I wrote an article two years ago titled “Oil and Gas: USA 1, OPEC 0.” I began that earlier article with these words:

“OPEC doesn't stand a chance.

Since most OPEC nations can pump all the oil and gas they need using first- or second-generation technology, they fail to [utilize fourth or fifth generation role technology to decrease their costs]. The point, when investing in energy companies, is not to ask merely, 'Is the price of oil up or down?' When investing, we are seeking firms that can grow their revenues and their earnings, thus increasing their intrinsic value through good times and bad. So the more important question to answer is ‘At what point can company A or country X make a reasonable return so that its earnings grow at whatever the current price of oil is?’

Answering that question for individual companies like those in America, Canada, Australia and much of Europe and the rest of the world involves determining the price the company receives for its efforts and beyond that, what its costs are to service its debt, pay its employees, upgrade equipment, etc. For these independent companies, once they have satisfied their creditors and employees, the rest is effectively divided among its shareholders via dividends, buybacks or an increasing stock price.

But for OPEC nations, which typically have just one state-owned monolith, the answer is very different. These behemoths exist to provide revenue for the massive welfare states the rulers of these nations have created. [They need more profit in order] to keep their grip on power… lavish largess upon their cronies, and provide food, fuel and other subsidies to their restive subjects in order to keep them in line.”

These state monopoly producers might be able to "pump" oil at a lower cost, but the price they need to stay in power far exceeds what independent oil and gas companies need to pay their bills and keep their shareholders happy. Thanks to OPEC, private companies have cut their cost of production by up to 50% since I wrote the original article two years ago. This is a tsunami that OPEC cannot hold back.

Nongovernmental producers of oil and gas, especially in the U.S. and Canada, have only to satisfy their shareholders, not the entire welfare state. (Except for ridiculously high taxes, of course, but that’s a subject for a different article.)

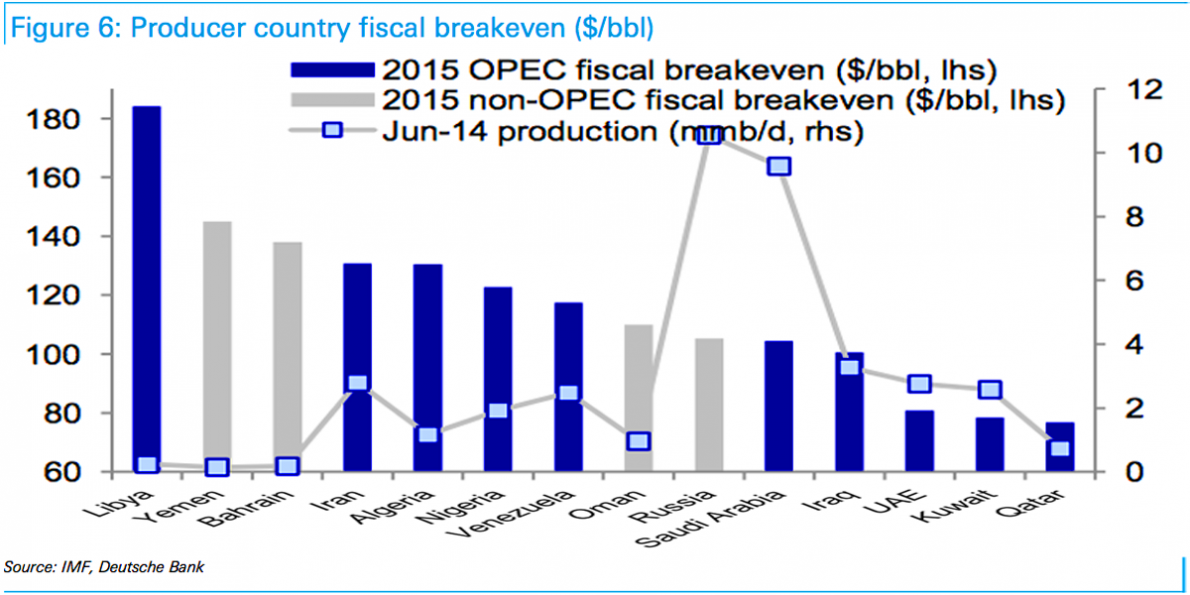

Here is what governments with state-owned monopolies need the price of oil to be in order to balance their budgets. Saudi Arabia may be able to extract oil for $7 a barrel, but it needs it to sell for roughly $100 a barrel in order to break even after paying off the royal family, the cronies, the bureaucrats and, via massive subsidies, a restive populace.

(click to enlarge)

OPEC is whistling past its own graveyard. Its level of naïveté dooms some, its arrogance the others. After the much-feted “agreement” of Nov. 30, it faces the possibility (likelihood) that almost all members will agree to one thing but will do another.

I liken this to the Prisoners’ Dilemma. It is a very real interrogation tool and famous in game theory whenever two or more perpetrators (or other actors like individuals, companies and nations) are placed in a situation where their courses of action are limited and their choices critical to their future.

In the traditional example of the Prisoners’ Dilemma, two suspects have been apprehended fleeing the scene of a heinous crime. They are immediately separated to prevent them from concocting a mutual story, are placed in separate holding cells, then in separate interrogation rooms. When interrogated, they each have a choice or dilemma: whether to confess, implicating the partner in crime, or claim innocence.

No matter what the partner is doing in the other room, each can improve their own chances of more favorable treatment by confessing — as long as they fear the “other guy” is going to confess as well. And even if Perp No. 2 keeps silent and fails to confess, then Perp No. 1 can obtain the better treatment accorded a state’s witness by confessing. It is this dilemma that helps explain why guilty prisoners often confess. Honor among thieves is a nice catch phrase, but it more often than not breaks down when hoisted upon the horns of this dilemma.

This dilemma is faced every day in economics, in business and especially in geopolitics. For instance, let’s say there are two countries selling the exact same product. We’ll call them Saudi Arabia and Russia. Each must decide on a pricing and production strategy. They best achieve their same goal of maximum national revenue when they both charge a high price. Their decision is complicated, however, because theirs is a business where supply and demand dominate pricing.

Lots of gas and oil sloshing around? The price will be lower. Too little available when and where needed? Buyers are willing to pay up. If Perp No. 1, let’s call it Russia, wants to sell its product to a country that is willing to collude with it by hiding the true amount purchased, let’s call it China, then Perp No. 1 will gain market share at the expense of Perp No. 2. In a commodity-type market, market share is critical. For simplicity, let’s say at price “x” both Russia and Saudi Arabia sell $15 billion per month of gas and oil. If one undercuts price “x” (under the table) by 10% it will lose a little revenue but it will increase its market share at the expense of the other that is still selling the agreed-upon amount of production. Since there is more supply now, the price will likely decline, harming all other gas and oil exporters.

Let’s say Russia decides to act in its own best interest and raise production above its allotment under the agreement because it can get it across the border into China and no one allegedly monitoring production can see it. By selling more gas and oil, even at a slightly lower price, Russia makes a much bigger contribution to its GNP and no one is the wiser. Of course, it doesn’t have to be Russia. It could also be Venezuela, Iraq or any other member. Iran has been cheating all along so, even with its uncapped-until-they-catch-up agreement, it might still cheat just to stay in practice.

In this example, by producing more but selling at a lower price, Russia wins business and increases its GNP at the expense of its rivals — er, teammates. This low-price/more (hidden) production strategy is akin to the prisoner’s confession, and the high-price/hewing to the agreement production level is like keeping silent. Call the former cheating and the latter cooperation.

Cheating is like a prisoner confessing; cheaters get the upper hand. The problem is even though its monitoring doesn’t detect Russian sales to China, Saudi Arabia notices that the known (not hidden) supply is still keeping a lid on prices and may even worsen, and it decides to cheat a little as well. When both cheat the result is worse than when everyone cooperates.

Compound this possible (likely?) outcome with cheating by more than just two members of the agreement. Add to that the uncapped production levels for Libya and Nigeria and the special accommodation for Iran. Who knows? Maybe China will became an exporter of oil itself and claim it came from Chinese production or, more likely, prop up North Korea with all the extra oil it doesn’t need for its strategic reserves. Now we have a prisoners’ dilemma on steroids.

Where does this leave OPEC members? OPEC members cheat. Russia cheats. They always have, and they always will. It is a cultural way of looking at the world that goes beyond the rationalism of understanding the prisoners’ dilemma and adds another solidifying element to it. Many cultures believe that win-wins are possible. Many others believe life is a zero sum game as in “For me to win, you must lose.”

Many OPEC nations and Russia will negotiate in bad faith, cheat on production, slip a few (million) barrels off to a known miscreant in whose interest it is not to divulge the source of its fuels and do whatever it takes to “win.” Signers of the agreement will likely cooperate more when their actions are more easily detected and less when actions are less easily detected, and industries with fewer competitors providing the product and strong barriers to entry are more likely to be collusive. (This is why free-market capitalism will always provide a more effective barrier to collusion and a better price for consumers than oligopolies, monopolies and socialist state-run enterprises.)

The problem with a “if you cheat, then I will cheat” strategy is that it is subject to misinterpretation. If Perp No. 2 only cheats if it righteously-indignantly believes Perp No. 1 cheated, but Perp No. 1 really didn’t cheat, then innocent actions misinterpreted as cheating increase the risk of setting off successive rounds of (unwarranted) retaliation.

OPEC has jumped the shark, and other sharks are now in the water. Saudi Arabia could once dominate both OPEC and world oil prices. Russia, Canada and the U.S. are now roughly equivalent peer competitors to the Saudis with many more nations like Norway and Australia rapidly closing the gap. Of course, there may be collateral benefits from this change. As the Saudis reflect on their changing role, maybe they will broaden their economy and reconsider their support and export of Wahabist/Salafist extremism.

Whether they do or not, the place to invest is in U.S. and Canadian shale oil and gas producers using horizontal fracturing and other modern techniques to extract product even from fields once declared dry. Just not right now.

OPEC members cheat. Russia cheats. They always have, and they always will. It is cultural as well as economic: “If I win, you must lose.” For this reason I see another decline in the price of oil and gas as supply mysteriously rises. Of course, we need to remember that since 2013, U.S. and other free-market producers have lowered their costs of production substantially, so much so that in many places, companies are actually profitable with oil at $50 a barrel. Heck, in the uber-prolific Permian Basin, costs are down as low as $35 a barrel.

Hello, fracking; goodbye, OPEC

If I’m not buying gas and oil now, what am I doing? There are six gas and oil investments I picked up prior to the OPEC and cronies talks: Chesapeake Energy (CHK, Financial), Southwestern Energy (SWN, Financial), Transocean (RIG, Financial), closed-end funds BlackRock Energy (BGR, Financial) and BlackRock Resources (BCX), of which the top positions are gas and oil, and ETF PowerShares Energy (PXI, Financial).

I have placed tight trailing stops on all of them (ranging from 4% to 8%). I also have some buy orders at significantly lower prices placed with our custodian brokerage firms. These include limit GTC buy orders on 300 ExxonMobil (XOM, Financial) at $77; 300 Total (TOT, Financial) at $41; 250 Chevron (CVX, Financial) at $88; 300 Royal Dutch Shell (RDS.B) at $41; 500 Suncor (SU, Financial) at $25.50; 500 Imperial Oil (IMO, Financial) at $28.50; 500 Canadian Natural Resources (CNQ, Financial) at $25; 200 Anadarko Petroleum (APC) at $47; 350 Devon Energy (DVN, Financial) at $32; 1,000 Encana (ECA, Financial) at $8.50 and 400 Range Resources (RRC) at $28. We will also look to buy back 1,000 Southwestern Energy at $9.40 or below and 1,500 Chesapeake Energy at $5.75 or less.

It may seem surprising that we’d sell these last two and buy them back after enjoying only a 40% profit. They’ve been very good to us in a very short time, but I believe our clients would do better to take their profits from these and buy a particular subset of actively managed mutual funds, which we’ve been doing for a week now. Why actively managed funds when most financial advisers advocate passive ETFs? That’s a whole ‘nother subject – which I promise to discuss this weekend.

Start a free seven-day trial of Premium Membership to GuruFocus.