Fiat Chrysler Automobiles (FCAU, Financial) acquired a large stake in Chrysler in 2009 after Chrysler filed for Chapter 11. When Chrysler emerged from the bankruptcy proceedings, its stakeholders were the United Auto Workers pension fund, Fiat and the U.S. and Canadian taxpayers through their respective governments. Over time, Sergio Marchionne brilliantly acquired the other parties' stakes. Marchionni did an especially great job in buying the 41.5% stake from the United Auto Workers at a reasonable price. The total cost to Fiat in order to acquire Chrysler added up to $4.9 billion. That excludes a billion-dollar pension liability though. Early 2014 Fiat announced a reorganization. Fiat merged the two companies into a new holding company. Later that year the Fiat group announced a proposal to spin off Ferrari. The company thinks it can spin off Ferrari before the end of 2015. This could serve as a catalyst for the market to re-rate the company.

source: company presentation

Financial strength

The company holds $25 billion in cash but unfortunately also has $35 billion in debt. Ebitda amounts to $8 billion. Its current ratio is below 1 which indicates there may be a problem. My opinion is that the company is financially vulnerable, and a sudden downturn could certainly throw it off course. However, the debt is mainly recourse to the core Fiat company, and subsidiaries can be saved from recourse. For example the company owns distinct highly coveted divisions like Ferrari and Maserati that not only could be spun out to shareholders, Ferrari is actually going to be spun out. Doing so in a crisis situation allows the company to raise capital which isn’t reflected in its current ratio. The company isn’t in the greatest of financial shapes, but when it's all hands on deck shareholders may come out with quite a few dollars in assets depending on how exactly the crisis plays out.

Management

Sergio Marchionne (CEO/chairman) is said to have been stunned when he learned executives at Fiat communicated with each other through their secretaries. He relocated his office to the fourth floor where the engineering department is. The chairman’s office used to be a swanky top-floor penthouse. He is widely regarded as an excellent manager and credited with the successful turnaround of Fiat and Chrysler although I’d argue that this process isn’t complete yet.

Marchionne is chairman of various boards and holds several other functions. This must be somewhat of a distraction, and it’s a strike against his leadership although outweighed by his apparent skill. Marchionne is also an outspoken proponent to improve the traditional Italian industry. Unions are a big problem for the Italian automaker and make it very difficult to maintain a manufacturing base within Italy. He advocates for local agreements between manufacturers and unions instead of striking collective bargaining agreements at the national level as an improvement.

Valuation

With all the moving parts in the Fiat Chrysler story, it’s not easy to value the company. To see the value of Fiat take its current sales or projected sales for 2015, I prefer the latter, and multiply it with the average net profit margin the company achieved over the past 10 years. In that time span there are a number of brutal crisis years but also a few good years. It certainly wasn’t the easiest of times. I’m using the average to keep the projection neutral. If we are moving into the better parts of a cycle, the company will do better and if we are going through another crunch it will surely do worse.

I think this is a conservative method because it doesn’t take into account the substantial restructuring the company underwent. A major change is, of course, that the Chrysler Fiat combination is a much larger platform bringing some economies of scale. More about that in a minute.

A net profit margin of 1.7% (which is the company’s 10-year average) would indicate conservative normalized forward earnings of ~$2 billion. With a market cap of $20 billion the company is trading at approximately 10x normalized forward earnings.

On average the S&P 500 trades at 18.5 times forward earnings. With the industry outlook being quite positive and with Marchionne (a manager who appears to be of far above average skill) it’s reasonable to expect the normalized earnings (based on historical figures) to be exceeded.

That makes this global automaker a real bargain which I can easily see at $30 in 1-3 years. That is almost a 100% return from today's price of $15.44.

Risks

Fiat Chrysler has quite a bit of debt, $35 billion, on its books and a large fixed cost base, a trait shared with its peer automakers. If sales fall back in a big way, which sometimes occurs in the cyclical auto industry that is dependent on the economy, then Fiat Chrysler will face a major challenge. Under the right circumstances Fiat Chrysler could save shareholders from impairment by spinning out divisions and breaking up the company again, while keeping the debt concentrated on the core Fiat company.

Outlook

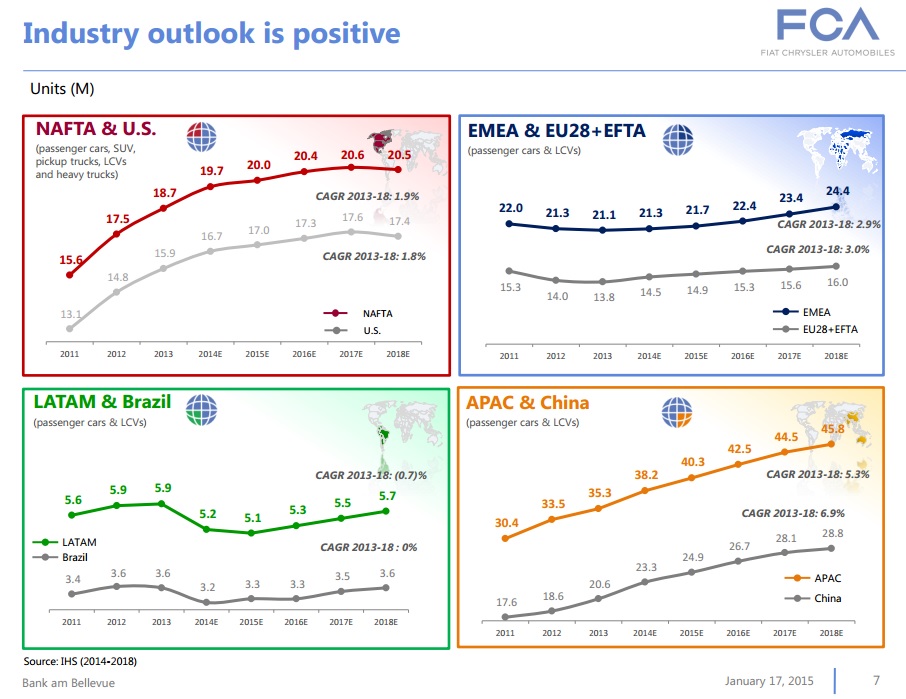

Management guidance for 2015 revenue is ~$117 billion. The Ferrari spin-off could be a catalyst for the market to recognize the value of Fiat’s sum of the parts. Furthermore Fiat Chrysler competes in a brutal industry with virtually no barriers to entry and competitive advantages other than scale. Operating results will vary depending how successful Fiat Chrysler is in meeting the demands of the market. The industry outlook is certainly favorable with solid expected CAGR globally:

Even when Marchionne doesn't succeed in achieving higher average net profit margins with Fiat Chrysler than Fiat has historically achieved, expected growth rate of the industry will very quickly turn a purchase at 10x normalized earnings into a very profitable one.