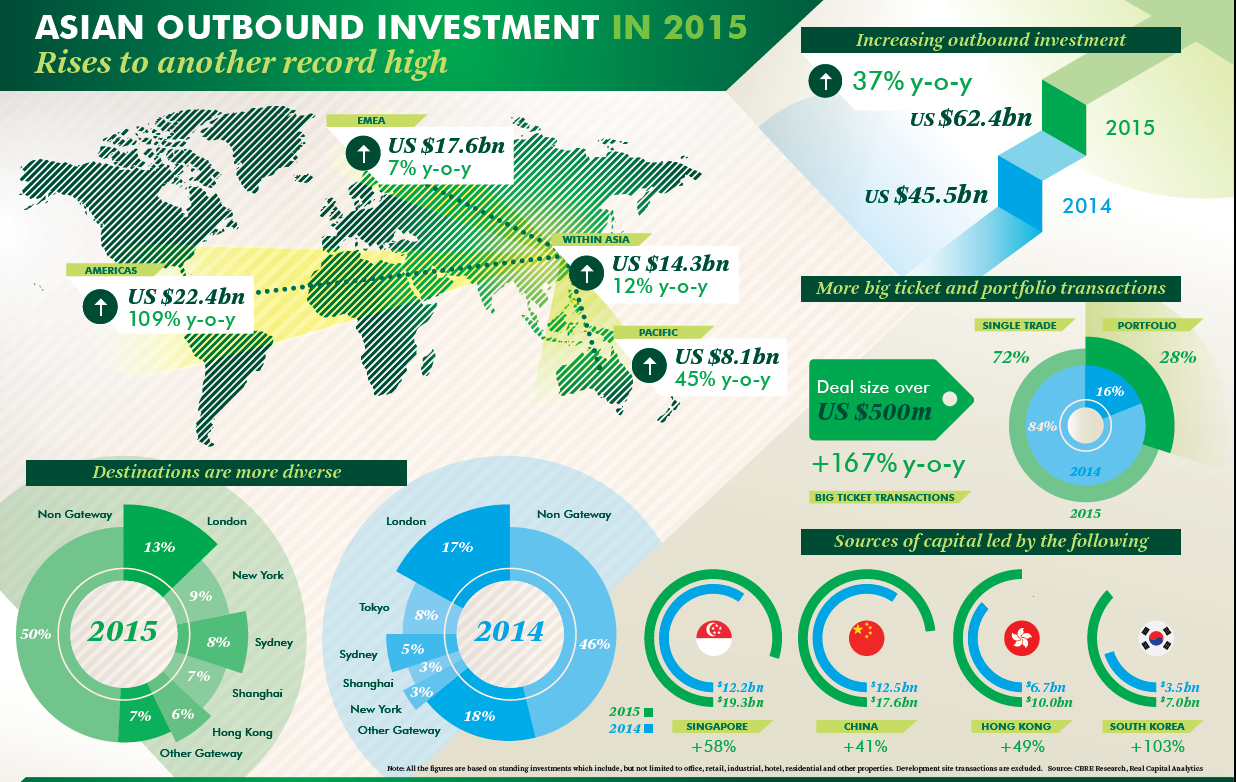

The figures below, from U.S.-based global real estate giant CBRE Group (CBG, Financial), do not include any outbound Asian investments into other nations' stocks or bonds. It is a look solely at Asian (mostly Chinese) investment in office, industrial, hotel and residential properties, expressed in U.S. dollar values.

A total of $62.4 billion left Asia for other safer destinations in 2015. As you can see, the bulk of that – all but $13.5 billion – came from China, Singapore and Hong Kong, with the latter two often way points along the path from China to other destinations.

Where did the total amount go? More than $14 billion was sent within (and staying in) other Asian nations, $8.3 billion went to Pacific nations (almost all of it to Australia and New Zealand), $17.6 billion found its way to Europe and $22.4 billion came to "the Americas."

Does it seem odd that so much cash would go into real estate rather than the far more liquid stock and bond markets? It shouldn't. The markets might provide a greater return, but for a nation that was primarily agrarian – as China was during the youth of most of those with money to sequester today – the land is the land.

Think Tara. (The last moments of "Gone With the Wind" find Scarlett O'Hara hearing her father Gerald say, "Land's the only thing that matters; it's the only thing that lasts," as well as Rhett Butler's voice from happier times, "It's from this you get your strength, the red earth of Tara.") Land is solid. Land lasts. And Will Rogers' dictum from 1930, usually shortened and misquoted as "Put your money in land because they aren't making any more of it," still makes sense today.

The Chinese are listening – and investing. The more China's leadership makes a show of clamping down on bribery, nepotism and ill-gotten gains, the more money will stealthily flow out of the country. The leadership is actually between a bit of a rock and a hard place. It is trying to become more transparent and responsive to Western demands for less bribery, etc. in order to attract Western investment, which has slowed down in recent years. But the more it does to placate Western governments and corporations, the greater the stream of Chinese money leaving China.

It is my belief that five sectors of the real estate market are most likely to benefit from new investment, whether from Asia, Europe, Latin America or elsewhere. I prefer, for the most part, to invest in these areas via real estate investment trusts (REITs) whenever possible.

The five sectors are: self storage (as a nation, we have too many "things" but are loathe to part with them), senior living (they ain't making any more land, but every month a quarter million Americans turn 65), student housing (as long as the federal government keeps promoting student loans and hints they will be forgiven, hundreds of thousands more will apply for college), medical office buildings and facilities (did I mention that every month a quarter million Americans turn 65?) and triple net lease commercial properties.

Sectors specifically seeing likely inflows from Asian, particularly Chinese, investors also include commercial, hotel and high-end retail properties.

In our Investor's Edge ® Growth and Value portfolio, we already own a large percentage of REITs. We own shares of Starwood Property Trust (STWD), the largest commercial real estate lending, servicing and investing company in the U.S. As the biggest originator of commercial mortgages, Starwood will see increasing revenues and earnings going forward – and that increasing revenues and earnings may prove to be a rarity among most US sectors and companies.

We also own National Health Investors (NHI – health care), Public Storage preferreds (PSA – self-storage), Blackstone Mortgage Trust (BXMT – a mortgage REIT), Physician's Realty (DOC – a medical facilities REIT), EPR Properties preferred (EPR – recreational properties like movie theaters) and Stag Industrial preferred (STAG – an industrial properties REIT).

Given that the current market as measured by the SPDR Standard & Poor's 500 (SPY) is no higher today than it was nine months ago, I plan to raise the percentage of real estate equities and preferreds from a current 17% of the portfolio to 22% to 27%. If the market cannot break out decisively from here, we'll be happy with a 6% yield on this portion of our portfolio. If it does, these will participate in the rally. And if it declines, that 6% yield will give us a cushion against the decline as more investors flock to the greater stability of real estate holdings.

I will write four more detailed articles about four of my favorites in the next two weeks. If you are an investor who prefers to buy a basket of REITs to get started, may I suggest for your due diligence Cohen & Steers Quality Income Realty (RQI). Cohen & Steers is a closed-end fund selling at a current discount of 8.3% and with a quite respectable yield of 7.4%. It is an equity fund that holds some of the biggest names in U.S. REITs – firms like Simon Property Group (SPG), Equity Residential (EQR), Public Storage, Omega Healthcare (OHI) and Vornado (VNO).

Cohen & Steers covers the waterfront. It owns common stocks and preferred stocks, but mostly real estate investment trusts. Interestingly, when I run the numbers for the fund since its inception in 2002, I find it has actually beaten the S&P 500 in total return – even during this bull market from 2009 forward. It has also beaten the Vanguard REIT ETF (VNQ) despite Vanguard's much-touted low expenses! So much for the "just buy index funds with the lowest expenses" mantra.

U.S. REITs and other real estate firms are situated for further growth this year. While the real American economy is merely plodding along, other nations are doing worse. As a result, a lot of foreign capital is coming to the U.S., and real estate is what most of these sovereign wealth funds and wealthy individuals know best. Unlike many of the nations from which these funds will flow, the U.S. real estate market is stable and seen as a safe haven. Please stay tuned for the next four discussions of our favorite individual real estate investments!

Disclaimer: As ”‹a ”‹registered investment Adviser, ”‹it is essential to advise that ”‹I do not know your personal financial situation so the information contained in this communiqué represents the opinions of the staff of Stanford Wealth Management and should not be construed as "personalized" investment advice.

Past performance is no guarantee of future results, rather an obvious statement but clearly too often unheeded judging by the number of investors who buy the current No. 1 mutual fund one year only to watch it plummet the following year.

I encourage you to do your own due diligence on issues I discuss to see if they might be of value in your own investing. I take my responsibility to offer intelligent commentary seriously, but it should not be assumed that investing in any securities my clients or family are investing in will always be profitable. I do our best to get it right, and our firm "eats our own cooking," but I could be wrong, hence my full disclosure as to whether we or our clients own or are buying the investments we write about.”‹

Start a free seven-day trial of Premium Membership to GuruFocus.