Gilead’s (GILD, Financial) misfortunes continue to hammer the stock. Since the stock’s spectacular run from under $20 in 2011 to near $120 in 2015, it has been on a slide and is now trading at seven times earnings, the lowest trading multiple among the top 10 pharmaceutical companies in terms of market capitalization.

The stock is a strong buy despite the market thinking otherwise, and I covered my reasons in detail in my earlier article "An Unfair Valuation Makes a Great Investment."

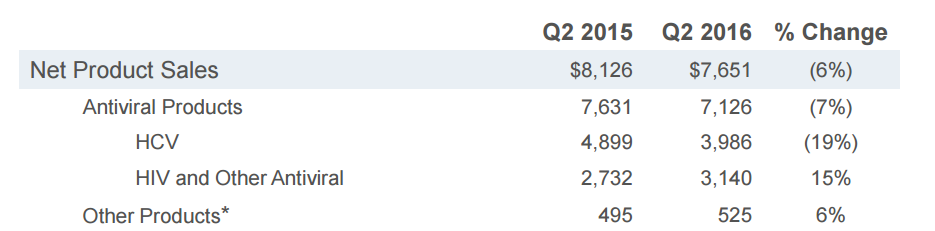

Gilead’s second-quarter earnings results did nothing to soothe investor sentiments as the company revised its revenue guidance downward from between $30 billion and $31 billion to between $29.5 billion and $30.5 billion. Despite the company managing to beat earnings estimates with EPS of $3.08 on the back of $7.78 billion revenues, the downward revision of sales projections for the year hurt the sentiment as well as the stock.

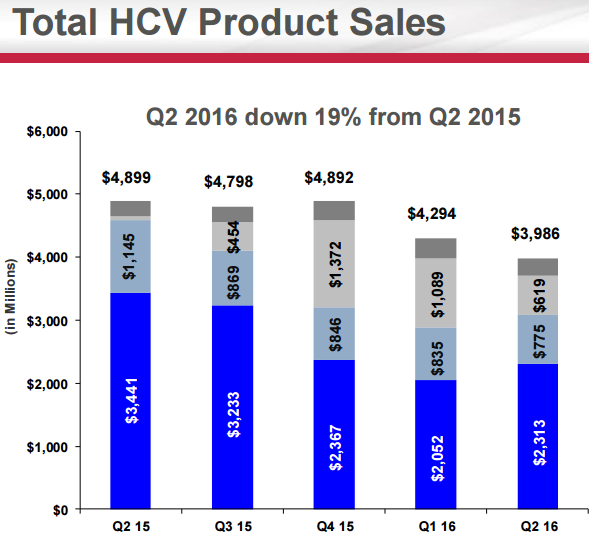

The company lowered its outlook on lower expectations with revenues from its HCV franchise, which was down by 18.6% during the quarter compared to the prior period, causing a 7% negative net impact on the antiviral segment.

“We are lowering net product sales guidance to a range of $29.5 billion to $30.5 billion. While we are seeing continued strength in non-HCV product sales, given the current trends in payer and patient flow dynamics for HCV, our updated models suggest net product sales will range from being slightly above to slightly below $30 billion for the year. As such, we believe it is prudent to update our full-year 2016 guidance.” – Robin L. Washington, chief financial officer and executive vice president, second-quarter Earnings Call

Total product sales were $7.6 billion during the third quarter, down 6% year over year, and the loss of sales can be directly attributed to the HCV franchise that included its star performers Harvoni, Sovaldi and Epclusa. Sales dropped to $4.0 billion from $4.9 billion last year.

Meanwhile, HIV and other antiviral franchises saw sales reach $3.1 billion, up 15% from $2.7 billion last year. The growth in the HIV segment was not good enough to compensate for the losses in the HCV segment, resulting in the 6% drop in overall revenues.

Things are not great in the short term as the HIV segment is not yet in a position to balance out the growing losses in the HCV franchise, and the company is still looking for that elusive billion-dollar product that can save its position.

The way the stock is being treated, you would think Gilead is going to drop off the edge of the earth. That’s a very unrealistic view, and the company looks extremely appealing when you factor in its balance sheet as well as its hefty pipeline.

At the end of the second quarter, Gilead had $24.616 billion cash on hand and long-term debt of $23.421 billion. There is enough firepower in its balance sheet for the company to actively pursue an “offset acquisition” for sliding revenues. As of now there are no visible plans for that, but it has the cash leverage if it is needed.

From a valuation perspective, and due to the strength of its balance sheet, Gilead is an extremely appealing investment that should pay off in the medium term.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.