When a company announces operating profits dipped 57% that quarter and net income dropped 39%, you would expect more than a mere 5% hit on share price. But, that’s exactly what happened to Under Armour (UA, Financial) yesterday.

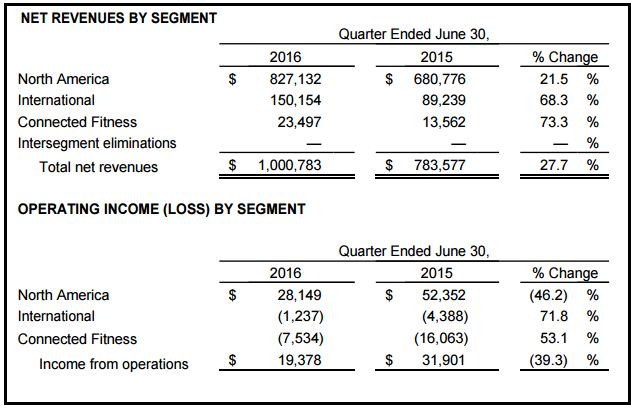

Having cited the liquidation of their largest seller, Sports Authority, as the primarily reason, UA posted $6.34 million in quarterly profits and $19 million in operating income during the second quarter call on Tuesday, July 26. That’s down from $14.8 million and $32 million, respectively, from the same period last year.

If it were any other high-growth company, the stock would have taken a much bigger hit. However, even though UA is trading at about 50 times its forward earnings, investors seemed to take it in stride, only punishing the shares by a small margin.

Under Armour also revised their sales growth guidance for the fiscal year from 26% to 24%. Considering they’ve lost their biggest retailer, that’s understandable. However, it’s good to see them bounce back with the announcement of Kohl’s starting to carry their brand. This is especially important for the West Coast market, where Kohl’s has 100 stores, and follows closely on the heels of two marketing agreements they have signed with Cal Berkeley and UCLA.

“This decision to reach new consumers through Kohl's is not a channel consideration but a consumer consideration. We want to reach our consumers where they expect to find Under Armour products, and we'll continue to partner with the retailers that provide us the opportunity to showcase the Under Armour brand.”

The Investment Angle

One thing is clear, the market did not see the profit meltdown as a trend. Rather, they recognized this was an isolated event that had extremely low odds of being repeated in the future. However, it also shows the risks are high when the stakes are high. Such an event can shake things up at the most basic level - sales and profitability. That’s one lesson UA will never forget and, hopefully, they’ll spread their sales risks a lot more evenly moving forward.

Third quarter growth is now expected at a modest 20%; modest, because until now they’ve been growing much faster. They’re targeting 24% this year, but they’ll need to at least maintain that if they want to hit their goal of $8 billion by 2018. That’s the lowest they’ve done since 2009 and it seems to be a baseline growth figure for Under Armour to reach their 2018 goal.

While it’s okay to look at the 5% stock drop as an isolated incident, if you’re investing in UA stock then you need to keep in mind that this is still very much a high-growth company. The market may not forgive them another major transgression. In fact, even minor shocks will likely hit stock prices by more than a mere 5%. If UA doesn’t meet and beat the 20% growth target in the third quarter, we may well see that happening.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.