GlaxoSmithKline (GSK, Financial), the British pharmaceutical giant, is yielding 5.07%. That’s much better than your average fixed deposit income would net you, and when you have a company that once proudly sat in Warren Buffett (Trades, Portfolio)'s portfolio then you are looking at a solid income earner for a long time.

But why is GlaxoSmithKline offering a more than 5% yield. Is there anything that we need to know before taking the plunge? Let’s check GlaxoSmithKline’s numbers and see if its dividends are safe.

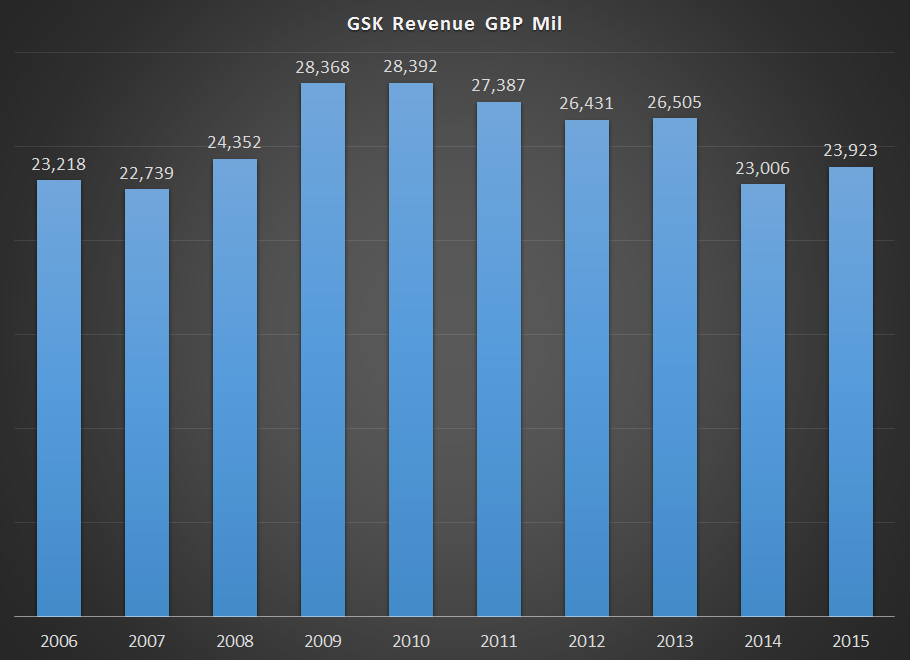

Revenue growth

In terms of revenue growth GlaxoSmithKline is nearly where it was 10 years ago, making 23.92 billion pounds ($31.24 billion) in 2015 compared to 23.218 billion pounds in 2006. It moved from 23 billion pounds to 28 billion pounds right through the recession only to see its numbers cut back to 23.92 billion pounds in 2015. It’s a bit of a surprise to see a company see its sales numbers grow when the world is contracting and do the opposite when the world economy is slowly expanding. But that was GlaxoSmithKline’s reality.

One of the reasons for that contraction was the sale of its oncology portfolio to Novartis for $16 billion. GlaxoSmithKline felt that it did not possess the scale to keep promoting legacy products when it had an immuno-oncology division to take care of.

On the positive side, GlaxoSmithKline does expect its pharma unit, which brings the lion's share of its revenues, to get back to the growth path this year. But the real key to its overall revenue growth as well as future is the way it is transforming itself into a more diversified company with revenues flowing from pharma, vaccines and consumer health care. Though not exactly in the mold of the earlier avatar of Johnson & Johnson (JNJ, Financial), GlaxoSmithKline wants to create revenue streams that can work on their own. It's a risky move that can only pay off in the long term, and it's the one that I sort of prefer, to be honest.

Balance sheet strength

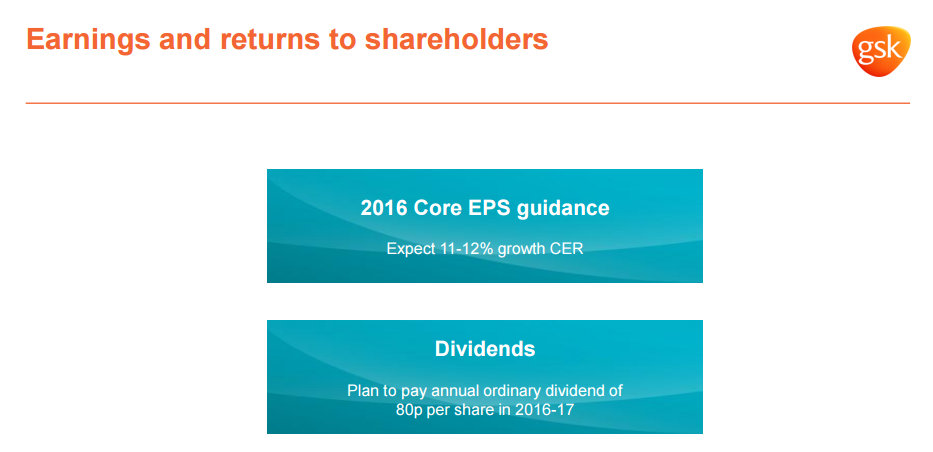

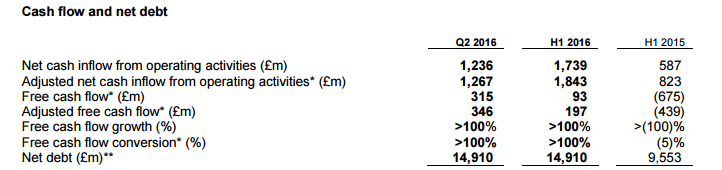

At the end of the second quarter GlaxoSmithKline had 4.67 billion pounds cash on hand with long-term debt of 15.098 billion pounds. With an operating income of 10.322 billion pounds in 2015, the balance sheet doesn't seem to be in trouble until you look at the payout ratio and the free cash flow metrics. The patent expirations of its top drugs have pushed the company so much that the company’s cash flow has been all over the place. Thanks to its sale of oncology assets to Novartis (NVS, Financial), GlaxoSmithKline had some breathing space to keep its dividends flowing and keep its future plans intact. The company announced that it plans to keep the dividends at 80 pence per share until next year as it works to turn its business fortunes around.

Â

From GlaxoSmithKline’s second-quarter press release:

“At June 30, net debt was 14.9 billion pounds, compared with 10.7 billion pounds at Dec. 31, comprising gross debt of 19.6 billion pounds and cash and liquid investments of 4.7 billion pounds. The increase in net debt primarily reflected dividends paid to shareholders of 3.0 billion pounds as well as a 1.3 billion pounds adverse exchange impact from the translation of the non-Sterling denominated debt. “

GlaxoSmithKline had to dip into its debt bucket to make its dividend payment, not an ideal situation for a dividend investor who wants to buy into the company for the long term.

My take

With free cash flow staying well below 1 billion pounds and total dividend payments at near 3 billion pounds, GlaxoSmithKline’s ability to pay dividends is reliant on its balance sheet strength more than anything else during the short term, and it sort of explains why GlaxoSmithKline’s yield is staying north of 5%.

GlaxoSmithKline still earns more than 23 billion pounds, and the debt level is not extremely high although it will run up a bit before the sales numbers start growing. From a dividend perspective this is an extremely risky stock, which is why the reward is also high.

The company is pushing hard to become a diversified entity, and it can pay off in the long run as it reduces pipeline/blockbuster drug dependence. The company has its eyes on the bigger picture and, as such, if you are ready to add a bit more risk to your portfolio then the reward is actually there.

Disclosure: I have no position in any of the stocks mentioned and no intention to initiate any position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.