Domino's Pizza (DPZ, Financial), the world’s second-largest pizza delivery chain with operations in more than 80 countries, has steadily grown in size in the last 10 years. As a restaurant chain with significant international operations Domino's has proved that its product can be sold all over the world, and with a highly franchised model the company can keep adding to its nearly 13,000 stores at a steady pace.

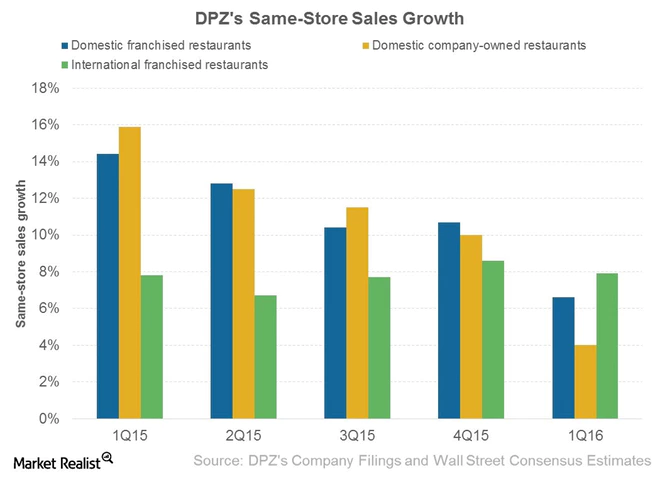

Same-store sales have dipped in the last few quarters from above 12% last year to around 9% this year. The near double-digit growth is still much better than some other big restaurant chains were able to achieve in the last two years.

Thanks to its steady growth and above-average same-store sales performance around the world, Domino's stock price has gone from under $25 to above $150 in five years. The stock is now trading at 40 times its earnings and 3.3 times its sales. In the second quarter Domino's posted a sales growth of 12% on the back of above 9% comps in the U.S. and 7% in the international market. For a company with 13,000 stores it is indeed a huge achievement.

As a heavily franchised model with global presence, improving the store numbers is not going to be a problem for the company. And as long as stores keep opening, franchisees are going to pay their share and Domino’s top line is going to keep expanding. But the problem with trading at 40 times earnings is that it leaves little margin of safety for investors because the company has to keep up with the current pace to sustain that earnings multiple.

Same-store sales cannot grow at double-digit rates forever. Menu innovation, change in product mix and competitive landscape all play a huge role in how many people are ready to walk in through the door and how much extra they are ready to pay for the same product. Footfalls and ticket price are the two things that impact same-store sales, and if the product price keeps growing forever, at some point consumers will start to retaliate by not coming in through that door anymore. It has to ebb and flow with market conditions, as is the natural pattern with restaurant chains.

But a 30 times forward earnings multiple is simply asking for too much growth from a restaurant chain. Things will catch up with Domino’s at some point, and at that point the multiple has to come down to reflect the size of the company. The stock price may grow in the meantime, but the question is: how much more do we stand to gain in that period? The other question is: when will that time come?

As such, with unpredictability adding pressure to the narrow margin of safety, it might not be a good buy right now. The better option would be to wait until the earnings multiple comes down to a more reasonable level that more accurately reflects growth prospects in the long-term future.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.