With fourth-quarter earnings around the corner, JPMorgan Chase & Co. has upped the expectations on streaming video-on-demand (SVOD) service leader Netflix (NFLX, Financial) by reiterating its “overweight” status for the company. JPMorgan expects Netflix's global profitability to increase due to stronger content.

Netflix will be reporting its fourth quarter earnings on Jan. 18. The stock’s performance will be tied directly to the number of subscribers the company added during the quarter and the forecast for subsequent quarters. When a company is trading at 6.8 times sales, even a small shock to sentiments could drive the stock significantly lower or send it skyrocketing upward. Companies trading with high valuation multiples, such as Netflix, tend to be highly volatile around earnings time, and that is something investors should use to their advantage, either to add to their position or to offload stock.

"We believe Netflix is on track toward significantly disrupting the linear TV market through strong subscriber growth, content differentiation and a better consumer proposition," JPMorgan analyst Doug Anmuth wrote in a note, as reported by CNBC. "We believe NFLX sets up as a cleaner story into 2017 with pricing changes behind, revenue accretion from higher ASPs [average selling prices], stronger content and increased global profitability."

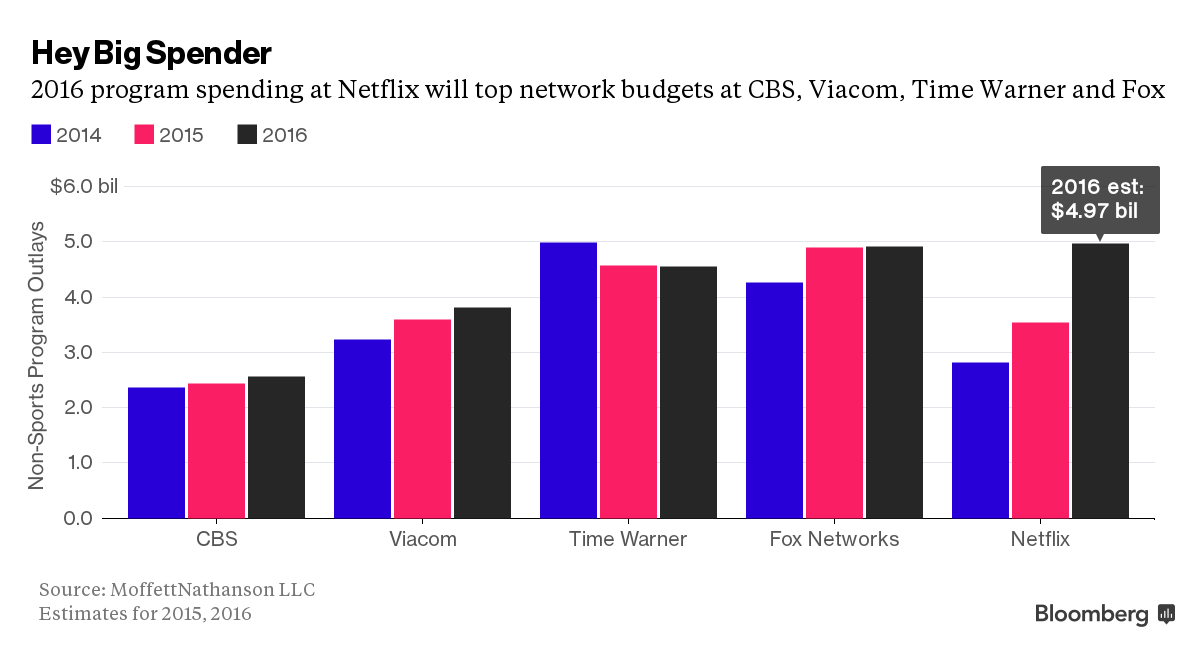

There are several underlying factors that could make JPMorgan’s expectations for Netflix come true. As U.S. subscription growth started slowing down due to high levels of penetration and increasing competition in the market, Netflix expanded rapidly into 190 countries. As the company added country after country to its operational list, Netflix also made a major announcement last year that it will be investing $6 billion towards original programming in 2017, making it one of biggest spenders in the category.

To put that number in perspective, Netflix’s planned expense for 2017 is nearly a billion dollars more than what Time Warner (TWC, Financial) spent in 2016 and it will be higher than what NBC and CBS are expected to spend in 2017.

In the process of expanding its original programming content, Netflix has been steadily trimming down its licensed content. The company expects that differentiation would be a better position to take in an overcrowded market.

Netflix is the only video streaming company with more than $2 billion in quarterly revenues. As a niche player, Netflix can afford to plough all of its cash flow into its content programming initiatives, making its competitors’ product lineup look extremely weak in comparison. Amazon (AMZN, Financial) and YouTube Red will find it extremely hard to match Netflix’s aggressive posturing in their own original programming plans as it is only part of their business, whereas that is the only thing Netflix does.

It is this collusion of factors that will keep Netflix growing from strength to strength until they reach comparable saturation levels in all the major markets they are now present in. And with internet penetration still climbing in newer markets, it could take years before that happens.

Disclosure: I have no position in the stocks mentioned above and have no intention of initiating a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.