My view that the world is becoming more complicated has made me revisit value investing’s core principle. This is me thinking out loud and not an attempt to convince anyone of any particular view. To start, here are beliefs that anchor my thinking:

- We all have limited ability to input, retain, process and output information.

- What we know compared to what is knowable is infinitesimal. We all know less than we assume we do. With how much of the knowledge on Wikipedia is any one person familiar? Wikipedia represents a sliver of what humanity thinks it knows.

- Our knowledge is incomplete and how much of it is wrong is uncertain.

- All individuals operate under false assumptions. We’re wrong about a bunch of stuff, we have no idea what we’re wrong about or the extent of our misinformation, and we don’t know what we don’t know.

- As somebody operating under incomplete and false assumptions, I reserve the right to change my mind at any time.

I have heard hiring managers seeking to fill international positions for a specific country say that they would prefer MBA students who’ve never visited the country over ones that have. That’s because job candidates who have had brief exposure to the foreign country assume expertise they do not possess. Imagine if someone visited Manhattan and assumed that’s what the entire country was like. They would have a very skewed view of the U.S. Similarly, all individuals have skewed views of reality because of our limited powers of comprehension.

Pardon the dreary rambling, but these beliefs make me question value investing’s central principle: buy stocks with a margin of safety relative to its intrinsic value. One of the most common methods to derive intrinsic value is to use Discounted Cash Flow (DCF) analysis. I’ll scope this article to just this valuation method. In layman’s terms, the DCF method is discounting a company’s future cash flow stream to its present value. The equation for DCF is shown in the picture below.

CF stands for cash flow and r (discount rate) equals WACC which stands for the weighted average cost of capital. It is comprised of debt and equity. You can use this link to see a more in-depth explanation of WACC and an example of how GuruFocus calculates Apple’s (AAPL, Financial) WACC. CF and r are based on projections of the future; DCF is theoretical and subjective. As a result, intrinsic value derived by DCF is also theoretical and subjective.

Thought experiment 1

How would you use perfect information?

Let’s say you were a genetically modified superhero with an alter ego named Larry with a really big, blue, bald head, and your power was omniscience, would you be a speculator or a value investor? I will define speculation as trading of price movements and being indifferent to business fundamentals. A value investor is someone who buys below intrinsic value.

If you were omniscient, how big of a pain in Larry’s rear end would it be to calculate intrinsic value? CF and r constantly change. GuruFocus uses annual earnings for its CF when it calculates DCF. But if you were omniscient, how often would you discount a CF variable to get a true value? The more precise, the more accurate. Would you use earnings per month? Earnings per minute? Earnings per second? Or would you use earnings at the time of every sale? You would have to burden every sale with every expense and then how would you adjust the variable n to account for the irregular frequency of sales? Also, would you use GAAP (generally accepted accounting principles) to calculate the CF inputs? If so, one must not forget that GAAP changes and the CF inputs must change to reflect that along with everything else that affects earnings. What rate would you use to discount each CF input? For the cost of equity in WACC, would you calculate the exact risk-free rate, the risk premium and the beta at the time of sale? I don’t have a good answer.

Irrespective of how one chooses to calculate DCF, I would simply argue that it would make much more sense to be a speculator if you were omniscient. There would be no need to wait for stocks to revert toward their intrinsic value. Omniscience would allow you to know every buyer and seller’s intention. You would profit handsomely by buying every stock at its daily low and selling at its daily high. In actuality, you would probably buy as frequently as possible when prices ticked down and sell when prices ticked up. The point is that one, intrinsic value is subjective, and two, speculation theoretically beats value investing.

Note: The high frequency trading strategy known as front running as practiced in the Michael Lewis book “Flash Boys” was not theoretical. HF traders electronically extrapolated other market participants’ intentions and profited. Traders bragged that they had a five-year stretch of not losing money on any single day. They were able to behave like Larry the speculator.

That’s Larry taking a break from trading.

Thought experiment 2

How do analysts calculate DCF for Apple?

They need to make earnings projections that start with sales projections. To simplify, let’s assume that Apple’s earnings are 100% derived from iPhone sales. Apple shipped ~212 million units last fiscal year for revenue of ~$137 billion. When people make an intrinsic value calculation for Apple based on DCF, they’re playing with some very big numbers. If an analyst projects an 8% increase in unit sales, that’s potentially 231 million individuals buying an iPhone in over 130 countries. Let’s think in terms of running a business so let’s think of the actual unique people that Apple needs to convince to buy an iPhone. Every individual represents a range of potential outcomes. Can you imagine the 231 million scenarios in 130 countries in which the buying decision would need to be made in order to fulfill the 8% growth projection? Probably not. We’re human.

How precise are analyst projections? With how many currencies do they have to deal? We’re just talking about the revenue side and only for one year. Plus, we’ve simplified this example to just include iPhones, ignoring Apple’s other businesses. On the expense side, an analyst must make projections about how suppliers and employees will behave, not to mention other stakeholders like regulators.

Thought experiment 2 is a long-winded way of saying calculating Apple’s intrinsic value amounts to guessing. Implicit in the guess are assumptions of the behavior of millions of customers in addition to suppliers and Apple employees. No practical amount of surveying or channel checking can yield precise earnings forecasts. We just had a presidential election where one of two people could win, and most “experts” still guessed wrong.

The image depicts a stadium with ~100,000 people. If an analyst projected 231 million iPhone units to be sold next year, that would be ~2,310 of these stadiums filled with individuals from over 130 countries. How reasonable is it to expect an analyst to accurately project sales five years from now?

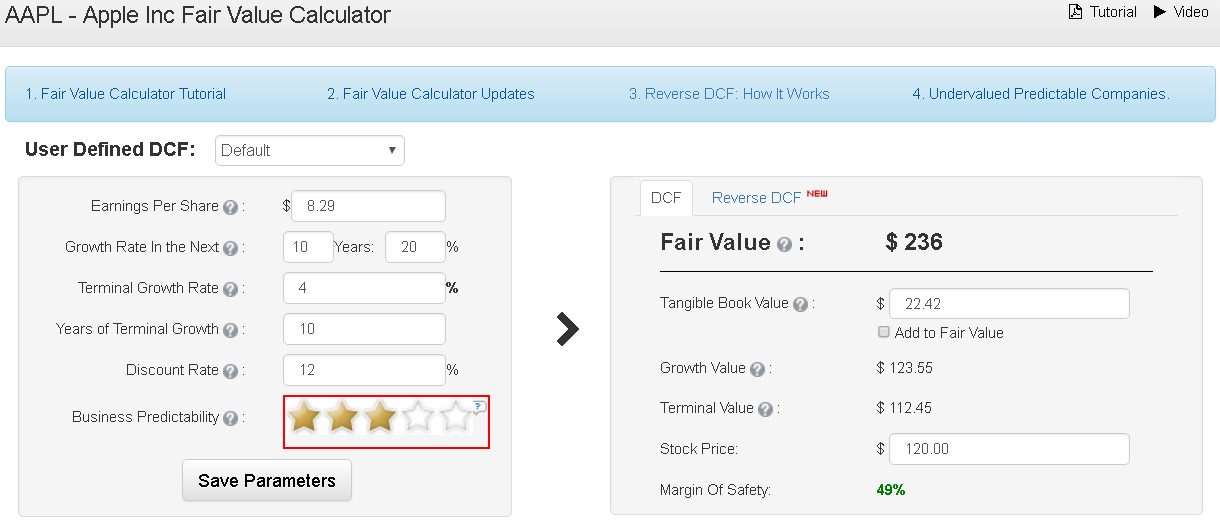

To illustrate how sensitive a DCF calculation can be, I’ve used GuruFocus’ DCF calculator for Apple with its default parameters of $8.29 EPS, growth rate of 20% for 10 years, terminal growth rate of 4% for 10 years and a discount rate of 12% that yields a DCF value of $236 per share.

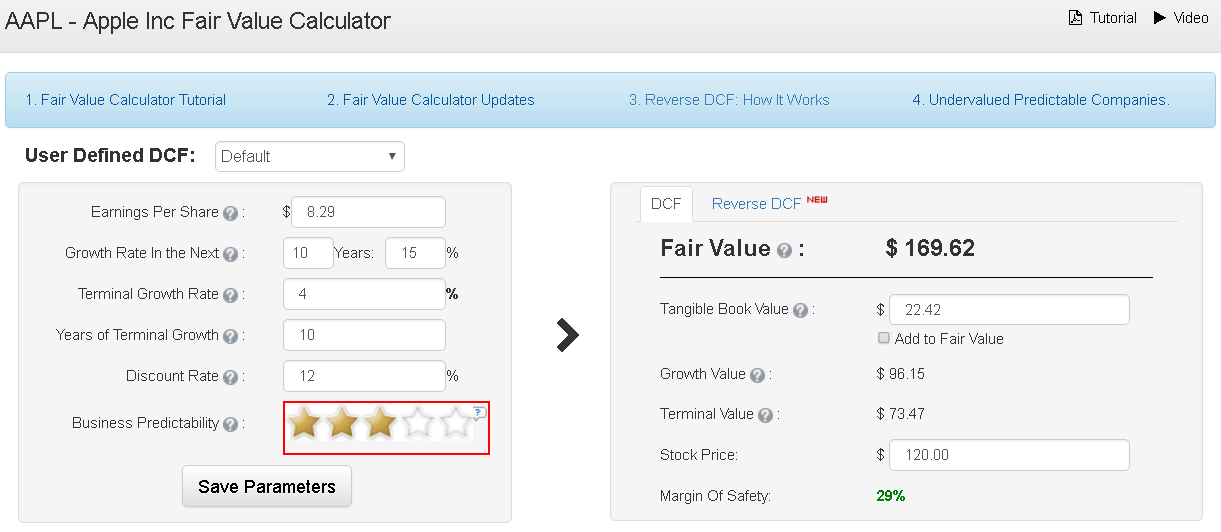

If the only variable I change is growth rate from 20% to15%, then the DCF value drops to $169.62, a decline of 28%. It shows how sensitive intrinsic value is to a person’s assumptions; 20% or 15% growth over the next 10 years for Apple would be wildly optimistic. What if, for the sake of conservatism, I calculated Apple’s DCF with a negative growth rate? If I project Apple’s growth rate over the next five years as -1% and assumed a terminal rate of 0 and discounted at 12%, DCF would equal $54.34.

On the other hand, average daily trading volume for Apple stock is about 29 million shares. How many actual individuals trade Apple shares each year? Tens of thousands? Hundreds of thousands? Millions? Fewer people trade Apple shares than buy iPhones. Speculators guess Apple’s stock price movements. They make assumptions about the buying and selling behavior of Apple shareholders. Which guessing game is more speculative – guessing the behavior of Apple customers/suppliers/employees or guessing the behavior of stock market participants who trade Apple shares? Where are the odds worse? Guessing Apple’s intrinsic value three years from now or guessing Apple’s stock price three years from now?

If you believe that everyone who sells and buys Apple stock is doing so based on intrinsic value calculations, then it’s a “chicken and egg” type question. If not all stock traders use intrinsic value calculations for their pricing decisions, then it’s reasonable to ask, how do people decide what price to pay for Apple stock?

I have contributor Alex Barrow’s article to thank for bringing my attention to a Stanley Druckenmiller (Trades, Portfolio) quote. Druckenmiller is an all-time great investor. According to Barrow, “Druckenmiller never had a single down year [over 30 years] and only had five losing quarters out of 120 altogether.” Here’s the quote:

When I first started out, I did very thorough papers covering every aspect of a stock or industry. Before I could make the presentation to the stock selection committee, I first had to submit the paper to the research director. I particularly remember the time I gave him my paper on the banking industry. I felt very proud of my work. However, he read through it and said, "This is useless. What makes the stock go up and down?" That comment acted as a spur.

Thereafter, I focused my analysis on seeking to identify the factors that were strongly correlated to a stock's price movement as opposed to looking at all the fundamentals. Frankly, even today, many analysts still don't know what makes their particular stocks go up and down.

The part about not understanding what makes a stock’s price go up or down smacked me in the face when I first read it. That’s not something that I had put much emphasis on. I was fixated on guessing intrinsic value which made me forget how money is made in the stock market -selling to buyers who pay above my purchase price. Value investors buy below intrinsic value and believe that someone will eventually agree with their view of the world. I interpret Druckenmiller’s quote as saying be aware of how other market participants view the world and incorporate that into your strategy. As an example, it’s my observation that many stocks are expensive relative to their intrinsic value because some people fixate on dividends. It’s the size and movement of the dividend payment that greatly influences whether those stocks move up or down. I recommend reading Barrow’s article if you want to learn more about Druckenmiller or reading this book.

What made me question value investing is the belief that the world is becoming more unpredictable. A growing population means more potential outcomes. Compound that with the accelerating pace of change where information is being dispersed faster, consumers being presented with more products and services faster, competition reacting faster, capital being raised faster, etc. Uber is a prime example of how quickly things can change. Ben Graham is often quoted as saying, “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” In an increasingly unpredictable world, what’s more difficult to handicap – the voting machine or the weighing machine?

People are still waiting for Netflix to generate consistent earnings growth. My observation is that Netflix (NFLX, Financial) analysts fixate on subscriber count. How long before the voting machine becomes the weighing machine? As John Maynard Keynes astutely observed, “The market can stay irrational longer than you can stay solvent.”

Many people like to use baseball as an analogy for investing. These thought experiments were done with the intent of refining my swing. In particular, my aim is to reduce risk. The situation I want to avoid is buying a stock at a price where there is a perceived margin of safety but then having the stock fall substantially lower as you sit on a loss. Some people consider this a paper loss. I disagree. The world is random and complicated. There’s no guarantee a stock will revert to an estimated intrinsic value or that your original thesis was correct. If this situation happens, then I accept it as the cost of investing, but that doesn’t mean I have to like it or that I can’t try to avoid it.

Let’s say you are interested in a stock with short-term problems where if the company keeps the dividend the same, the stock will stay flat, but if it is cut the stock could immediately fall by 15%. The short-term risk/reward of buying this stock is skewed toward waiting until after the dividend payment announcement is made. Asking “what makes the stock go up and down?” is something I’ll ask to look for better entry and exit points.

Note: After I wrote this, I re-read Howard Marks (Trades, Portfolio)’ book, “The Most Important Thing: Uncommon Sense for the Thoughtful Investor." Here are some relevant quotes.

- For self-protection you must invest the time and energy to understand market psychology.

- Try to have psychology and technicals on your side as well.

- Trying to buy below value isn’t infallible, but it’s the best chance we have.

Disclosure: No positions.

Start a free seven-day trial of Premium Membership to GuruFocus.