I’ve been quite interested in investing in shipping over the years. Currently shipping rates are very low and shipping stocks depressed. Meanwhile the S&P 500 is at all-time highs. Shipping stocks are not as correlated to the broader market because they respond to shipping rates specifically and not so much to the general economic outlook. Now is a perfect time to look more closely at shipping stocks and get some solid diversification.

Unfortunately, shipping is a very asset-intensive industry and it takes a tremendous amount of time to determine the value of each company's fleet. Especially as there are something like 100 publicly traded shipping companies. To find better investments faster, I worked together with a brilliant programmer to develop a screening tool to quickly compare the company’s enterprise value to a calculated enterprise value (fleet value).

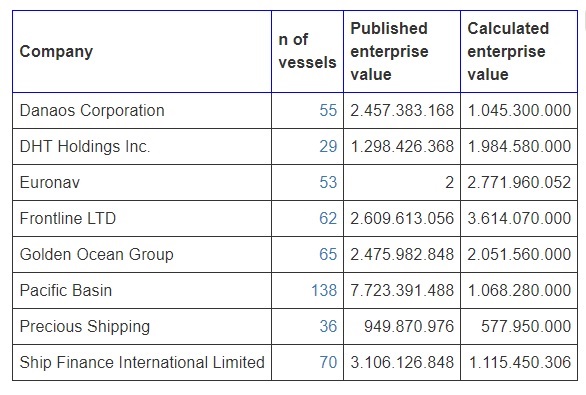

This calculated enterprise value is actually the value of the fleet based on recent broker values. Running the beta test of the screener with the first eight companies, DHT Holdings (DHT, Financial) and Frontline (FRO, Financial) jumped out at me in a positive way. Possibly other companies like Ship Finance International (SFL, Financial) derived some of their value from activities besides monetizing owned ships. Companies that lease ships and re-lease ships will also tend to score badly. However, it is very helpful to find undervalued opportunities backed by hard assets:

Source: VLCCAnalyzer

Currently, the information offered by the screener is still quite limited, which is why I pulled additional information through the GuruFocus screening tool:

Frontline and DHT Holdings are still quite attractive when reviewing their financial stats. DHT Holdings trades at a more attractive EBITDA and EBIT multiple. Its revenue is more predictable and its debt profile suggests the company is run more safely.

However, Frontline achieved a median return on capital that’s over 2x that of DHT Holdings over the past 10 years. Ultimately, this is an important driver of shareholder returns.

Last year Frontline tried buying DHT Holdings:

"In January 2017, the Company approached DHT Holdings, Inc. (NYSE:DHT), or DHT, with a non-binding proposal for a possible business combination whereby the Company would acquire all outstanding shares of common stock of DHT in a stock-for-stock transaction at a ratio of 0.725 Company shares for each DHT share. The proposal was declined by DHT’s board of directors. The Company, together with its affiliates, has also acquired 15,356,009 shares of DHT, representing approximately 16.4% of DHT's outstanding common stock based on 93,366,062 common stock outstanding. Of the total, the Company purchased 10,891,009 shares for an aggregate cost of $46.1 million. In February 2017, Frontline presented a final offer of 0.80 Frontline shares per DHT share, which was also declined by DHT’s board of directors," the company said in an SEC filing.

That means Frontline, which is not the worst capital allocator in the industry, paid on average $4.20 per share it acquired on the open market. Subsequently, it was willing to pay a control premium to get its hands on the remainder of DHT Holdings' shares.

What makes DHT Holdings so attractive is the average age of its vessels:

Image: DHT fleet

Its ships are relatively young. That doesn't just mean it has a long time on the clock, but it is also more fuel efficient. With energy prices in an uptrend, that is becoming increasingly important.

The VLCCAnalyzer tool takes age into account, which is how it arrived at a calculated enterprise value over 50% of Frontline’s while the company owns half as many vessels.

I also quite like DHT Holdings' large number of tankers on spot. If you have ships on contract, your revenue stream is more reliable. However, in shipping you make the big money by being on spot when the price of transportation spikes for what’s typically a short period of time.

Of the companies VLCCanalyzer allows me to look at, I like DHT Holdings a lot. Its EV/EBITDA of 7.9x is attractive, and it trades at 4.58x free cash flow and just 0.57x book value. There is debt, but the company sports a very low break-even on shipping rates. That helps in downturns as competitors go bankrupt first, which slows down new capacity coming into the market.