Attempting to predict the outcome of an election is a fool’s errand — we do not bother with it.

But that does not mean we cannot make money off the vote.

Over the last few weeks, we have discussed the reasons for the rise of populism and how it has impacted the false trend in European equities. We explained how these Soros-style false moves are dependent on narrative “tests” that either strengthen the trend or reverse it. In Europe’s case, its narrative test is arriving in the form of French elections.

This year’s elections are pivotal because the French are dangerously close to electing a populist, anti-euro candidate named Marine Le Pen. If she clenches a victory, there is a good chance France will leave the European Union, hammering the final nail into the coffin of the European experiment. The aftermath will quickly negate the short-term positives driving European equities.

The general consensus is Le Pen will lose. But this is only one possibility. There is also a good chance Le Pen will actually win. Like we said, no point in trying to predict the outcome directly. We would rather put our money in something clear-cut when it comes to these narrative “tests.” And that something is volatility.

The way we play volatility heading into macro events is based off how it behaves around equity earnings. Take a look at Amazon’s (AMZN, Financial) option volatility below:

The red dotted lines denote earnings announcements, and the blue line is the implied volatility of the weekly options (to learn more about implied volatility and options, click here).

The pattern is clear. As earnings approach, traders bid up implied volatility. This reflects the increased uncertainty that comes with a data release. The results serve as a narrative “test” for the stock. After earnings are announced, implied volatility plummets as pent up uncertainty is resolved. You can see this in the chart. The blue line crashes to normal levels after each earnings date.

Extrapolating this pattern into macro land means going long volatility into uncertain events. And then being short volatility over the event to benefit from the volatility crush after the uncertainty is resolved.

We executed this exact strategy during the U.S. elections. It played out perfectly. VIX ran up before the event and sold off hard afterward.

The VIX puts we traded after the U.S. elections were among our more profitable trades in 2016.

For the French elections, we wanted to pull from the same playbook.

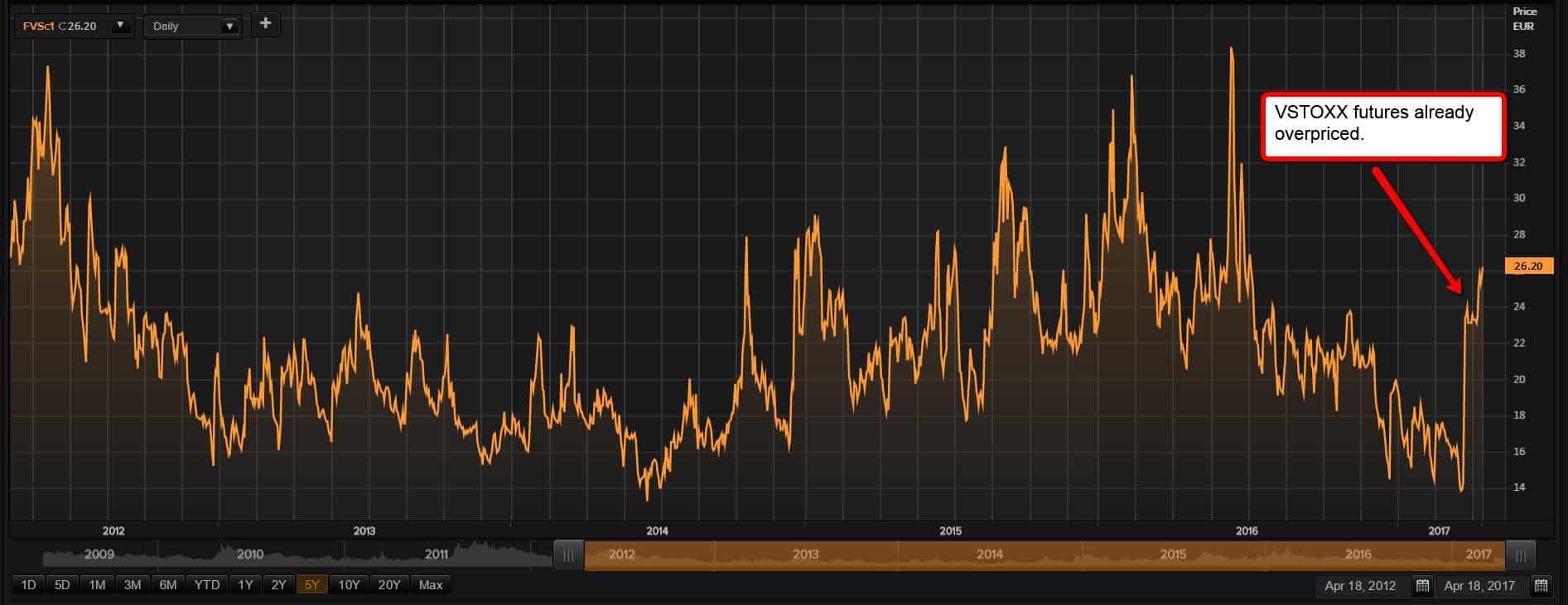

The European stock market has its own volatility index called VSTOXX. It is their version of the VIX. They also have futures on VSTOXX, making it possible to bet directly on volatility.

But in this case, VSTOXX futures were not the best option to play the French elections. They had already priced in the coming volatility.

VIX futures, on the other hand, were sitting in a quiet range near lows.

On top of the election catalyst, U.S. markets had gone a while without the VIX term structure inverting (represented by a value over 1.00 in the chart). At the time, it had been 147 straight days of peace and quiet since Trump’s win. And as we know, long periods of low volatility tend to precede a large spike.

There was clearly a trade here.

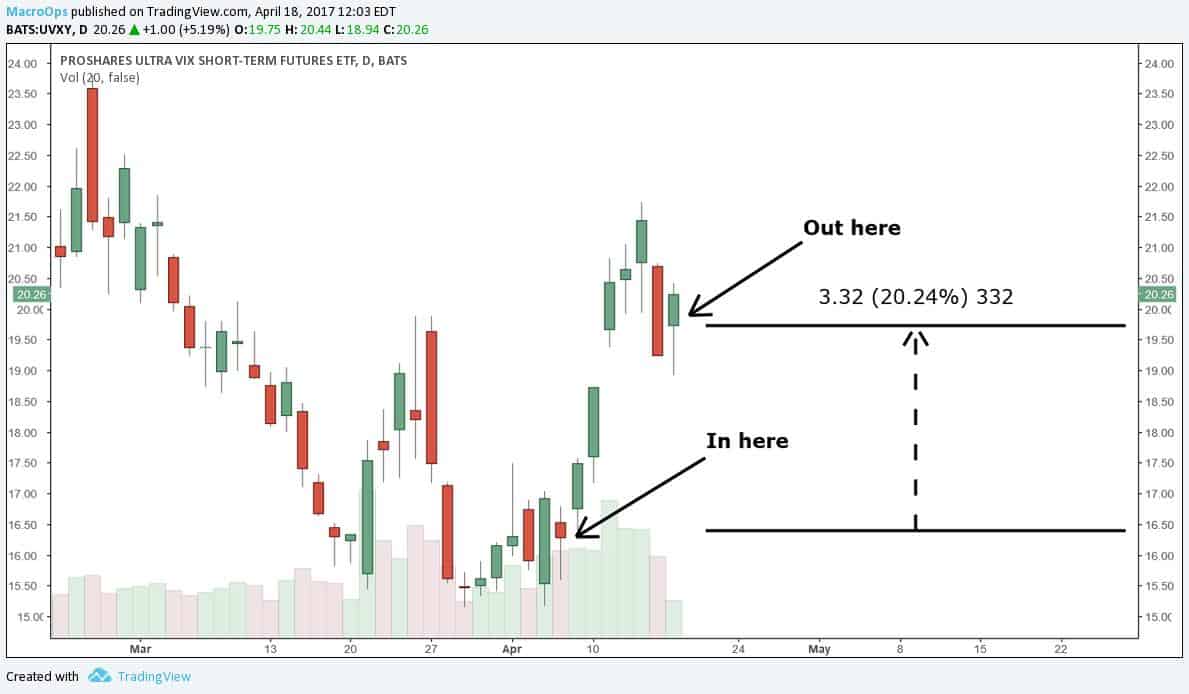

We ended up pulling the trigger and going long volatility using ProShares Trust Ultra VIX Short Term Futures (UVXY, Financial) on April 6 (our Hub members were alerted to the trade immediately).

Over the next week, UVXY ripped as traders rushed for cheaper hedges into the French elections. Our UVXY position appreciated 20% in six days before we exited.

The original plan was to hold into the Friday before the French elections. But Monday’s price action warranted an exit. The volatility term structure (VIX/VXV) closed below 1.00. Historically speaking, this was a reliable signal that VIX would continue to mean revert lower.

Volatility could still spike more before elections, but the risk-reward is not good enough to continue holding. At current levels, the trade is more of a 50-5- proposition than 80-20 like when we first entered. We are not in the business of betting on fair coins. We need edge. It was time to take profits and move on.

But lucky for us, the fun is not over. Things are getting more interesting as the election approaches. According to prediction markets, Le Pen is expected to win the most votes of any candidate in the first round of elections on April 23. She is represented by the light blue line below.

French elections are conducted over two rounds. The first includes all five presidential candidates. To secure the seat in the first round, a candidate needs over 50% of the votes. Otherwise, the elections go to a second round between the top two candidates. So although Le Pen is expected to win the most votes, it likely will not be enough to end the election. The race will go on to a second round on May 7. Emmanuel Macron (the safe bet) is the favorite to win the second round because both Fillon and Melenchon voters are expected to support him over Le Pen (Macron is pictured in light blue below).

We made good money betting on volatility into the first round of elections. The plan now is to sit back and see how things shake out. From there we will look and see if any volatility trades look attractive for the second round. Our upcoming May edition of the Macro Intelligence Report (MIR) will have all the details. To learn more about the MIR and how you can profit alongside us, click here.

Start a free 7-day trial of Premium Membership to GuruFocus.