Google bought YouTube in 2006 for $1.65 billion when YouTube had 72.1 million users across the globe. It is possibly one of the best acquisitions Google, now a subsidiary of Alphabet (GOOG, Financial)(GOOGL, Financial), has ever made because the user base alone has exploded to more than 1 billion users watching hundreds of millions of hours of video.

With nearly one in every three people with access to the Internet already on YouTube, the video giant has achieved the massive scale required to make it practically competitor-proof. Facebook (FB, Financial) has been aggressively pushing its video platform, but despite the size of its user base it is still way behind the curve when it comes YouTube’s video consumption rate.

The growth of smartphones and mobile devices around the world, the increasing penetration of the Internet and the ever-increasing Internet speeds have led to accelerated video consumption around the world. It has now become easier than ever to stream videos online, and the resulting growth has been staggering.

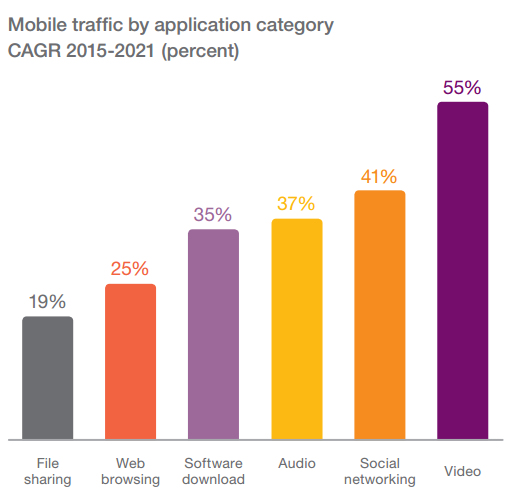

According to Cisco (CSCO, Financial), online video traffic will increase fourfold between 2015 and 2020, a CAGR of 33%. Ericsson (ERIC, Financial) predicts a similar growth pattern as well and expects mobile video traffic to account for two-thirds of all mobile traffic by 2021.

“Mobile video traffic is forecast to grow by around 55% annually through 2021 when it should account for over two-thirds of all mobile data traffic. While social networking is forecast to grow by 41% annually over the coming six years, its relative share of traffic will decline from 15% in 2015 to around 10% in 2021 as a result of the stronger growth in the video category. The rest of the application categories have annual growth rates ranging from 19% to 37% so are shrinking in proportion to the whole. The trend is accentuated by the growing use of embedded video in social media and Web pages, which is considered video traffic in this context.” – Ericsson Mobility Report

To take just one instance, the massive growth of Netflix (NFLX, Financial) over the last five years is a huge validation for streaming-video-on-demand (SVOD) content. The market has matured to a stage where it is ready to pay for video content delivered over the Internet. While Netflix remains the king of paid video content, YouTube still remains the king of public, user-generated video content – something that no company has been able to disrupt.

From the production side of things, as the largest public video platform YouTube is still the most attractive destination for content creators because that’s where the bulk of its audience is. It’s reached a point where it is now a self-feeding cycle of production and consumption.

And that creates a moat that is uncrossable for all practical purposes.

With video consumption projected to grow at an extremely fast pace over the next several years, video advertising will follow suit, increasing YouTube's revenues. Every company wants to get a slice of that growth, but with 1 billion users on its video platform, YouTube will stay ahead of everybody else.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.