Sitting pretty at the top of the general purpose payment card industry are two of the most “weather-proof” companies in the world - Visa (V) and MasterCard (MA). Together, they control more than 80% of the industry and although they’ve lost some market share over the past year or so, they remain the two largest players in this space.

Source: Nielsen

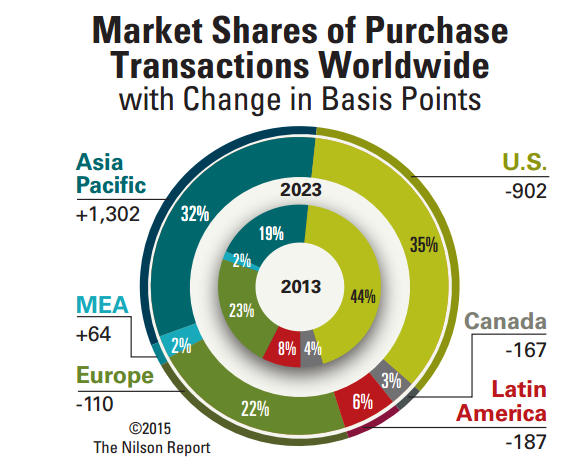

With a projected $468.61 billion in transactions by 2023, the industry itself is growing at a rapid pace with Asia Pacific, Middle-East and Africa being the potential key drivers of that growth. Surprisingly, the estimates for mature markets actually shows negative growth in transaction value over the same period, with the U.S. leading that decline.

Other players in this game include Discover (DFS, Financial), American Express (AXP, Financial), Diners Club, UnionPay and other electronic fund transfer companies.

That brings us to the real nature of the competition.

What’s the competition for Visa and MasterCard?

One of the biggest external threats to card-based payments has always been PayPal (PYPL, Financial). With a market share of over $280 billion in transactions as of 2015, PayPal is equally strong, but in a different sub-segment of the industry - online transactions.

PayPal and Visa recently announced a partnership where they can each create more opportunities for themselves, but they’ll always remain fierce competitors.

The other possible rival is MCX, or Merchant Customer Exchange, a mobile payment system that was jointly launched by some of the biggest retailers in the world like Wal-Mart, Best-Buy and Target - and, surprisingly, Exxon-Mobil. However, card operators have a wide moat to their business because of the sheer number of locations at which their products can be used. For MCX to grow into any sort of scale is going to take a long time, if it happens at all.

Besides that, there are very few disruptive technologies in the payment space other than mobile wallets and possibly biometric payment verification systems such as PayPal’s Venmo.

Though arguably viable, any kind of global payment system requires hardware and software to be supplied to millions of merchants. And there’s always the possibility that either Visa or MasterCard will quickly move to acquire any tech that could be detrimental to their own market shares.

That moat is what makes these two stocks so “investible”; some might invest for the dividend returns or capital gains, but it’s really the rock solid moat that is the biggest reason. However, as an investor you need to understand all aspects of this business.

Let’s first look at their dividend health.

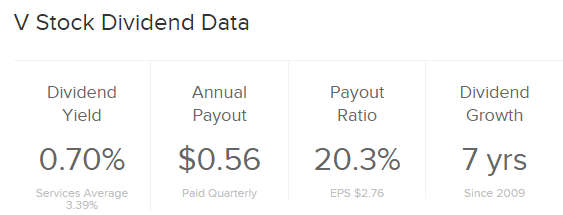

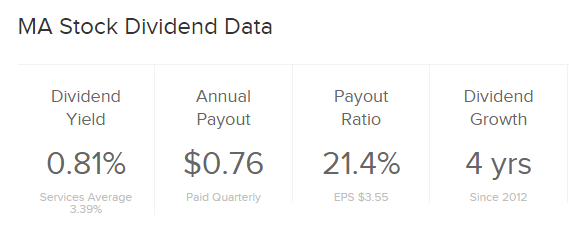

Dividend yield

Source: Dividend.com

Source: Dividend.com

Dividends for both companies are not what you would call enticing, but that’s probably the wrong way to look at it. Even as part of your dividend portfolio, these stocks are going to keep growing for a long, long time. Investing in companies with this kind of a moat is going to serve you long after you’ve divested your portfolio of all those high-growth companies that will have to taste disruption in one way or another.

With Visa and MasterCard, that longevity will give you benefits that will accrue year over year. Moreover, the fact that their payout ratios are near the 20% mark translates to growing dividends over a long period of time.

What about their business health?

The best part about these businesses is that they are high-margin, low-capital companies. Should it be surprising, then, that both of them feature in Warren Buffett (Trades, Portfolio)’s portfolio?

With operating margins over 50%, the scale they’re reached is obviously driving their bottom lines stronger by the year. That’s great news because it makes their moat even stronger. Any new company in this space would necessarily have to sacrifice margins for growth because of the sheer quantum of capital they would have to pump into the business for several years.

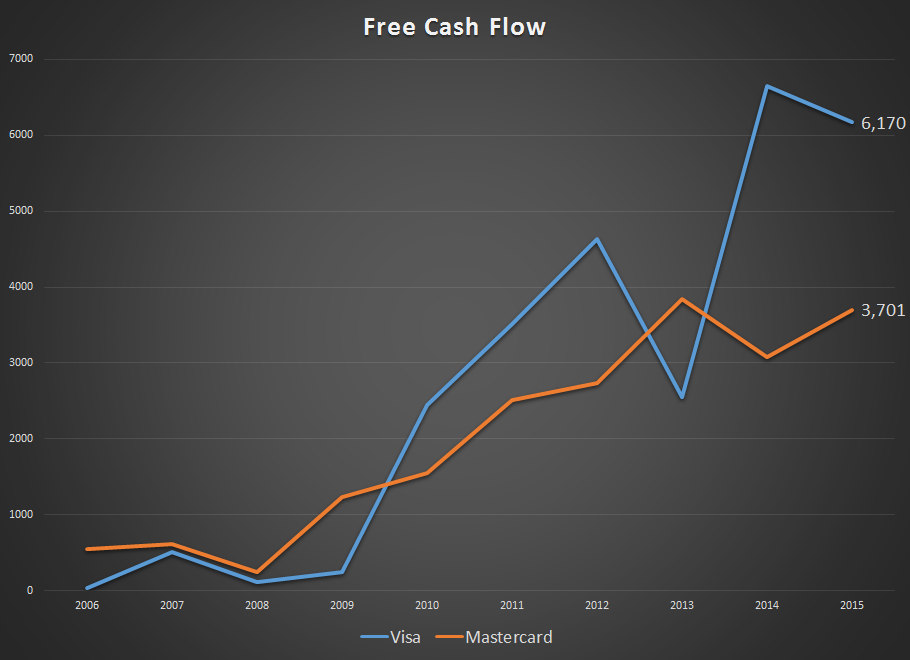

In terms of free cash flow, Visa’s FCF has grown from $435 million in 2006 to $6.1 billion in 2015, while Mastercard’s moved from $556 million to $3.7 billion. As you can see, cash flow has increased along with their operating margin improvement, clearly pointing to the widening gap between these two companies, the competition between them and the scale at which both these companies are operating.

Their global reach, size and scale will be a hard nut to crack for any other company. This has grown so massive in terms of their reach that even new mobile wallet payment systems are actually piggybacking on these payment providers. Even PayPal recently signed an agreement with Visa, further cementing their place in the world of purchase transactions.

These two are among the very few companies that pushed through the Great Recession like it didn’t happen, and this shows how heavily our society is dependent on credit - especially when a major crisis hits.

Another metric to keep your eye on is capital expenditures. Capex for both has been less than $500 million per year. You don’t often see a 3.5% Capex with companies that are growing stronger each year. That’s the reason they exhibit healthy cash flow levels.

Let’s also look at their balance sheets to see whether they should be in your dividend portfolio.

This is actually the cherry on top of the whipped cream. Visa’s LTD was $15.87 billion and cash in hand was $15.94 billion; MasterCard’s LTD was $3.3 billion and cash was $4.9 billion.

There’s no longer any need for them to dip into debt to keep growing. Unless a major acquisition opportunity comes along, I expect it to stay that way for a long time.

The investment opportunity

It should be obvious by now that investing in both companies makes more sense than just having one of them in your portfolio.

Such an investment should ideally run on autopilot, so a dividend reinvestment plan would probably be ideal.

Any concerns about dividend yield will hopefully be offset by the sheer stickability and resilience of these businesses. Cash flow growth, low Capex, market leadership, strong balance sheets, high margins and low payout ratios will tempt the most skeptical of dividend investors.

Having said that, the timeline for investment is very important. This is not something you buy and then sell at the earliest opportunity to take home the money. This should be the last thing on your portfolio to be liquidated, if it ever comes to that.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.Â