Salesforce (CRM, Financial) has been clocking double-digit growth rates for the past several years. The side effect of such growth is that its price multiples have always been way over the top. The stock price has gone up by nearly 28% in the last 12 months and is now trading around seven times sales. The company never cared about operating income as it has always prioritized chasing top line numbers.

The enterprise software segment is inherently a high margin business. A quick look at Microsoft’s (MSFT, Financial) Productivity and Business Processes segment will show you the high double-digit margin nature of the business. IBM (IBM, Financial) wanted to move away from its legacy business lines into the software segment because of its high margin nature. But why, then, has Salesforce barely registered a profit in the last 10 years, and how does the company continue to get away with it?

The biggest reason is that Salesforce spends a lot of money toward marketing. In the first nine months of the current fiscal, Salesforce’s revenues were $6.09 billion while its marketing and sales expenses were $2.83 billion, accounting for nearly 46.47%. That means, for every dollar of revenue, Salesforce has spent nearly 50 cents toward customer acquisition. Unsustainable as it may seem, Salesforce has been growing this way for a long time and continues to do so.

Â

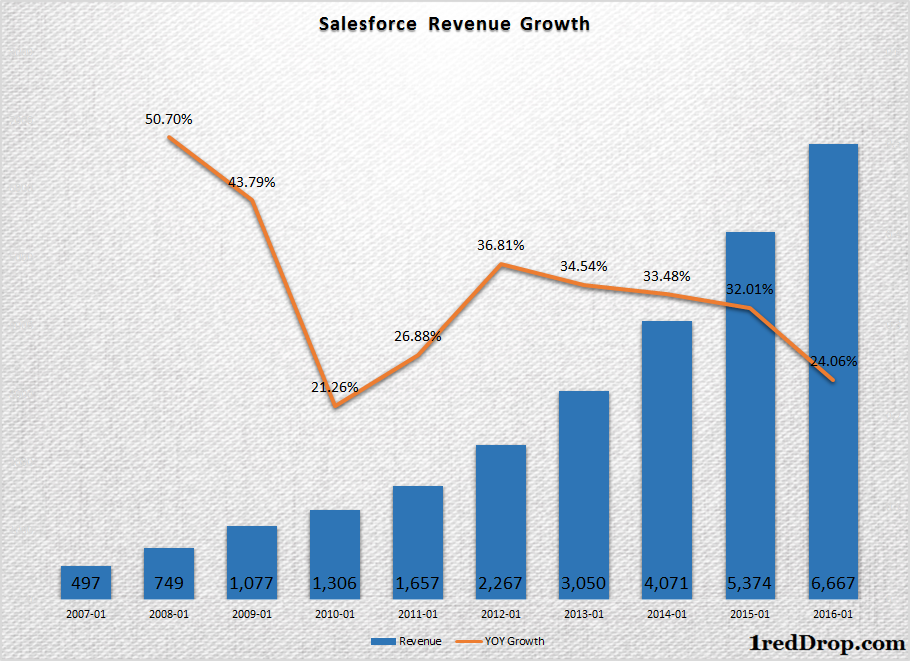

Revenue has now grown more than tenfold in the last 10 years. Though the growth rate has been slowly edging lower in the last five years – as the company gets bigger and bigger – Salesforce saw its revenues increase by 25.52% in the first three quarters of the current fiscal year. Growth rate has come down compared to its past performance but is still strong.

What has this accomplished for Salesforce?

Â

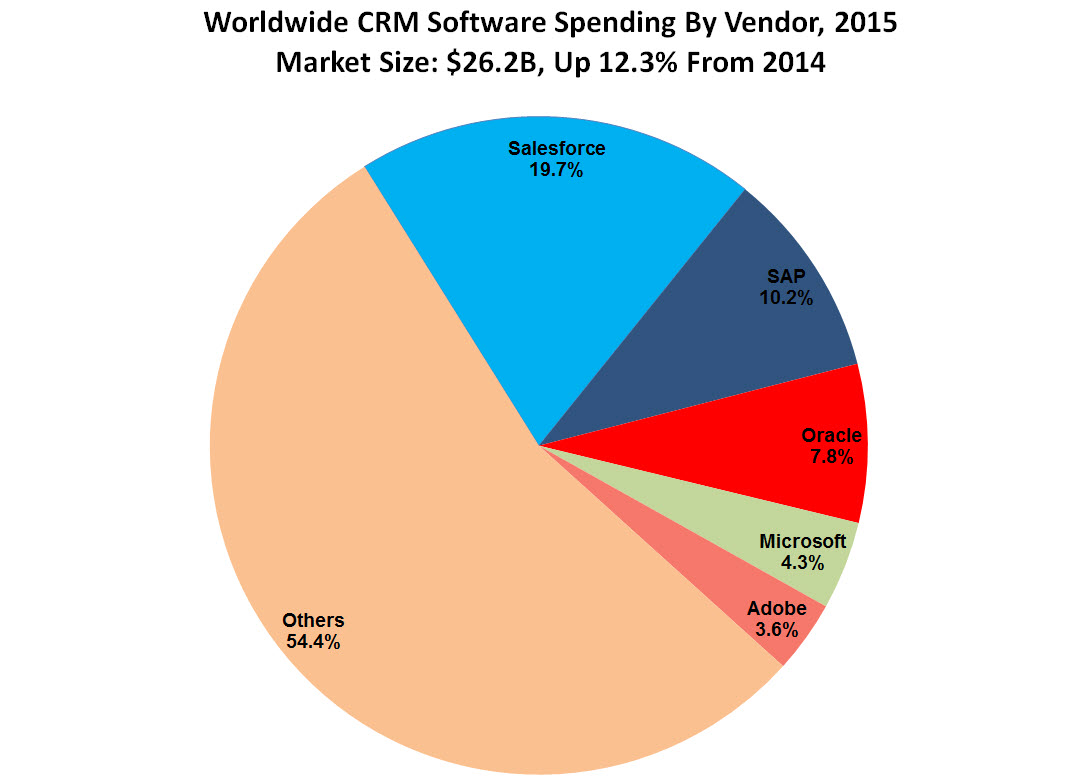

Salesforce is the market leader in Customer Relationship Management software holding nearly 20% of the market. According to current estimates, the CRM segment is expected to keep expanding at double-digit rates in 2017. The growth of cloud has significantly improved market awareness about SaaS products, and nearly all the tech majors have jumped on the SaaS delivery model.

The enterprise management software segment in particular has become extremely competitive, with Microsoft, Oracle (ORCL, Financial), SAP (SAP, Financial) and Salesforce fighting for space. One of the key reasons for Salesforce’s strong growth in the past was that the company took the SaaS/cloud delivery route for its products while the big tech majors sat on their annual licensing models. Those days are now gradually coming to a close, and SaaS is now the preferred software sales model.

With Microsoft and Oracle increasing their focus on the enterprise software segment, customer acquisition is going to get harder and harder moving forward. Salesforce is aware of the underlying market shift, which could explain why the company has been on a buying spree, spending billions of dollars in acquisitions.

Its leadership position in the CRM niche will give it a lot of room to add more layers to its service, and the Demandware acquisition for $2.8 billion provides it a foot in the door of the ecommerce industry.

The problem with Salesforce is not its ability to execute or bring in the top line numbers but the multiple at which the company is trading. At seven times sales, Salesforce has to keep up its double-digit growth rate, which is not going to be easy as its top line gets bigger and bigger while its competition also gets stronger and stronger.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.