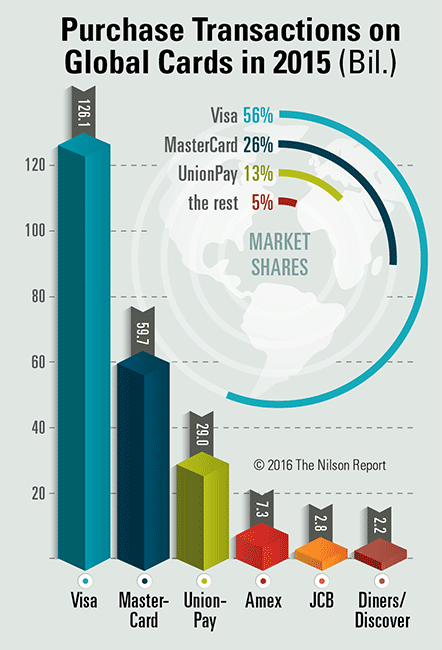

Discover (DFS, Financial) has been living in the shadows of Visa (V, Financial) and MasterCard (MA, Financial) for a long time, and aside from American Express (AXP, Financial), no other company in the industry has been able to scale up with significant market share. These top three players controlled more than 82% of the total transactions around the world in 2015.

But the underdog, Discover, looks like an extremely attractive investment. The company is currently trading at 2.8 times its sales - far less than Visa’s near 14 times and Mastercard’s near 11 times valuation. Although Discover’s revenues have not exactly been on fire, they have been extremely steady in the last 10 years, and the company still managed to expand its operating margins from near 30% levels in 2006 to near 40% in 2016.

Discover is also a well-managed company. Free cash flow has more than doubled in the last 10 years, while capital expenses remained stable in the $100 million to $200 million range.

One of the biggest problems Discover faced for a long time, and still continues to face, is its acceptance at merchant locations. Being a much smaller player compared to the top three has never helped their case, but the company has done its best to improve its merchant acceptance rate.

Back in 2014, WSJ wrote:

“One long-time knock against Discover was that the credit cards on its network weren’t accepted by as many merchant locations as Visa and MasterCard. But the number of locations accepting Discover has been on the rise. Roughly 9.2 million locations in the U.S. accepted credit cards on the Discover network in 2013, up 2% from 2012 and up 24% from 2009, according to data from the Nilson Report, a payments-industry newsletter. The number of U.S. locations that accept Visa and MasterCard, which surpass Discover, increased 15% since 2009.”

The company still has a lot of road to cover. While Visa and Mastercard are well-known brands around the world, Discover is still an unknown entity in several countries. Flip that around and what it means is considerable potential for growth over the next several years. The company has been managing its operations well, but they need to get a bit more aggressive with their expansion plans and get out of Visa’s and Mastercard’s shadows with some strong branding of their own, or find a niche they can dominate, the way American Express has.

The company is trading at less 10Â times forward earnings and it remains an extremely attractive company at this price point. Growth has been stable, free cash flow has grown even faster and there is plenty of room to continue their expansion.

Disclosure: I have no positions in any stocks mentioned and no plans to initiate any positions within the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.Â