IBM’s (IBM, Financial) transition has been painful to watch with revenues declining year after year as the company slowly increased the contribution from the high margin Software as a Service segment.

Revenues from IBM’s strategic imperatives, which include cloud, analytics, cognitive, mobile and security, increased by $8 billion in the last two years. But the growth was nowhere near what IBM was losing on other segments and, as a result, revenues have continued to edge lower and lower.

Total revenues declined by 2% in 2016 despite the strategic imperatives segment posting a healthy growth of 13% and cloud revenues surging by 35%. Clearly, IBM’s losing revenue streams are bigger than IBM’s growing revenue streams.

Strategic imperatives brought in $32.8 billion in 2016, 41% of its overall revenues of $79.9 billion in 2016. Though the rate of the revenue slide came down last year, sustainable revenue growth is only possible once strategic imperatives account for at least half of overall revenues.

IBM’s cloud-delivered products are key to that transition, and this segment brought in nearly $13.7 billion in 2016, posting growth of 35% during fiscal 2016. IBM has managed to keep pace with Amazon (AMZN, Financial) and Microsoft (MSFT, Financial), both of whom have crossed the $14 billion annual run rate from cloud revenues.

The good news for all three companies is that cloud is still in the early stages of growth. In 2016, the Infrastructure as a Service market was estimated to be worth only $21 billion or so while global IT spending runs in the order of trillions of dollars.

The Iaas+SaaS market is expected to keep growing at double-digit rates for the next several years, and the leading vendors of the segment will capture most of that growth.

Though all three companies – IBM, Microsoft and Amazon – operate in the same cloud segment, their offerings are extremely different from each other’s. While Amazon has remained laser-focused on the IaaS segment, Microsoft has built a solid office collaboration suite of SaaS products along with Azure, its IaaS offering, and is more of a horizontal player in the cloud market. And IBM has kept its focus on large enterprises looking for hybrid cloud and managed cloud services.

Considering the future growth of cloud, there is plenty of room for all the players to grow, and IBM has become extremely strong in the analytics segment with Watson in the background. The analytics segment alone brought in $19.5 billion in revenues in 2016 and is the largest of its kind in the segment. Cloud and analytics will eventually propel IBM’s strategic imperatives’ revenues to account for more than half of the company’s revenues, but it will take a year or two to hit that level. Once that happens, however, revenue will shift to positive growth. Even if that pace is slow, it will be a huge validation for CEO Ginni Rometty.

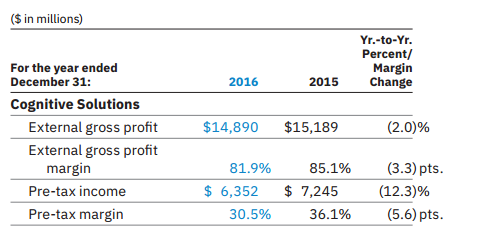

We still don’t exactly know the impact of cloud on IBM’s operating margins as it is mixed with several financial reporting segments, but the SaaS and IaaS segments are inherently high-margin businesses. IBM’s Cognitive Solutions segment, which includes analytics solutions, Watson and cloud data services, along with talent management solutions, security platforms and on-premise transaction processing software, had $14.89 billion in revenues in 2016 with a pretax margin of 30.5%.

As these forward-looking business lines grow, they will not only allow revenue to grow in the future but also will increase operating margins in the process. IBM is now trading at 12.6 times earnings, and it’s likely that the low valuation will continue until IBM reports flat revenue growth. Bu when IBM hits that point, the price-earnings (P/E) ratio will have gone up quite a bit. Considering the dividend yield of more than 3%, IBM is an extremely attractive investment at the current price point.

Disclosure: I have no positions in the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free seven-day trial of Premium Membership to GuruFocus.