When you are buying a company that is owned by Warren Buffett (Trades, Portfolio), there is always a sense of relief in knowing that the world’s most famous investor believes in the long-term fortune of the company in which you are investing.

With a near 3% yield, Kraft Heinz (KHC, Financial), which was born of the merger between Kraft Foods Group and Heinz Holding Corp., is an extremely appealing company, but the question is: how safe is its dividend?

The company, with its eight billion-dollar brands and enviable product portfolio, has one thing going for it: longevity. With daily staples like dairy products, condiments, coffee and meats being at the core of its offerings, it’s no wonder this is among the top five food and beverage companies in the world. And it’s equally no surprise why such a business would have an extremely long shelf life.

Source: Company Infographic

Despite the fact that its recent merger attempt with Unilever (UN, Financial) fell through, we learned an important lesson about how the company wants to move into the future. The M&A approach to growth is the only one that will work in such a mature market and for such a mature company.

During the most recent quarter, the company paid $736 million in dividends, or 47.4% of its operating income of $1.55 billion for the quarter. Long-term debt stood at $29.75 billion by the end of first quarter with $3.24 billion in cash on hand.

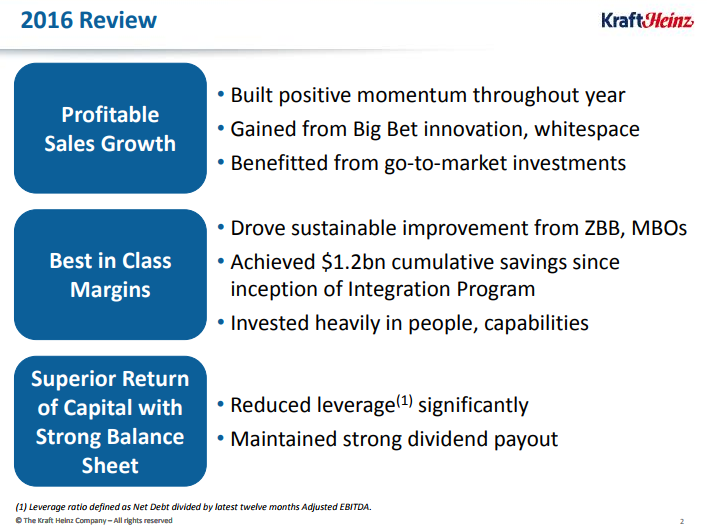

At the 2016 review presentation, Kraft Heinz made it amply clear that it wants to keep reducing leverage, strengthen its balance sheet and keep dividend growth on the upswing.

Source: Kraft-Heinz Q4-16 Presentation

Though the work ahead might seem tough going, the fact that the company has two fiscally disciplined companies as its largest investors – Berkshire Hathaway (BRK.A, Financial)(BRK.B, Financial) and 3G Capital – does give it a significant advantage as it deals with debt, engages in cost control and keeps its acquisitions going.

The strategy now is to have fewer, but larger, brands to help cut overall operational expenditure.

“In short, our strategy of prioritizing fewer, bigger and bolder bets is paying off. Underpinning all of this, we remain on track with our cost savings initiatives and the pace of savings is coming in very much as expected so far this year. Cumulative savings from our integration program are approximately $1.3 billion, and we continue to generate savings from ZBB and supply chain initiatives in all our zones outside of North America.” – Bernardo Vieira Hees, CEO of Kraft Heinz, during the recent earnings call

Revenues in the first quarter declined from $6.57 billion to $6.36 billion this year with a drop of 2.7% in organic sales. The 2.8% yield and the stock’s sideways movement since third-quarter 2016 can be attributed to the revenue growth slowdown.

That said, the company’s strong product portfolio and its equally strong management makes it an irresistible dividend play –Â and for nothing less than decades more.

Disclosure: I have no positions in the stock mentioned above and no intention to initiate a position in the next 72 hours.

Â