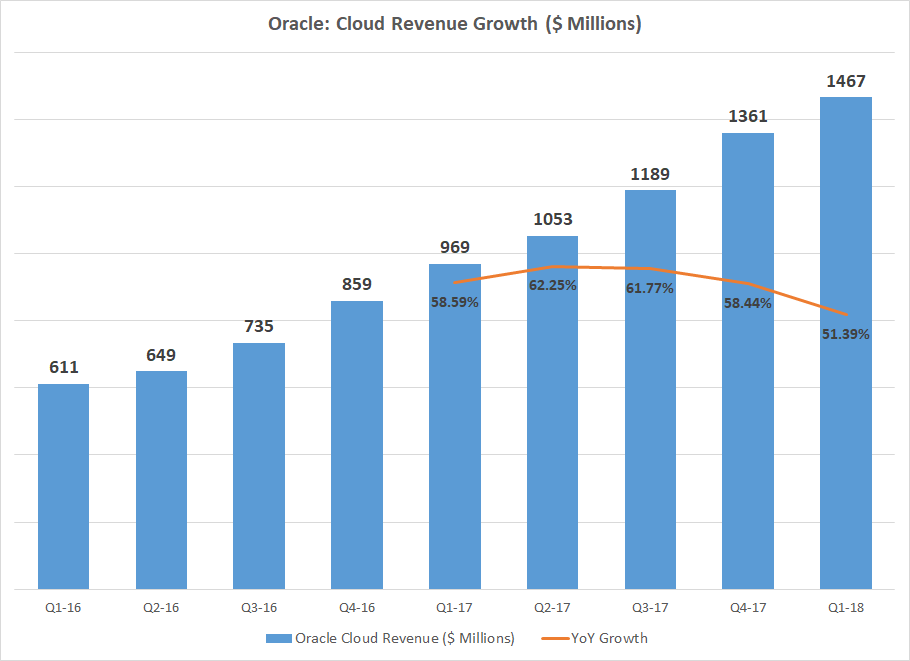

Oracle (ORCL, Financial) nearly fired on all cylinders during the first quarter of 2018, beating Wall Street expectations both on the top line as well as the bottom line as Cloud remained the fastest-growing segment for Oracle, posting 51% growth compared to last year. But Oracle’s stock price sharply declined by 7.67% after the results were announced: Oracle’s guidance for the second quarter came in well below market expectations.

Oracle expects second-quarter Cloud revenue to grow in the 39% to 42% range, resulting in 2% to 4% net revenue growth, and earnings per share of 64 cents to 68 cents. Wall Street was expecting second-quarter earnings per share of 68 cents, right at the top end of Oracle’s guidance. In a market that moves from one earnings estimate to another, the possibility of lower-than-expected revenue growth and EPS numbers has pushed the stock price to drop sharply as soon as the numbers were released.

To add to the below-par guidance numbers, Oracle’s expectation of less than 50% growth in Cloud also affected sentiment, simply because Oracle’s Cloud revenue actually grew in excess of 50% for the last five quarters.

With Amazon (AMZN, Financial) and Microsoft (MSFT, Financial) still posting solid revenue growth numbers despite their size and scale, the much smaller Oracle should be able to post strong growth, and it remains to be seen if this is the start of slower Cloud revenue growth for Oracle. If the numbers recover during the second half of the year, it will be great news for the company, but if they continue to edge lower, Oracle’s stock will remain under pressure because Cloud is already the lead revenue growth driver for Oracle.

Oracle didn’t give out any details about why the company expects sub-50% Cloud revenue growth during the second quarter. With quarterly Cloud revenue at around $1.5 billion, Oracle needs to keep expanding at a strong rate if it wants to catch up with Amazon and Microsoft. Both theses companies make more than $4 billion each in quarterly revenues from Cloud. With IBM (IBM, Financial) and Google also in the fray, competition is intense in the Cloud Computing segment, so these concerns played a huge role in affecting market sentiment against Oracle.

But Oracle is still growing, and the company has already shown that its on-premise revenues are not declining as fast as some would have thought. Moreover, Cloud revenue is now able to more than compensate for any losses from the company’s legacy business segments. The sharp drop in stock price on Sept. 15 was a typical overreaction from Wall Street, and investors should use opportunities like this to buy Oracle.

Disclosure: I have no positions in the stocks mentioned above and no intention to initiate a position in the next 72 hours.