Evercore ISI has commenced its coverage on Cognizant (CTSH, Financial) with an Outperform rating, setting a price target of $100. The firm sees Cognizant as well-equipped to reclaim a leading position in its sector, particularly with strong potential for consistent growth in constant currency terms. Analysts at Evercore ISI suggest that Cognizant is capable of capturing a larger share in an expanding total addressable market, which could lead to a stock revaluation. This optimistic outlook indicates confidence in Cognizant's strategic positioning within the industry.

Wall Street Analysts Forecast

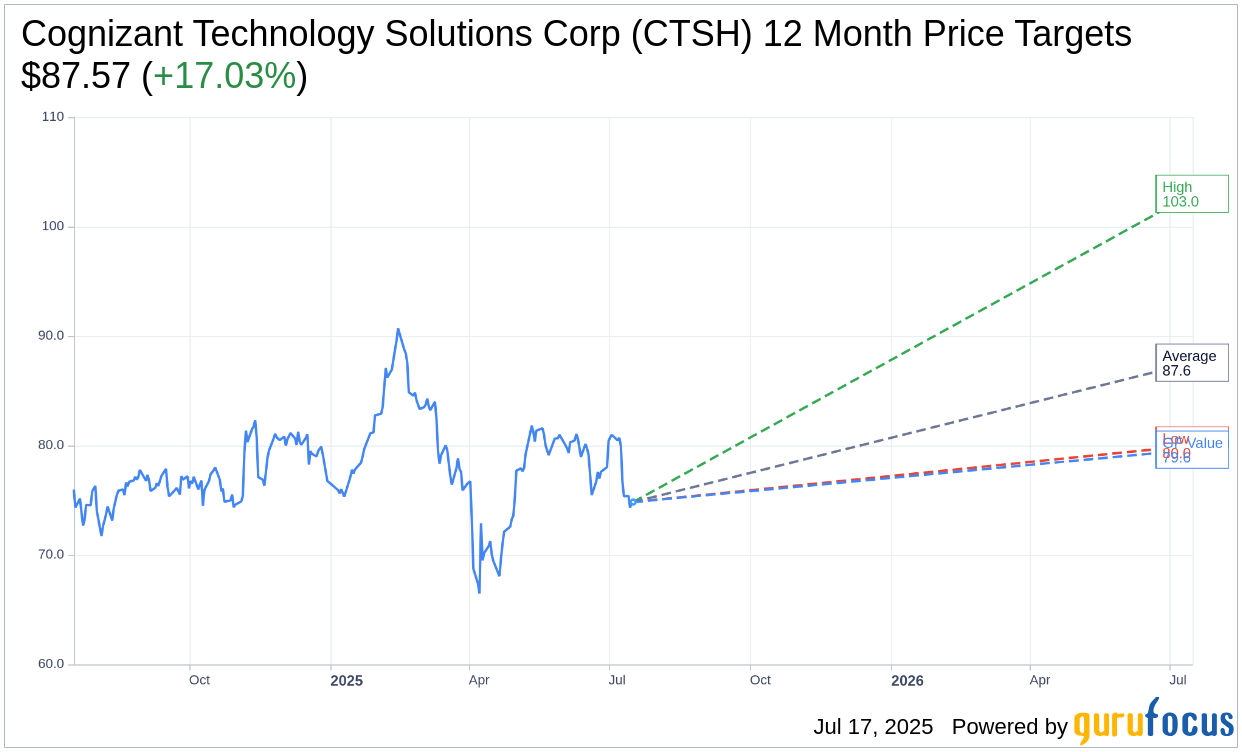

Based on the one-year price targets offered by 19 analysts, the average target price for Cognizant Technology Solutions Corp (CTSH, Financial) is $87.57 with a high estimate of $103.00 and a low estimate of $80.00. The average target implies an upside of 17.03% from the current price of $74.83. More detailed estimate data can be found on the Cognizant Technology Solutions Corp (CTSH) Forecast page.

Based on the consensus recommendation from 26 brokerage firms, Cognizant Technology Solutions Corp's (CTSH, Financial) average brokerage recommendation is currently 2.7, indicating "Hold" status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Cognizant Technology Solutions Corp (CTSH, Financial) in one year is $79.62, suggesting a upside of 6.4% from the current price of $74.83. GF Value is GuruFocus' estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business' performance. More detailed data can be found on the Cognizant Technology Solutions Corp (CTSH) Summary page.

CTSH Key Business Developments

Release Date: April 30, 2025

- Revenue: $5.1 billion, up 8.2% year-over-year in constant currency.

- Health Sciences Revenue Growth: Over 11% year-over-year in constant currency.

- Financial Services Revenue Growth: Up 6.5% year-over-year in constant currency.

- Adjusted Operating Margin: 15.5%, improved by 40 basis points year-over-year.

- Adjusted EPS Growth: 10% year-over-year.

- Bookings Growth: 3% year-over-year on a trailing 12-month basis.

- Free Cash Flow: $393 million.

- Cash and Short-term Investments: $2 billion.

- Net Cash: $1.4 billion.

- Shareholder Returns: $364 million through share repurchases and dividends.

- Revenue Guidance for Q2 2025: Expected growth of 5% to 6.5% year-over-year in constant currency.

- Full Year 2025 Revenue Guidance: Expected growth of 3.5% to 6% in constant currency.

- Adjusted Operating Margin Guidance for 2025: 15.5% to 15.7%.

- EPS Guidance for 2025: $4.98 to $5.14, representing 5% to 8% growth.

- Planned Shareholder Returns for 2025: Approximately $1.7 billion, including $1.1 billion in share repurchases and $600 million in dividends.

For the complete transcript of the earnings call, please refer to the full earnings call transcript.

Positive Points

- Cognizant Technology Solutions Corp (CTSH, Financial) reported a strong start to 2025 with revenue growth of 8.2% year-over-year in constant currency, reaching $5.1 billion.

- The Health Sciences segment led revenue growth with an increase of over 11% year-over-year in constant currency, driven by large deals that offset discretionary spending pressures.

- Financial Services segment showed resilience, growing 6.5% year-over-year in constant currency, with healthy discretionary spending on cloud and data modernization.

- Adjusted operating margin improved by 40 basis points year-over-year to 15.5%, aligning with the company's full-year guidance for margin expansion.

- Cognizant Technology Solutions Corp (CTSH) is making significant investments in AI, with approximately 1,400 early Gen AI engagements, positioning the company to capitalize on AI-led productivity and innovation opportunities.

Negative Points

- April saw a slowdown in client decision-making and discretionary spending, particularly affecting the Health Sciences and Products and Resources segments.

- Despite strong first-quarter results, the macroeconomic environment remains uncertain, impacting client spending and decision-making.

- Bookings declined 7% year-over-year, driven by a decline in the Rest of the World region, which had significant deals in the prior year period.

- The Products and Resources segment experienced weak demand due to discretionary spending pressure and the impact of tariff policies.

- The company faces intense pricing pressure in large deals, requiring a focus on AI-led productivity to maintain competitive pricing.