UPS will be reporting its second quarter earnings results on July 29 before markets open.

2015 was a great year for United Parcel Service (UPS, Financial), and the trend continued during the first quarter of the current fiscal with the company posting 10% growth in quarterly income while revenue increased by 3.2% to $14.42 billion.

Over the past half-decade, revenues have been growing in a steady manner, and the last fiscal saw UPS reaching an all-time high on operating profits.

There seems to finally be some stability in International package revenue. In the first quarter UPS posted flat revenue growth on a constant currency basis, but operating profits increased by 15% year over year to $574 million.

The last mile shipment is typically the most expensive leg for any logistics company, and residential deliveries rose 6% during the first quarter, but thanks to the increasing emphasis on efficiency UPS was able to expand its margins instead of going the opposite way.

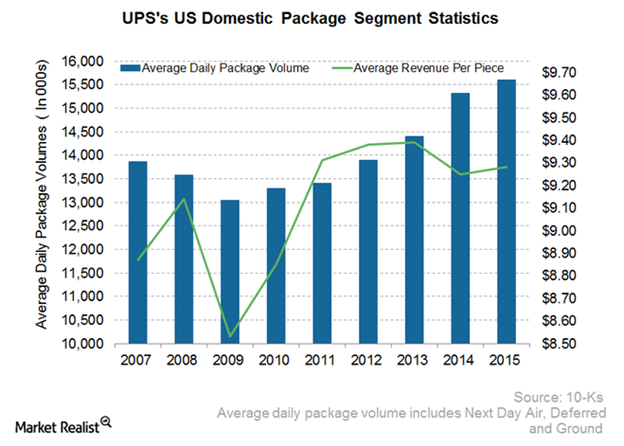

“The company increased U.S. domestic package operating profit by 7.6% to $1.1 billion and expanded its operating margins as the company reduced its average cost per package by 1.9% through efficiency gains and lower fuel costs. Average daily U.S. package volume increased by nearly 3%.” –Â Wall Street Journal

The big question here is whether 2015 was just a lucky strike or whether it's been growing at a sustainable rate.

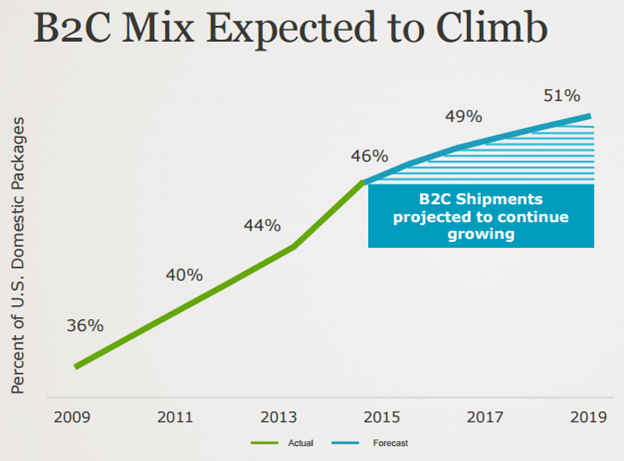

Key movements in ecommerce

UPS fully expects to ride the ecommerce tide that is sweeping across the U.S. By 2019 the company expects to hit 51% domestic B2C (business to consumer) deliveries by volume.

Under normal circumstances, this would not be good news for any parcel delivery company. UPS, on the other hand, has managed to improve margins in this segment and turn a profit on it –Â unlike Amazon (AMZN, Financial), which still continues to struggle with last mile shipping costs.

That’s the kind of operational efficiency that differentiates a pure-blood logistics and transportation company from an ecommerce company that also tries to handle its own shipping needs. Amazon does use UPS as well as FedEx (FDX, Financial) for its delivery needs but is increasingly trying to handle some of its needs on its own, such as peak season excesses. However, it's not seeing the kind of gains it expects.

UPS, on the other hand, seems to be an expert in cost efficiency, and it shows in its operating income for this segment, which expanded 50 basis points to 12.1% in the first quarter despite 46% of packages being for ecommerce customers.

UPS has been growing its revenues at a slow but steady pace over the past five years. That continued into the first quarter as well. If you look at the mature and developed markets in which UPS has a significant presence, that kind of growth is great for such markets because you can’t really expect double-digit growth there.

International packages

The biggest concern has been UPS’s performance overseas. The international packages segment that includes small package operations in Europe, Asia, Canada, Latin America, the Indian subcontinent, the Middle East and Africa, has been experiencing flat growth since 2011, and revenues dropped during the first quarter.

The problem with the international market is the intense competition as much as economic headwinds. The FedEx acquisition of TNT will exacerbate the problem, and things aren’t going to get any easier moving forward. That’s the number I will be keeping my eyes on when the second quarter call comes around in the next few days.

Despite lukewarm revenue growth, there’s no doubt that UPS is becoming more efficient in its operational capabilities. That’s true at home and overseas, but home market efficiency has been solely responsible for its five-year growth spurt through 2015.

The pivotal factor, however, seems to be its international markets. If we see significant gains there at the second-quarter earnings call, then UPS stock has only one way to march – and that’s upward.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.