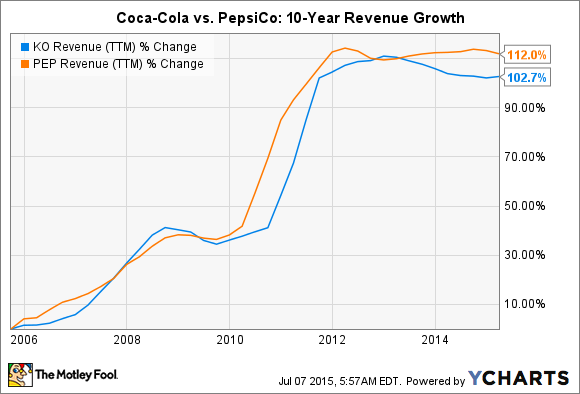

Coca-Cola Co. (KO, Financial), the world’s largest non-alcoholic beverage maker, displays all the signs of a slow moving giant. Revenue growth in the last five years has been declining, operating margin has come down a bit, and soda consumption in the U.S. has fallen to 30-year lows, which has made the environment really difficult for the company to maneuver. PepsiCo (PEP, Financial), their rival, has also followed the same path and both companies have been finding it hard to move their sales needles for the past few years.

But Coca-Cola’s dividend yield of 3.3% is too attractive to let it pass. Despite the slowdown, the company has managed to keep its operating cash flow hovering around the $10.5 billion level for the last five years, while free cash flow has been holding steady around the $8 billion level.

As a dividend investor, the moat is a very important criterion for making an investment. Coca-Cola and PepsiCo have huge moats that have allowed them to exist for more than a century each, and the kind of products they have will still be around long after we are gone. Unlike the technology industry where one brilliant mind and few years of hard work can totally transform the industry landscape, the beverage industry is a traditional one where you have to build your business brick by brick. Once you reach scale, you have the money and you can always buy any promising player that is threatening your space.

At the end of the second quarter of the current fiscal, Coca-Cola had nearly $24 billion in cash and investments, while their long term debt stood at $29.25 billion. For a company that had an annual operating income of $8.72 billion and free cash flow of $7.9 billion in 2015, their balance sheet is strong enough to withstand a recession should one hit right now.

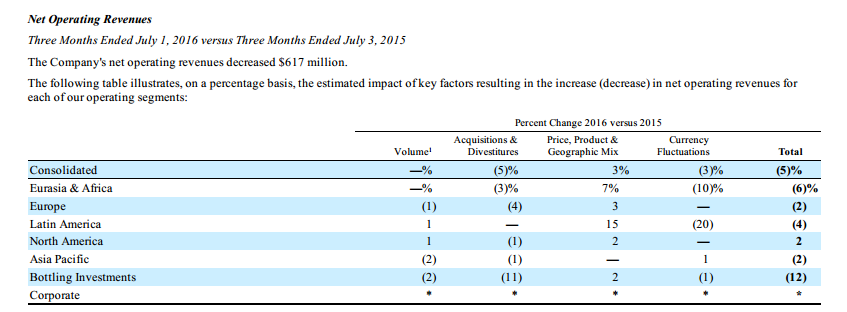

One of the biggest factors contributing to their sales slowdown is Coca-Cola’s international market presence. As a company with significant amount of revenues coming from international markets, Coca-Cola is brutally exposed to fluctuations in the currency market. A stronger dollar has played a huge role in denting their sales numbers, and during the second quarter alone currency headwinds, among other factors, contributed to a 5% decline in revenues.

Coca-Cola reported second quarter 2016 operating results in July, where Muhtar Kent, chairman and CEO, said:

“Despite challenging macroeconomic conditions, structural changes and foreign exchange headwinds which contributed to a 5% decline in reported revenues, we delivered 3% organic revenue growth, gained value share in total nonalcoholic ready-to-drink beverages, expanded our operating margins and grew profits in line with our expectations.”

Coca-Cola has stepped up on cost-saving measures as it navigates the difficult environment, but the company seems to be upbeat about its prospects for the rest of year, expecting 2016 organic revenues to grow 3% and full year comparable currency neutral income before taxes to grow at between 6% and 8%.

The company’s product portfolio, moat and balance sheet strength will allow the company to slowly get out the difficult macro-economic problems they are facing, and the best part of the deal is the 3.3% yield.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.