Longleaf Partners just released its third-quarter letter, and it contains a number of strategic lessons any DIY investor may want to implement. Longleaf details three areas of the market where it has historically enjoyed much success and current ideas that fit the framework. The areas are time arbitrage, leadership and complexity. Over the years I’ve incorporated all three hunting grounds for ideas within my own investing and know from experience there’s value there. I’ll discuss every area and share Longleaf’s unique insights on the subject (read the entire letter here):

Time arbitrage

"The two most powerful warriors are patience and time."Â – Leo Tolstoy

Â

Time arbitrage is a fancy way of saying you make money by sitting on your ass – which is how Charlie Munger (Trades, Portfolio) puts it.

"Southeastern assesses how a company’s value per share will grow over the next three to five-plus years. Arbitraging this investment time horizon difference surfaces many opportunities for a patient investor focused on the intrinsic worth of a company. For example, a cyclical business such as CNH Industrial’s (CNHI, Financial) agricultural equipment has depressed near-term earnings that should recover as corn and other commodity prices rise above multiyear lows."

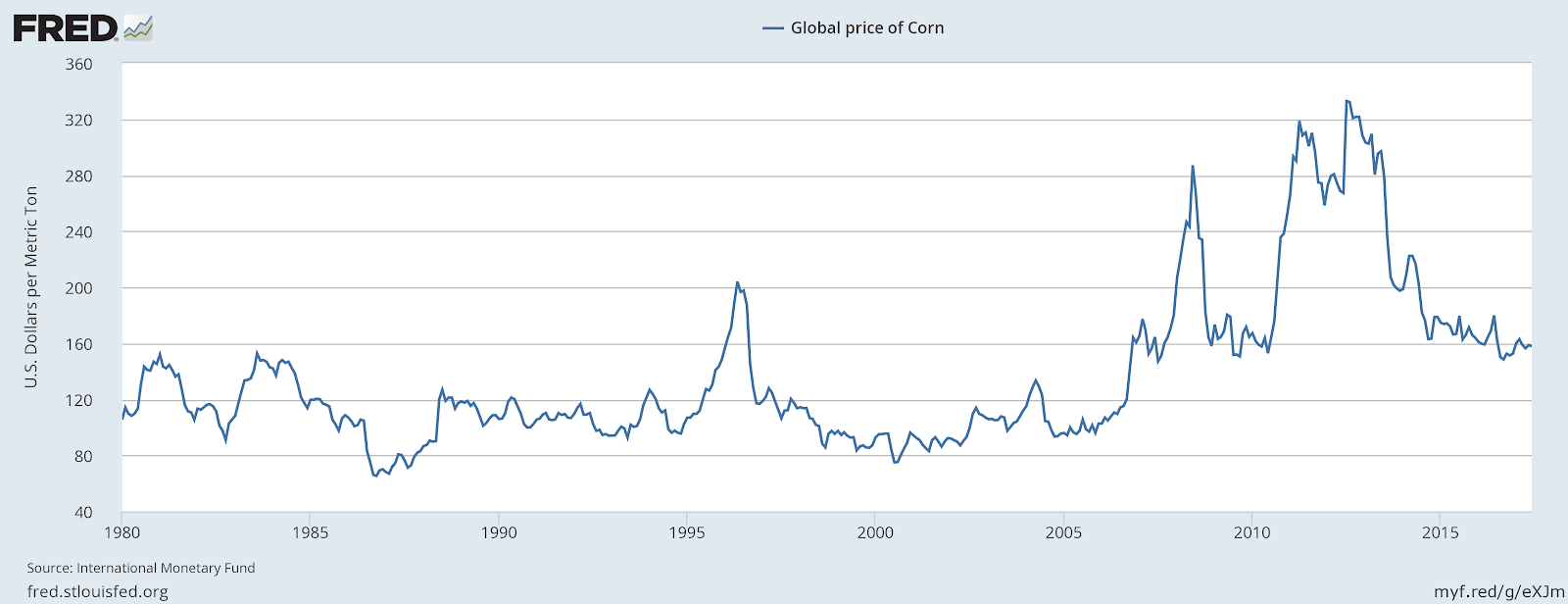

Even though I lack the 40 years of investing experience Longleaf can lean on, I have enough experience to confirm the notion the market can aggressively discount future (uncertain) earnings if they are one year-plus out. Generally speaking it’s all about the next year. There are some exceptions like Tesla (TSLA, Financial) or biotechs where it is all about the dream. In those cases and almost inexplicably the market discounts future earnings very generously. Corn is at multiyear lows, but it is not that low in a historical perspective going back to the 1980s:

Alphabet (GOOG, Financial) (GOOGL, Financial) is a favorite of value-oriented managers, and it is investing heavily in businesses that aren’t close to monetization; project Loon, self-driving cars and even its cloud business are not yet getting much credit. Baidu (BIDU, Financial) is a company I’m invested in as well and just like Alphabet it is investing heavily in future cash flow generating businesses. You can argue both companies also share the other two characteristics they like to look for – great leadership and complexity.

Leadership

"I am not afraid of an army of lions led by a sheep; I am afraid of an army of sheep led by a lion." –Â Alexander the Great

Â

Looking for great leadership works if it doesn’t show up in the earnings yet. One way it doesn’t work is in a mature business where great leadership has been present for many years. When this is the case the quality of management is usually reflected in the height of margins and consequently earnings and potentially even in the earnings growth rate as well. By putting a lot of emphasis on the terrific management you may be double counting.

- If managers are skilled capital allocators at a firm that’s spewing off cash that’s often only detected by the market after decades of operation and even then it’s sometimes discounted.

- When a great CEO is incoming at a firm that was previously under mediocre management can also be severely discounted.

- Owner-operators often take a countercyclical approach and get discounted severely for lagging in bull markets or by stretching the balance sheet during recessionary periods.

Superior management teams and owner-operators who are willing to think and act unconventionally for the benefit of shareholders can create discount opportunities because standard valuation metrics do not adequately encompass what investors are getting. Last year, Chairman John Malone and CEO Greg Maffei of Liberty Media Corp. divided the company into three different tracking stocks. The most complex, Liberty Media Group, also had the most upside potential for smart capital allocation due to its large level of cash and investments. The company quickly announced its purchase of the global racing circuit Formula One (FWONK, Financial) and adopted the name for the combined entity. Even better, Malone and Maffei recruited Chase Carey, an all-time great Southeastern partner during his time as CEO at DirecTV, to be CEO. Our partners created instant value in an unexpected way but also laid the foundation for significant future upside.

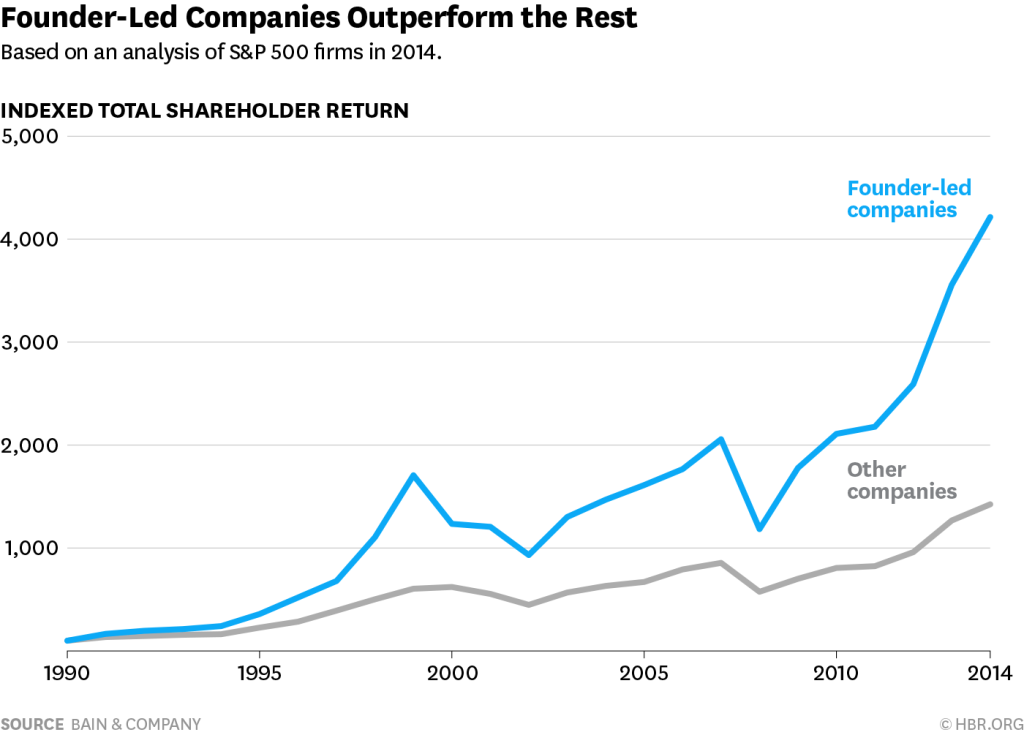

Owner-operators have been documented to outperform (HBR research here). Especially in down markets these guys tend to do well; with the market at its second-highest CAPE ratio ever, that gives me some comfort. Another idea in this category that’s mentioned in the letter is Fairfax Financial (FFH, Financial) led by guru Prem Watsa (Trades, Portfolio).

Complexity

"Fools ignore complexity. Pragmatists suffer it. Some can avoid it. Geniuses remove it." –Â Alan Perlis

Â

Complex companies are often run by owner-operators. A strong shareholder is required to keep a diversified conglomerate – and its accompanying discount – together. Otherwise the market will demand value creation through spinoffs. Agent operators will have a tougher task keeping their jobs if they start plowing money into unrelated businesses. If these are unsuccessful for even a short period, they quickly get into very uncomfortable conversations with their boards. Longleaf:

"Companies with complex structures (as opposed to complex products such as biotech or information technology) can be overlooked because they require time, multi-industry knowledge and global perspective to appraise properly."Â – Longleaf

Complex businesses as great places to look for outperformance have been confirmed by the academic community (Lou Cohen 2010). Quantpedia, who catalogs academic financial research, writes:

Very complex companies are hard to evaluate as the investor has to consider effects of many different industrial branches in which the company runs a business. It is therefore no surprise that academic research detected price anomaly in complicated firms – conglomerates. Research says that investors’ limited processing capacity and complexity in information processing leads to a significant delay in the impounding of information into asset prices.

Longleaf has a number of favorites:

CK Hutchison (CKHUY, Financial) spun off its property business, which made properly assessing the remaining segments even more important. Other examples of multi-industry complexity and change in focus include EXOR (MIL:EXO, Financial) and Graham Holdings (GHC).

But also:

LafargeHolcim (HCMLF) amortizes acquisition intangibles and large upfront spending for its cement plants, causing current earnings per share, which most cement analysts use as the foundation for their stock recommendations, to be well below the free cash flow power of the company.

Positions

Here’s an overview of the firm's largest positions:

Conclusion

Longleaf runs its firm using three principles that make a lot of sense to me: time arbitrage, leadership and complexity. In their latest letter they break down why these principles work and what ideas are based on these principles. Interesting investment ideas mentioned are CK Hutchison, Graham Holdings, EXOR, Liberty Media Group, Fairfax Financial, Alphabet, Baidu and CNH Industrial.

Disclosures: Author is long Baidu and Franklin Resources.