In a surprising turn, value investor Charles Bobrinskoy does not like banks anymore, just as they are tearing it up on the market. The main reason: book to market values are running up like crazy. He does not believe regulatory changes are going to improve the environment enough to justify valuations. Mid-cap banks are trading at 2.2 times book value. There are individual names that are still underpriced, but the category as a whole is not. The bank business is just not as great as it was in the glory days.

One financial he still likes, a non-bank, is KKR & Co. LLP (KKR, Financial), which he believes is unpopular because of its partnership structure and concerns over carried interest.

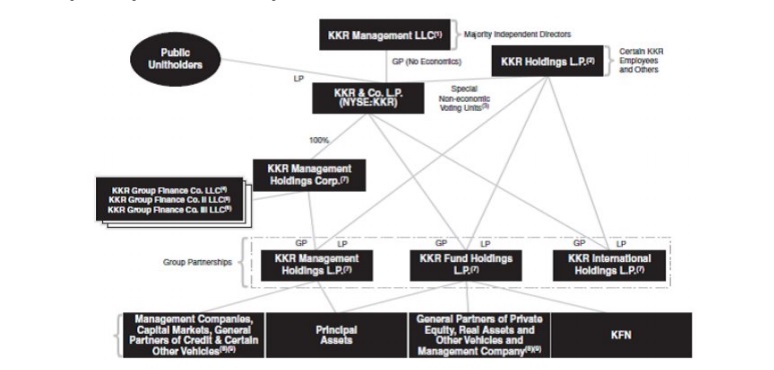

Its structure is really kind of complicated:

And to take Scott. C. Nutall's, the head of Global Capital and Asset Management, comments on the latest earnings call a little bit out of context:

"The market really likes simplicity, and we largely get paid to assess and understand and invest in complexity, and we're finding complexity is pretty cheap right now."

Basically, there are two important ways KKR makes money:

- By investing its own money and generating returns.

- By charging management and performance fees to its limited partners.

This means its assets under management is an important number and so is its book value (which is not included in AUM but represents capital it can invest for its own book and on behalf of KKR’s unit owners).

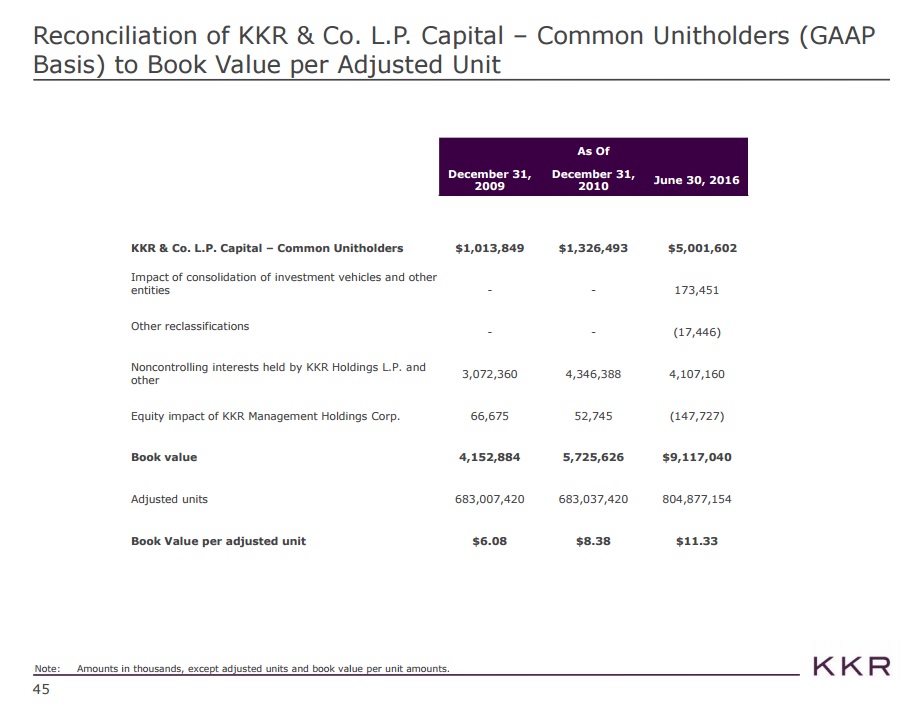

Here is KKR’s overview of book value per adjusted unit:

Note we find almost $11.95 in value here while the share price is only $16.62. The market ascribes only $4.67 of value to KKR’s business of attracting outside capital and generating fees on it. This is remarkable because most of the capital it has contracted is locked up for up to 10 years.

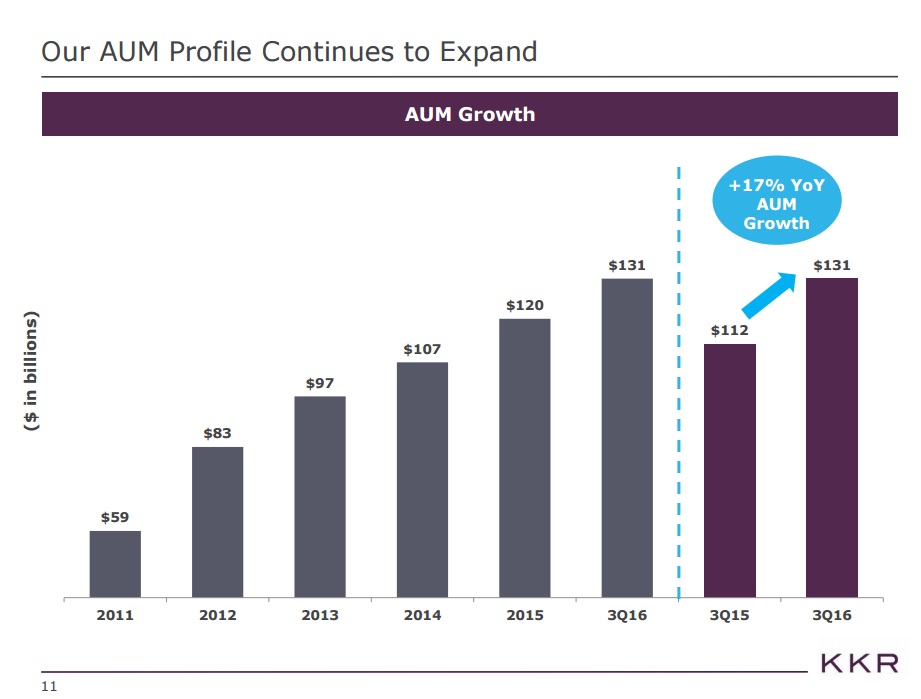

The firm has $130 billion of assets under management. You can value asset managers on AUM, as I wrote in my earlier write-up of Fortress Investments (FIG, Financial):

"...typically they are worth somewhere between 2% and 8% of AUM with the mean lying closer to the bottom of that range. In general fixed income and institutional investments are worth less and PE, hedge-funds, retail, equity and special investments are worth more. Think higher fees (incentive fees, etc.) = more valuable and hard to withdraw = also more valuable. Even if you would value the firm at just 2% in the very bottom of the range, it is worth $1.4 billion, which is roughly 40% higher than its market cap."

There is a big difference between the value of the AUM of Vanguard (VTI, Financial) or Blackrock (BLK, Financial) compared with that of KKR:

- KKR charges a blended fee of 1.2% on its AUM

- 100% of capital is locked up for 8 years

- All AUM is subject to performance fees

One can make a good case it should be valued on the higher end of assets under management ranges, but even if it was valued at just 2% of AUM, it should be worth $26 billion or $5.8 per unit. Even that low-ball valuation exceeds the markets assessment of $4.67 by 24%. If valued at 4% of AUM, the value should go up 150% to close the gap. And that is still only half of what the range for asset management firms can go up to.

The almost $12 in investments and cash on the balance sheet is not undervalued much, but one could argue it is a good deal as well. KKR uses this money to plow into its investments along with its limited partners. Its limited partners liked KKR’s investment results so much that they handed over $130 billion to manage. However, the cash utilized by KKR itself is subjected to much lower fees, giving you access to its strategies through a much better proposition. The downside is you do not get your capital locked up, which means you will still have to exert the discipline of holding through market vagaries yourself. The blessing and curse of the value investor.

Disclosure: Author is long KKR and FIG.

Start a free 7-day trial of Premium Membership to GuruFocus.