Companies sometimes need a rude awakening to shake them out of their deep slumber. As they grow bigger, they tend to get more sluggish and reactive instead of nimble and proactive. Procter & Gamble (PG, Financial), one of the leading consumer brands that, at one point, had Warren Buffett (Trades, Portfolio) as a proud shareholder, is now floundering without a clear path to keep driving its sales growth.

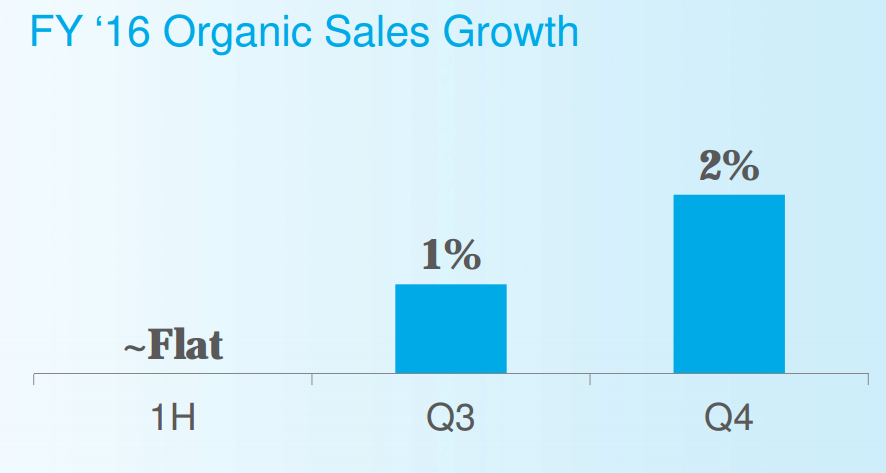

Revenue growth has been declining for the last four years, and the company decided to cut out the fat by selling off its low-margin brands and tightening its product portfolio with brands that have a higher potential for growth. But organic sales growth seems to have finally returned during the second half of the year, increasing by 2% during the fourth quarter.

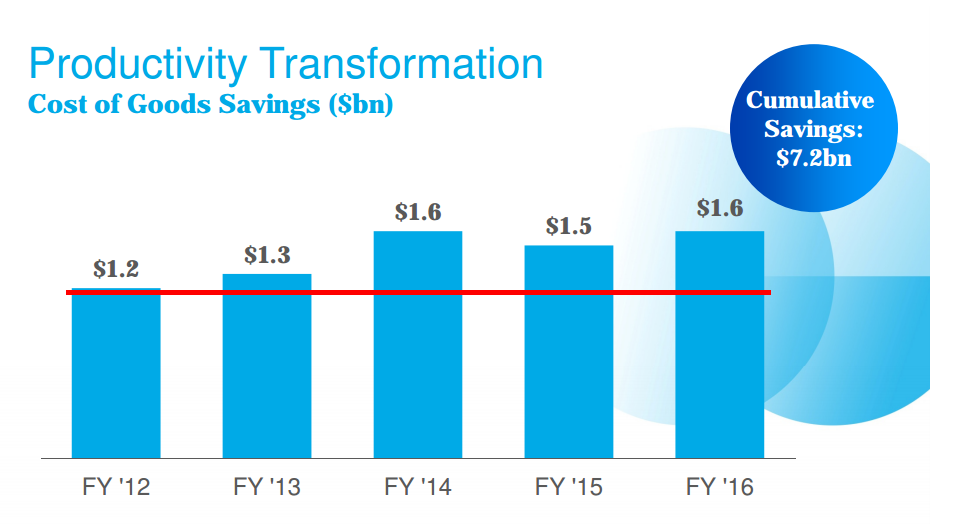

Procter & Gamble has also gotten more aggressive with its marketing budget, increasing its 2016 marketing spend as a percentage of net sales by 90 basis points. While the company increased its efforts to sell more goods, it also started cutting costs. According to the company, the cumulative savings from those efforts in the last five years have netted it $7.2 billion in savings.

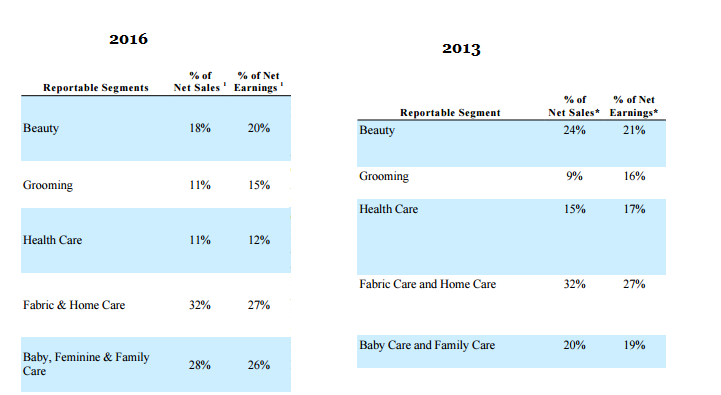

The transformation of the company’s product portfolio is stark when you compare the current segment distribution with 2013. Procter & Gamble’s Grooming and Healthcare segments now account for 22% of net sales, compared to 24% in 2013; the Beauty segment’s hold has also declined from 24% to 21%, while Fabric and Home Care’s contribution still remain the same. The Baby Care segment alone has expanded from 20% of net sales in 2013 to 28% in 2016.

“In 2012, the Company initiated a productivity and cost savings plan to reduce costs and better leverage scale in the areas of supply chain, research and development, marketing and overheads. The plan was designed to accelerate cost reductions by streamlining management decision making, manufacturing and other work processes to fund the Company's growth strategy.

As part of this plan, the Company expects to incur approximately $5.5 billion in before-tax restructuring costs over a six-year period (from fiscal 2012 through fiscal 2017). Through the end of fiscal 2016, 89% of the expected costs have been incurred.” - Procter & Gamble 2016 Annual report

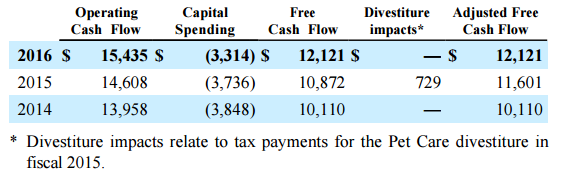

Clearly Procter & Gamble has been actively correcting its internal composition. It has reduced the number of products it sells, increased its advertising budget and reduced overall costs as well. This has had a huge impact in their operating margin, which has increased from 15.6% last year to 20.6% this year, while operating cash flow expanded from $14.6 billion to $15.43 billion.

The increase in operating cash flow should allow the company some room to breathe. As it is, many dividend investors were shocked at the 1.1% increase the company gave out earlier this year because Procter & Gamble increased dividends by 3% in 2015 and by 7% in 2014, 2013 and 2012.

It was a rude shock to many investors, as the company has been paying dividends for more than 125 years. But it also showed the company's changing circumstances.

A crucial part of their transformation is now over. Their cost reduction program is already 89% complete, and their ‘sell the unnecessary brands’ strategy is also more or less complete. The real challenge starts now, as they will have to show consistent organic sales. The initial signs are good but I will still remain cautious until I see some growth stability on the organic front.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.