Automakers around the world are going through a terrible time at the hands of investors. Market sentiment is so bearish on the industry that not even Toyota (TM, Financial), the largest company by market capitalization, and Tesla (TSLA, Financial), the best disruptor in the industry, are being spared.

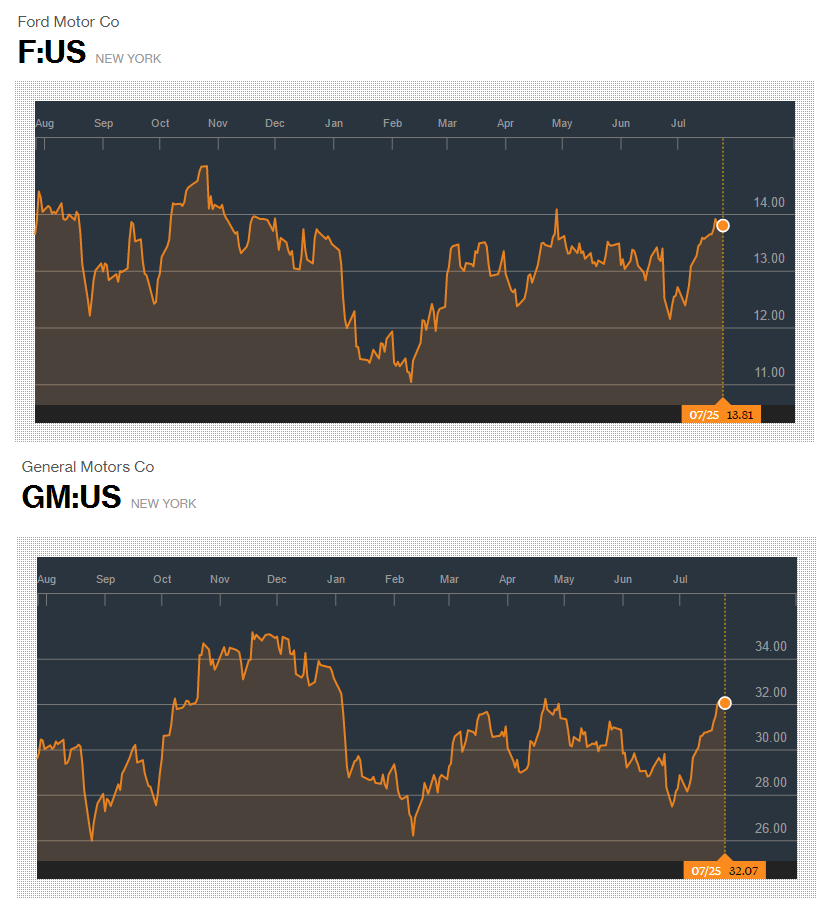

Of the top four companies –Â Toyota, Ford (F, Financial), Honda (HMC, Financial) and General Motors (GM, Financial) – only Honda is trading with a double-digit PE ratio while the other three are well below 10, indicating the bearishness in the market. The stocks of all four companies are down this year with the exception of Ford, which shows a measly 2.66% increase thanks to the best quarterly results the company has ever posted.

Source: Finviz

But that was last quarter. Under normal circumstances, just an earnings beat should move the stock nicely, but the sentiment is so negative that Ford’s above-average results and record-breaking first-quarter results barely made the stock move. There are several things that are weighing heavily on these companies’ stocks, especially General Motors and Ford.

The peak auto sales myth

If you take a closer look at both GM’s and Ford’s stocks, you will notice that both of them started plunging after November 2015, and then started recovering by February, mostly moving sideways since then. But that’s not the only similarity between both stocks. It was around this time that the theory of U.S. having reached peak auto sales gained momentum, and the implication was that since we are at the peak, the sales can only go one way –Â down.

That theory turned out to be a myth, and the doomsday scenario predicted by analysts has not arrived to date. I don’t think it will happen again unless we enter a credit crunch phase in the U.S. economy – or the economy itself starts contracting.

Here’s why I think that will be the case.

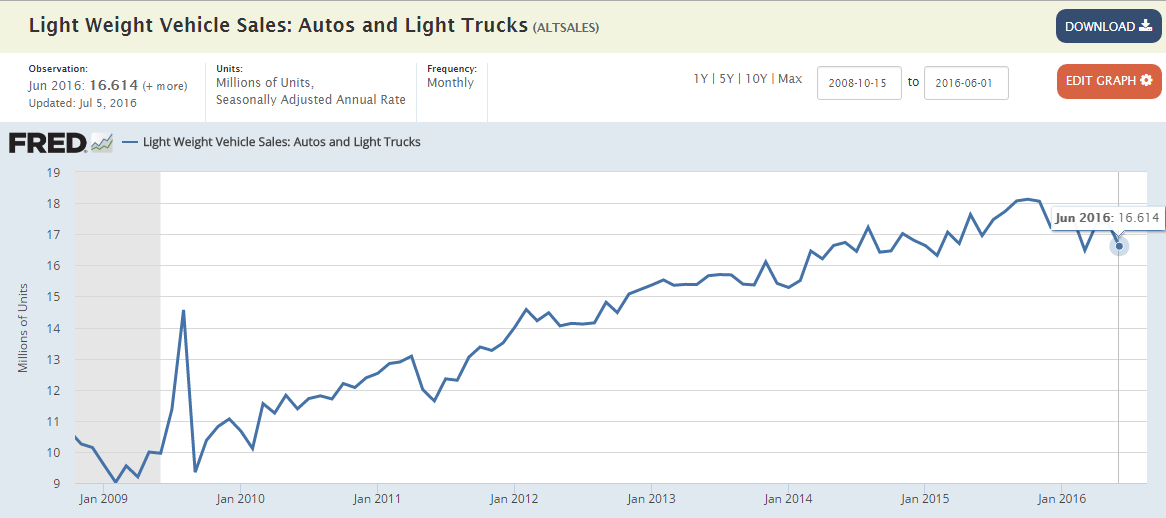

Source: FRED

Auto sales have recovered nicely with the economy and, as you can see from the lightweight vehicle sales in U.S., it breached 18 million units around October 2015 – exactly a month before the auto stock rout began. In December sales fell to 17.22 million units from 18.05 million in November, sparking off the “we have peaked and therefore the only way is down” theory.

To a great extent I, too, agree that we are somewhere near the peak potential of auto sales in the U.S. What I don’t agree with is the second part of that theory – that things can only go downhill from here.

Sales reached a peak because conditions were favorable to create the demand, and the supply was there to fulfill it. Unless the underlying conditions change in a drastic manner, I don’t see any reason why monthly sales will change dramatically. However, since the industry itself is a cyclical one, we will see the normal ups and downs we have always seen.

The U.S. economy is projected to grow at 1% to 2% until 2020 so there is no macroeconomic threat to the market as of now.

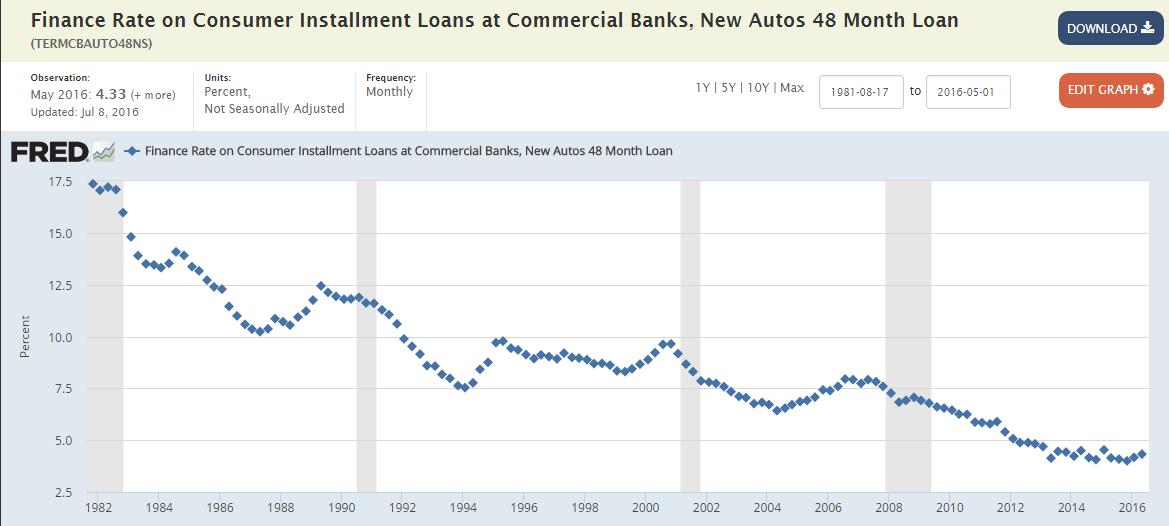

The other key factor that most analysts keep ignoring is credit availability and interest rates. Unless the economy shrinks, credit is going to be available; and as long as interest rates stay where they are, it is logical to expect auto sales numbers to stay within a tight range instead of randomly jumping up and down. But from the way Ford and GM stocks have been moving, you would think that disaster is just around the corner.

Take a closer look at how interest rates have moved since the recession – they kept going lower and lower while auto sales started going higher and higher. Both of them are inextricably interrelated. If you look closer, since 2014 auto interest rates are looking quite stable; in tandem, auto sales also started moving within the 16 to 18 million range.

Source: FRED

The investment angle

Interest rates are going to rise at some point, but we all know that it cannot happen overnight. And to be quite frank, nobody knows how many years it might take for us to get back to pre-recession interest rate levels. That means we’re not going to be seeing auto sales slide into the Pacific Ocean just yet – at least not during the next two quarters.

The U.S. is a key market for both Ford and GM, and both companies depend on it. As such, what happens here directly affects their profitability and, thereby, the stock as well. With the U.S. economy expected to chug along at a decent pace, Ford and GM are being unfairly punished for a theory that has so many holes we can see right through it.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.