Facebook’s (FB, Financial) valuation has always been way over the top, but there are several underlying factors that are driving the price multiples toward the sky.

Revenue growth has been staggering as the social media giant keeps posting record-breaking quarterly results. In 2016, Facebook’s revenue reached $26.88 billion from $17.07 billion per year before –Â growth of 57%. Despite reaching tens of billions in revenue, Facebook is still doubling its revenue every few years.

The growth of digital advertising and the current forecasts for double-digit growth over the next few years means Facebook advertising revenue will keep expanding. The other important factor is Facebook’s user base expansion all over the world. Facebook’s main platform continues to add millions of users to its rolls every year. The social network closed 2016 with 1.86 billion users, representing growth of 17%.

Instagram is one more growth lever that Facebook has under its fold, and the billion-dollar acquisition Facebook made looks all set to deliver the booster shot for the company’s user base expansion, further extending the already long userbase runway Facebook had.

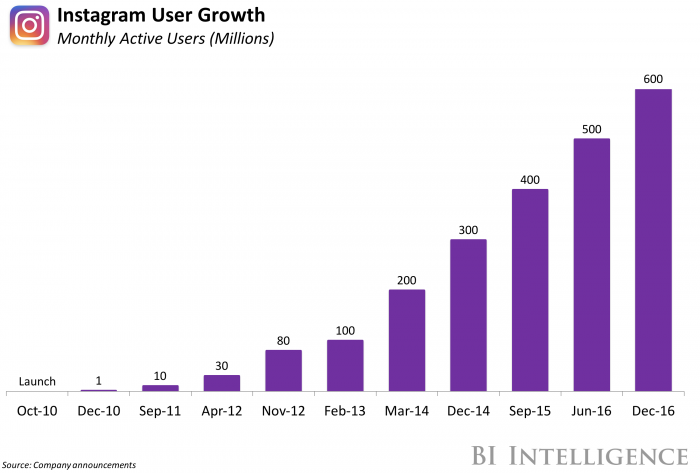

In a short span of seven years, Instagram has moved from zero to 600 million users.

As Facebook’s penetration around the world keeps increasing, its growth rate will slowly come down. Facebook has been able to compensate for the slow growth in developed markets with more users from Asia Pacific and Rest of the World regions.

Now, the stunning growth of Instagram, which looks all set to get over the crucial billion-plus user base mark over the next few years, will make sure that Facebook’s advertising revenue can continue its double-digit growth for a few more years.

Facebook has not one but two different applications that are monetizable. There will be several users who will be using both applications, but from an advertiser's point of view, that will still be considered as two applications to reach the potential user base. To put it simply, one person with a Facebook account and an Instagram account is still considered two users as far as the advertiser is concerned.

Facebook did the smart thing by not folding Instagram into its own platform, allowing it to stand on its own feet instead. This not only increases the number of users but also increases the amount of time the user spends on Facebook’s assets. The more time users spend on these applications, the more ads that can be shown per user, which Facebook refers to as "ad load."

WhatsApp is another application that already has a solid user base, but Facebook is yet to start monetizing the application. No one knows how long Facebook is going to take before that happens, but the growth of WeChat, China-based Tencent’s (HKSE:00700, Financial) messenger application, is a perfect example that billions of dollars in revenue are waiting to be captured by WhatsApp.

With all three applications, Facebook, Instagram and WhatsApp look set to bring in more users as well as more revenues, which is why it’s not really a surprise that the stock keeps trading near the 14 times sales mark.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.

Â