Intel Corporation (INTC, Financial) has had a good year so far, with the stock moving up by nearly 21% in the last 12 months.

The last five years have been extremely disappointing for the company as revenue growth remained nearly flat, moving from $53.9 billion in 2011 to $55.35 billion in 2015. This was a period that also witnessed the decline of PC sales, which hurt Intel’s breadwinner, the Client Computing Group, as well as Intel’s withdrawal from the smartphone processor segment after investing billions of dollars.

But things returned to normal this year thanks to the stability in PC sales around the world and Intel’s decision to concentrate on the fast-growing data center and Internet of Things segment is an encouraging one. Intel returned to revenue growth this year, posting sales growth of 7% in the first quarter and 3% in the second quarter, and the company is expecting mid-single digit growth in 2016. That means it is expecting the good news to continue through the second half of the year.

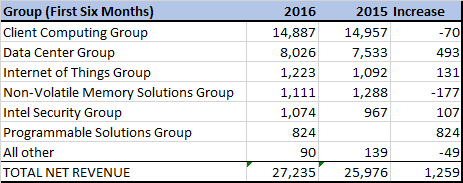

Total sales in the first six months of the fiscal year grew from $25.97 billion last year to $27.23 billion, a growth of 4.8%. Of the $1.2 billion sales increase, nearly half a billion can be attributed to growth in the data center segment, which saw its revenue climb from $7.53 billion to $8.02 billion. Internet of Things grew from $1.09 billion to $1.22 billion. So, clearly, these two segments played a vital role and were the key drivers for more than half of Intel’s growth this fiscal.

The Data Center Group, which includes platforms designed for the enterprise, cloud, communications infrastructure and technical computing, still has plenty of potential for growth. The IoT segment has also been growing, albeit at a slower pace. The industry itself is in its early stages as large-scale implementation of IoT systems is yet to happen. Until that happens, IoT will still have growth but not at the levels we can expect from the data center segment. The latter is obviously a high growth segment due to the accelerating adoption of cloud infrastructure and cloud-related services.

As such, Intel’s short- to medium-term results are dependent on two things: how stable the PC market is and by how much Intel’s data center segment grows. PC sales have been relatively stable this year, giving Intel some breathing space while its data center segment gains more traction.

There’s another angle to this, however. Data center growth may well happen faster, but PC sales aren’t suddenly going to show a spurt. In fact, several forecasts show that it is expected to undergo a slow decline through 2020.

With IoT requiring a lot more time to go mainstream, Intel’s precarious position is highlighted by the fine line it is walking between declines in PC-based sales and growth in the data center segment.

The stock has run up quite a bit in the last 12 months and is already trading near its 52-week high. At more than three times sales and nearly 16 times earnings Intel does not look cheap when you consider the headwinds the company is facing in the medium term.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.