Rehabilitation hospitals, crucial for aiding recovery from significant surgeries and injuries, represent a profitable segment in the healthcare sector. However, federal data and inspection reports have highlighted some concerns about facilities managed by Encompass Health (EHC, Financial) and other profit-driven organizations. These reports indicate occasional serious patient harm and below-average performance on specific safety metrics tracked by Medicare.

While inspections sometimes uncover severe injury cases, regulatory bodies do not notify the public or impose penalties on these rehab centers as they do with nursing homes. Despite these issues, Encompass is noted for its effectiveness in assisting most patients to return home and maintain their recovery. Yet, Medicare data also suggests that Encompass owns a number of rehabs with high rates of avoidable readmissions to general hospitals. Currently, Encompass Health shares have dropped nearly 10%, trading at $107.81 during afternoon market sessions.

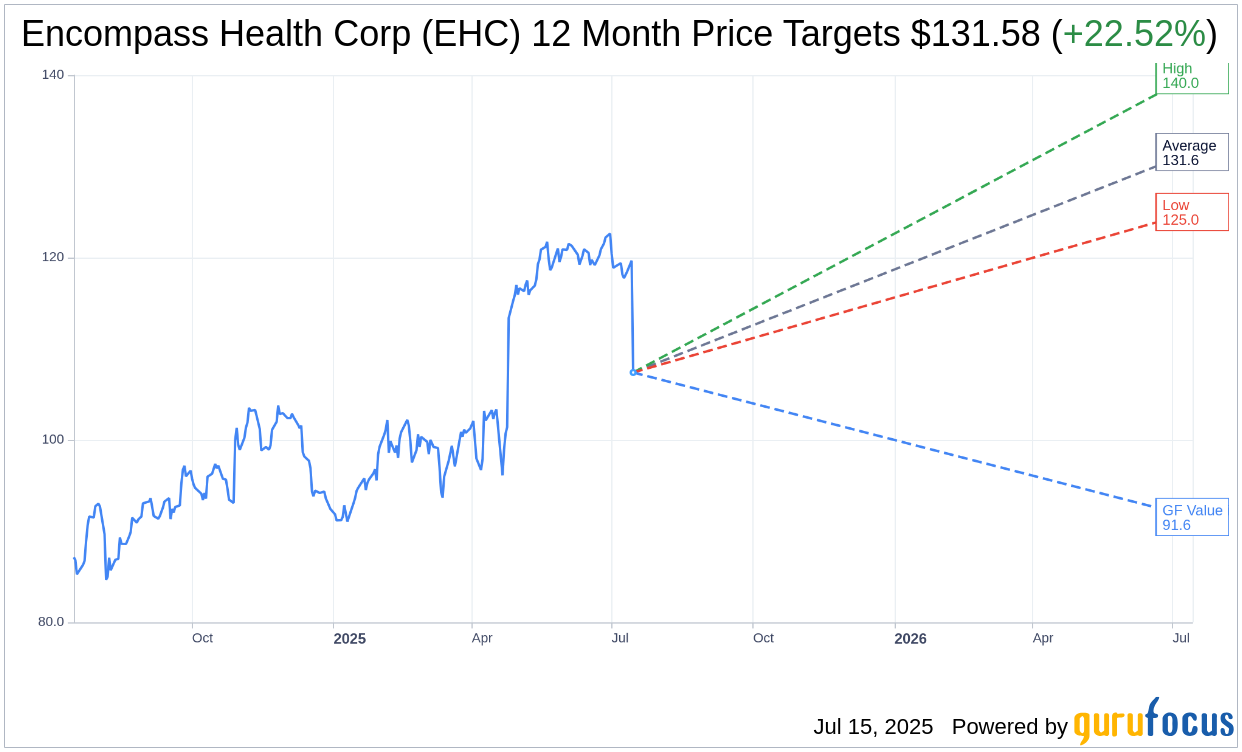

Wall Street Analysts Forecast

Based on the one-year price targets offered by 12 analysts, the average target price for Encompass Health Corp (EHC, Financial) is $131.58 with a high estimate of $140.00 and a low estimate of $125.00. The average target implies an upside of 22.52% from the current price of $107.40. More detailed estimate data can be found on the Encompass Health Corp (EHC) Forecast page.

Based on the consensus recommendation from 13 brokerage firms, Encompass Health Corp's (EHC, Financial) average brokerage recommendation is currently 1.5, indicating "Buy" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Encompass Health Corp (EHC, Financial) in one year is $91.56, suggesting a downside of 14.75% from the current price of $107.4. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Encompass Health Corp (EHC) Summary page.

EHC Key Business Developments

Release Date: April 25, 2025

- Revenue: Increased 10.6% to $1.46 billion.

- Adjusted EBITDA: Increased 14.9% to $313.6 million.

- Total Discharge Growth: Increased 6.3%.

- Same Store Discharges: Grew 4.4%.

- Net Revenue per Discharge: Increased 3.9%.

- Q1 Adjusted Free Cash Flow: Increased 32.7% to $222.4 million.

- Contract Labor Costs: Declined $5 million to $28.6 million.

- Net Leverage: 2.1 times at quarter end.

- Unrestricted Cash: $95.8 million.

- 2025 Guidance - Net Operating Revenue: $5.85 billion to $5.925 billion.

- 2025 Guidance - Adjusted EBITDA: $1.185 billion to $1.220 billion.

- 2025 Guidance - Adjusted EPS: $4.85 to $5.10.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- First quarter revenues increased by 10.6% and adjusted EBITDA rose by 14.9%, indicating strong financial performance.

- Total discharge growth of 6.3% was achieved, with same-store discharges growing by 4.4%, showcasing robust operational performance.

- The company opened a new 40-bed joint venture hospital in Athens, Georgia, and plans to open six De Novos with a total of 300 beds, reflecting strategic expansion efforts.

- Encompass Health Corp (EHC, Financial) reported a decrease in premium labor costs, with contract labor costs down by $2.9 million from the previous year.

- The company increased its 2025 guidance for net operating revenue, adjusted EBITDA, and adjusted earnings per share, demonstrating confidence in future performance.

Negative Points

- Benefits expense per FTE increased by 14%, driven by an increase in the severity and frequency of group medical claims, which could impact future profitability.

- The company anticipates elevated group medical expense growth in Q2, which may affect financial results.

- Despite a decrease in contract labor costs, the company still faces challenges in maintaining labor efficiency and managing staffing levels.

- The company's exposure to regulatory developments and potential changes in Medicare and Medicaid reimbursement rates pose risks to future financial performance.

- The high occupancy rates and demand for inpatient rehabilitation services may strain existing resources and require significant capital investment for expansion.