The recent action in the stock market seems to be governed by crowd psychology and reminds us of a theory we created in college called the “coat theory.” Back in the 1970s, the fraternities and sororities at my alma mater hosted several mixers so the students could get to know each other better. The ladies hung their coats on a large coat rack just inside the door to our fraternity house. We sang and shared our dessert with our sorority guests.

It didn’t take us very long to figure out the behavior of these sorority girls. When the main part of exchange was over, one of the ladies would go to the coat rack, put her coat on and prepare to leave. Within five to 10 minutes, virtually every one of their sorority sisters had gone to the coat rack and headed back to their dormitory or home near campus. We called this behavior “coat theory.” The theory was that one coat would quickly lead to all the coats.

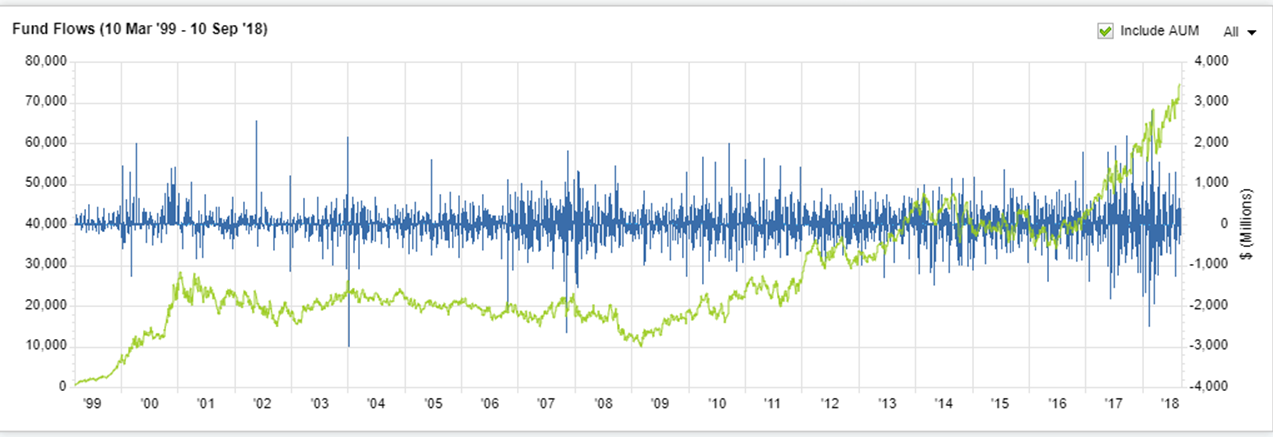

From a historical perspective, tech stocks are as large a part of the S&P 500 Index as they were at their all-time peak in popularity at the end of 1999. If you count Amazon (AMZN, Financial) and Netflix (NFLX, Financial) as tech companies, the tech stock coat rack looks just as crowded today. Here is a chart which shows that the most popular tech exchange-traded fund, the PowerShares QQQ Trust (QQQ), has seen its assets grow to $75 billion recently, dwarfing the peak of $27 billion in 2000. (1)

Source: FactSet

When you put 30 or more coats on the coat rack inside the entrance of our fraternity, the rack got crowded. In the stock market, when everyone piles into the same stocks, it also gets very crowded. Unless you have been hiding under a rock, you know that we have had an unusually long stretch of popularity in the largest-cap tech-stock darlings, and those highly-priced shares have gained a disproportionately large part of market gains in recent years.

With the recent vaping of Facebook (FB, Financial) and Twitter (TWTR, Financial), and the temperature-reducing decline of Tesla (TSLA, Financial) shares, numerous questions must be asked. Is there a change in the crowd psychology surrounding the tech stocks? Were Facebook and Twitter the first people in the sorority to get their coats and will this lead to a pendulum swing in crowd psychology in the stock market? How twisted up is the ownership of tech in the S&P 500 Index and does this make it a crowded coat rack? Where will the money go if investors pull their coats off the glam tech rack?

After getting vaped, Facebook and Twitter have not rallied like tech stocks did in prior head fake corrections. Also, Tesla quickly joined the negative swing in the psychology by pretending to go private and attempting to squeeze short sellers. Now, all the biggest internet-based businesses are having their power in the marketplace examined by political leaders and antitrust legal minds. In a recent New York Times article, journalists are now sharing the debate about monopoly status and the anticompetitive nature of Amazon, Alphabet (GOOG)(GOOGL, Financial) and Facebook (2). This wasn’t true in prior corrections.

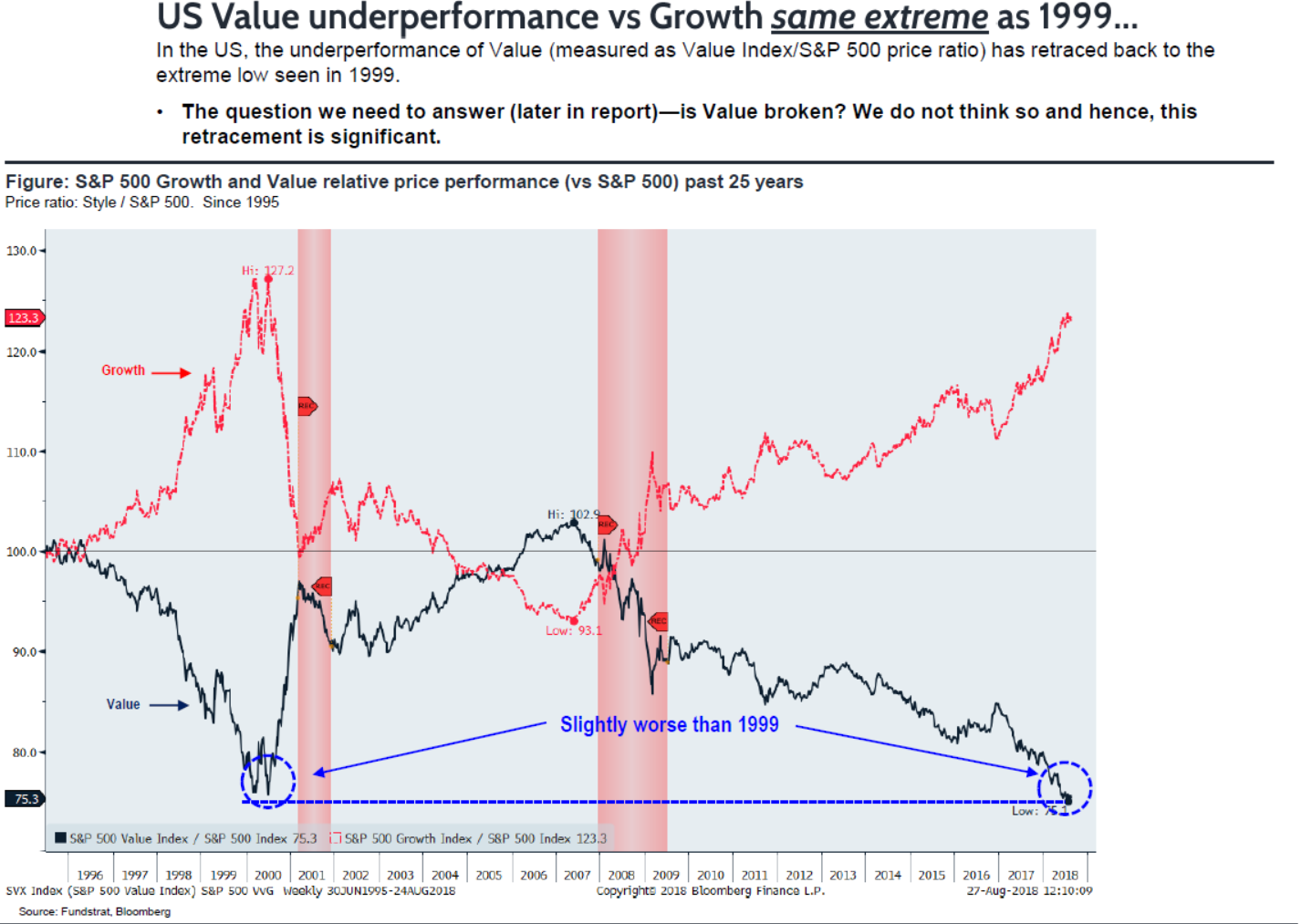

We have had many head fakes on prior pullbacks in glam tech shares. However, this current run in momentum growth stock investing looks long in the tooth over 20 years of history. Fundstrat has provided some great research and the chart below (3):

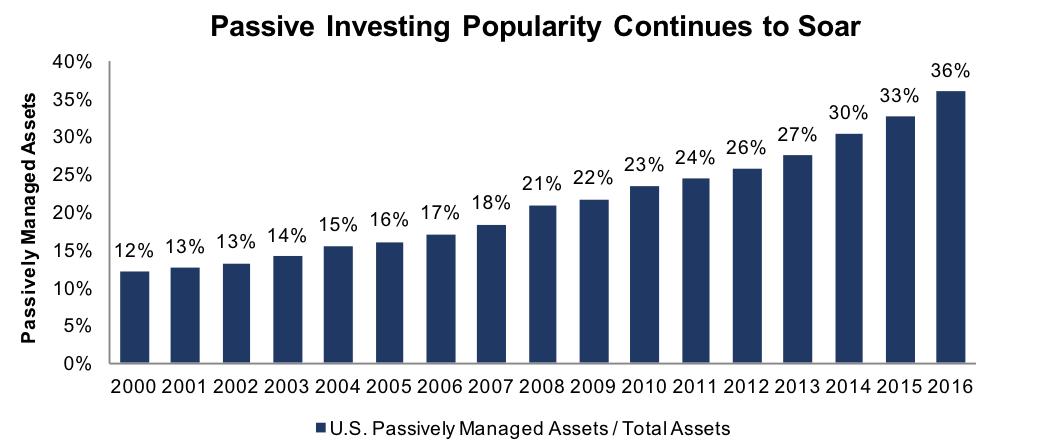

The S&P 500 Index has become dramatically more popular as a percentage of total assets invested in the U.S. stock market, which means a negative feedback loop could be triggered by the combination of a coat theory event in glam tech shares and a crowd exit from the S&P 500 Index itself (4):Â

Source: New Constructs

When the tech bubble broke in 2000, tech was 40% of the S&P 500 Index and it was 12% of the total assets invested the U.S. stock market. How will it react as coats are pulled from the current 40% tech representation in an index which is greater than 36% of total stock market assets? The S&P 500 Index fell 40% in three years back then and that coat rack was way less loaded from an indexing standpoint.

Lastly, our job as stock pickers is to find companies which fit our eight criteria with lots of room on their coat rack. Our guess is the growth money will move toward health care shares like Walgreens (WBA, Financial) and Amgen (AMGN, Financial). Both trade at very reasonable price-earnings multiples and have been questioned by Amazon’s push into health care, which kept many “coats” away.

The all-out assault on old media has left an empty coat rack for Disney (DIS, Financial) and Discovery Inc. (DISCA, Financial). These are wonderful content creators in a world where content just keeps getting more valuable. Also, they are favorites among moms, who to this day are still responsible for most of the consumer spending in the U.S.

History would argue that even if this correction in glam tech shares is temporary, the long-duration investor could benefit from avoiding the remainder of the time that their coat rack remains full. However, there are some obvious signs that all is not well for those who want to keep the “social life” going in the glam tech sector.

1 Source: FactSet

2Â The New York Times (Amazon's Antitrust Antagonist Has a Breakthrough Idea)

3 Source: Fundstrat.

4 Source: New Constructs (Hidden Trigger For Another (Flash) Crash: Passive Investing - New Constructs)

Disclosure:Â Smead Capital holds WBA, AMGN, DISCA and DIS.

The information contained in this missive represents Smead Capital Management's opinions and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.